If you're working through a recruitment agency in the UK, you've almost certainly been asked to choose between an umbrella company and agency PAYE. Both pay you under PAYE. Both deduct income tax and National Insurance. Yet the take-home pay, the rights you get and the way the rate is quoted to you can look very different. This guide unpacks the real differences so you can pick the option that actually leaves you better off.

What is agency PAYE?

Agency PAYE means the recruitment agency that places you with the end client also employs you for payroll purposes. They run you through their own PAYE scheme, deduct income tax and Class 1 National Insurance, and pay the employer's NI contribution themselves out of the rate they've agreed with the client.

The headline rate you're quoted is the rate you actually earn before personal tax. You receive statutory holiday pay (28 days including bank holidays for a full-time worker), statutory sick pay if you qualify, and pension auto-enrolment after the qualifying period.

What is an umbrella company?

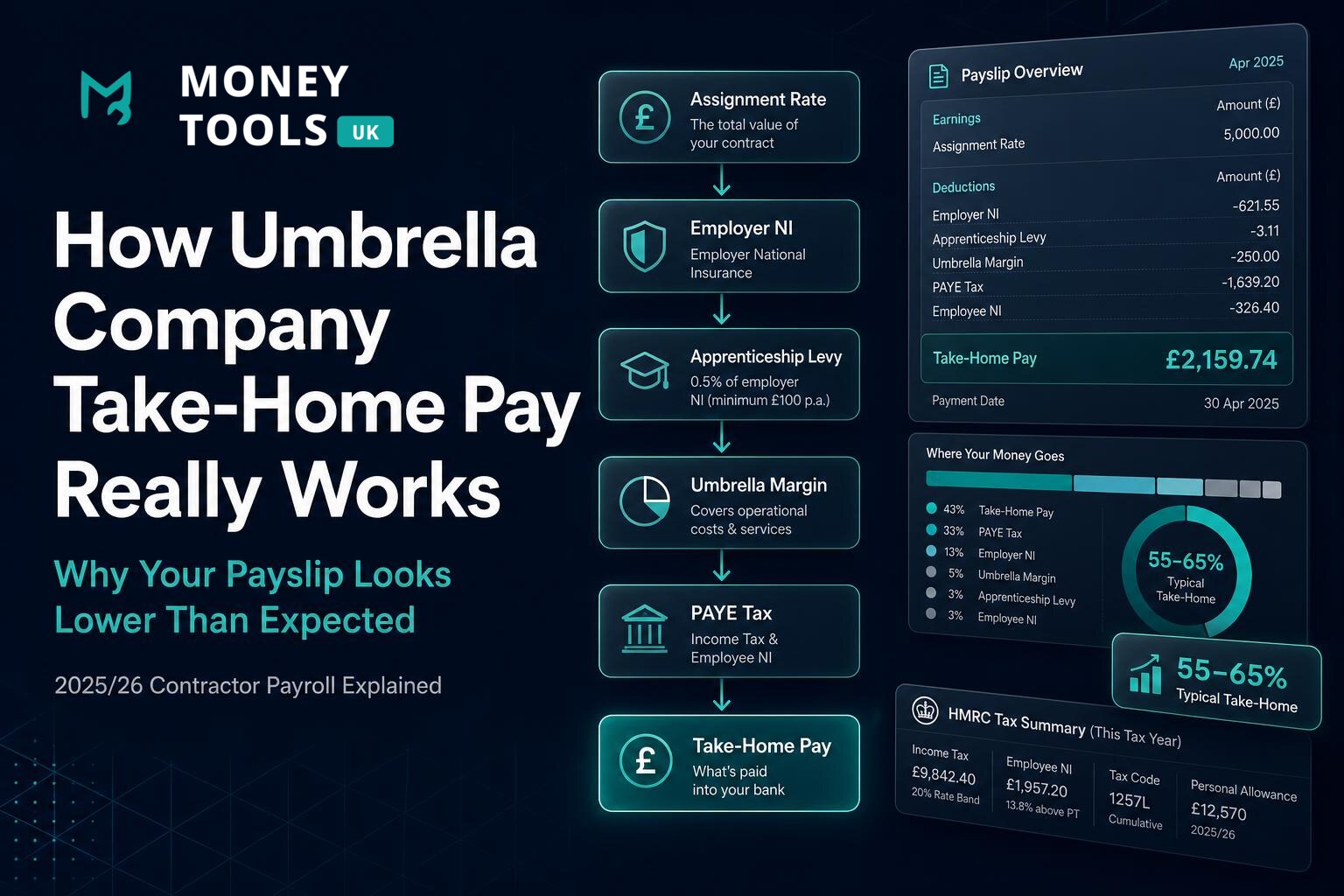

An umbrella company is a third-party employer. The agency pays the umbrella an assignment rate, the umbrella deducts the costs of employing you — employer's NI, the apprenticeship levy and their own margin — and what's left becomes your gross pay. From that gross pay, the umbrella then deducts income tax and employee NI and pays you the net.

You're a permanent employee of the umbrella, so you get the same statutory rights as any other UK employee: holiday pay, SSP, pension auto-enrolment and continuity of employment between contracts.

Two rates, not one

Deductions side by side

Take a £400/day assignment. On agency PAYE you'd typically be offered around £335/day as the headline rate (the agency keeps £65/day to cover employer's NI, apprenticeship levy and their margin). On umbrella, you'd be quoted £400/day, and the umbrella would deduct those same employer costs from your side.

- Employer's NI (13.8% above the secondary threshold): paid by the agency on PAYE, paid out of your assignment rate on umbrella.

- Apprenticeship levy (0.5%): almost always paid out of your assignment rate on umbrella.

- Umbrella margin: typically £15–£30 per week. Doesn't exist on agency PAYE.

- Holiday pay: usually rolled up into the gross on umbrella (12.07%) — visible but yours; accrued separately on agency PAYE.

- Income tax and employee NI: identical on both — same bands, same thresholds, same personal allowance.

Compare the two on your own day rate

Plug your assignment rate into the umbrella calculator to see the full deduction stack and your real net pay.

Take-home pay: which actually wins?

Once you compare like-for-like rates, take-home pay between umbrella and agency PAYE is usually within £20–£40 per week. The umbrella margin is the only structural cost on umbrella that doesn't exist on agency PAYE — everything else (employer's NI, levy, income tax, employee NI) is paid in both cases, just by a different party from the same pot of money.

Where umbrella often pulls ahead is on flexibility: one continuous employment across multiple agencies, easier salary-sacrifice pension contributions, and the ability to roll from one assignment straight into the next without a P45 in between. Where agency PAYE pulls ahead is simplicity: no margin, one payslip from one party, and no risk of choosing a non-compliant umbrella.

Rights and protections

Both routes give you full UK employment rights for tax purposes — you are an employee of either the agency or the umbrella. That means:

- 28 days statutory holiday including bank holidays (pro-rata).

- Statutory Sick Pay if you meet the earnings threshold.

- Pension auto-enrolment, with the option to opt out.

- Statutory maternity, paternity and adoption pay if eligible.

- National Minimum Wage protections.

Continuity of employment is the practical edge umbrella has: because you remain employed by the umbrella between assignments, mortgage lenders generally treat your income as employed PAYE income with continuous service rather than a string of short agency contracts.

When to pick which

Pick agency PAYE if

- You're on a single, short assignment with one agency.

- The role is low day-rate (under ~£200/day) where the umbrella margin eats a meaningful percentage.

- You don't want to think about choosing a compliant umbrella.

Pick umbrella if

- You move between agencies or assignments regularly.

- You want to make significant pension contributions via salary sacrifice.

- You want continuous employment for mortgage or finance applications.

- The role is inside IR35 and your only realistic alternative is umbrella anyway.

Avoid non-compliant umbrellas

How to compare properly

Always ask the agency for both rates: the PAYE rate and the umbrella assignment rate. Then put each into the right calculator. The Umbrella Calculator models the full assignment-rate deduction stack, while the Take-Home Pay Calculator will give you a clean view of the PAYE rate. Compare the net weekly pay, not the headline numbers.

For inside IR35 contracts, the umbrella route is usually the only practical option — see Why inside IR35 take-home is so low for the full picture.

Get new UK finance and property guides from Money Tools UK

Plain-English UK finance insights, tax updates and property investing guides.

Related calculators

Umbrella Company Calculator

The exact calculator this article is built around — open it and run your own numbers.

Open calculatorFrequently asked questions

Related guides

How Umbrella Company Take-Home Pay Really Works (2025/26)Understand every deduction on your umbrella payslip in 2025/26 — employer's NI, employee NI, Income Tax, the Apprenticeship Levy, umbrella margin, pensions and student loans, with worked examples.

How Umbrella Company Take-Home Pay Really Works (2025/26)Understand every deduction on your umbrella payslip in 2025/26 — employer's NI, employee NI, Income Tax, the Apprenticeship Levy, umbrella margin, pensions and student loans, with worked examples. How Much Does an Umbrella Company Actually Cost? (2025/26)See how much an umbrella company really costs in 2025/26, including umbrella margin, Employer's NI, Apprenticeship Levy, holiday pay, pension deductions and contractor take-home pay.

How Much Does an Umbrella Company Actually Cost? (2025/26)See how much an umbrella company really costs in 2025/26, including umbrella margin, Employer's NI, Apprenticeship Levy, holiday pay, pension deductions and contractor take-home pay. Is a £500/Day Contract Worth It After Tax? (2025/26)See how much a £500/day contract could be worth after tax in 2025/26. Compare umbrella company, inside IR35, outside IR35 and limited company take-home pay.

Is a £500/Day Contract Worth It After Tax? (2025/26)See how much a £500/day contract could be worth after tax in 2025/26. Compare umbrella company, inside IR35, outside IR35 and limited company take-home pay.Disclaimer: This content is for informational purposes only and should not be treated as financial, tax, mortgage, investment or legal advice.