A £35,000 salary sits slightly above the UK median full-time wage and lands comfortably inside the basic-rate tax band. It's a salary common among skilled workers, teachers, nurses, technicians, supervisors and junior managers — and the point at which many people start thinking seriously about pensions and longer-term financial planning. This guide shows exactly what £35k looks like on your payslip in the 2025/26 tax year, how much actually reaches your bank account each month, and how pensions and student loans reshape that figure.

Most workers on £35k want to understand the same handful of things: their monthly take-home pay, how much Income Tax and National Insurance is deducted, and how pension contributions or student loan repayments change the final number. We'll cover all of it below — and you can run your own figures any time with the UK Take-Home Pay Calculator.

Quick Facts — £35,000 Salary (2025/26)

Figures assume a standard 1257L tax code with no pension or student loan deductions.

Why £35k is an important salary level

£35,000 is above the UK median full-time salary, placing you in a relatively stable financial position. It's a salary level reached by many teachers, nurses, public-sector workers and early-career professionals — a genuine career milestone that offers meaningful budgeting headroom across most of the UK.

Crucially, £35k is often the point where pension contributions and salary sacrifice begin making a noticeable difference. Because your entire salary sits inside the basic-rate band, every pound you contribute to a pension attracts 20% tax relief, and salary sacrifice can save you National Insurance on top. That makes £35k a practical sweet spot for starting — or increasing — long-term retirement savings without the complexity of higher-rate tax relief claims.

Understanding your exact take-home pay at £35k helps with budgeting, mortgage planning and long-term savings. Whether you're saving for a house deposit, building an emergency fund, or working out how much you can afford to put into your pension each month, knowing your real net pay is the essential first step. You can model your own figures with the UK Take-Home Pay Calculator or explore your borrowing potential with the Mortgage Affordability Calculator. Compared with the £30k salary after tax level, the extra £5,000 of gross pay translates to roughly £300 more in your pocket each month — a meaningful step up in financial flexibility.

Open the UK Take-Home Pay Calculator

Run your salary, pension, student loan and bonus through the calculator for a full payslip-style breakdown in seconds.

Updated for 2025/26

The short answer

The short answer

Annual Take-Home

£28,720

Estimated annual net pay

Monthly Take-Home

£2,393

Approximate monthly pay

Weekly Take-Home

£552

Approximate weekly pay

Effective Tax Rate

17.9%

Effective Income Tax + NI rate

Figures assume a standard tax code with no pension and no student loan deductions.

How much better is £35k than £30k?

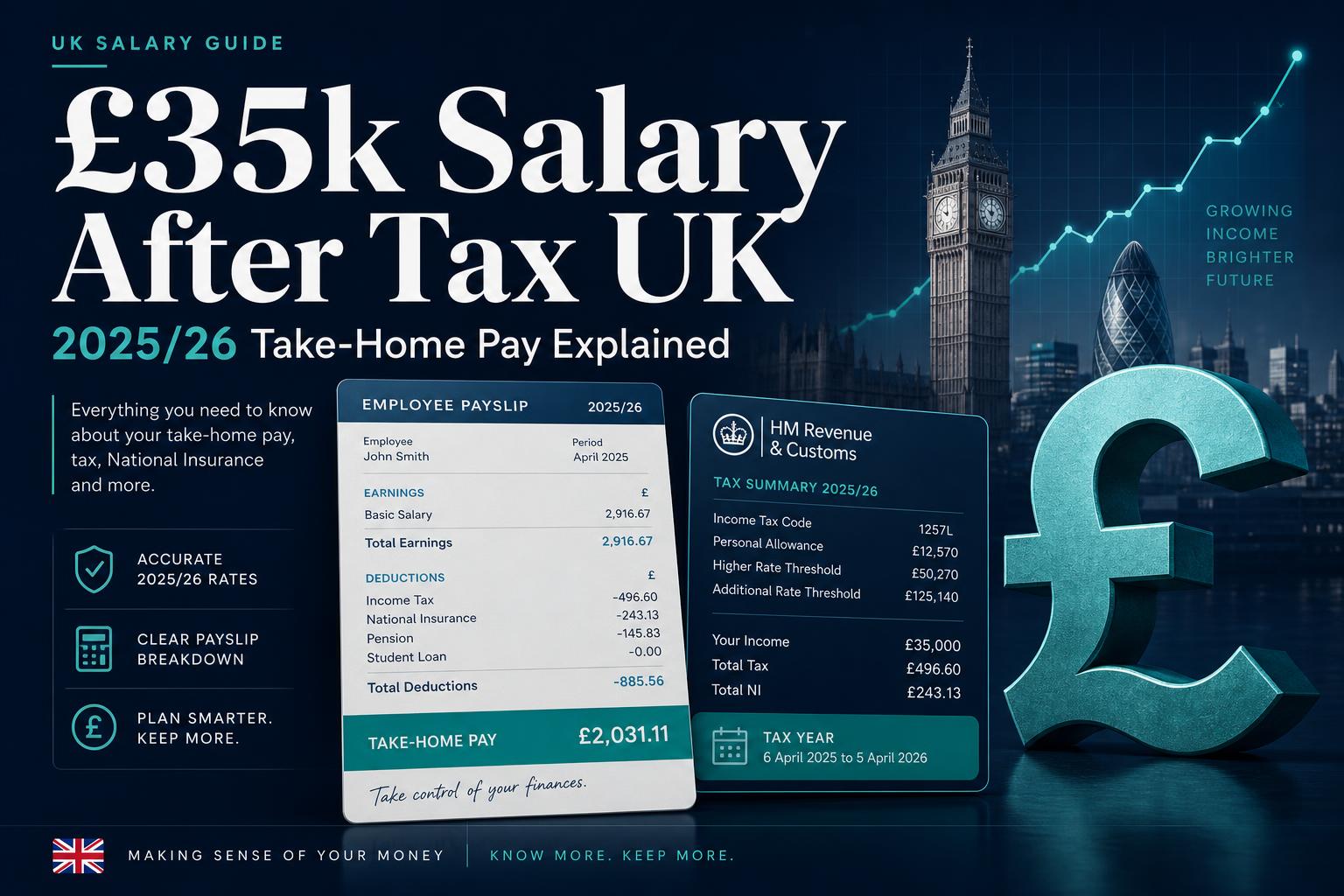

How a £35,000 salary is taxed in 2025/26

For 2025/26, the UK Income Tax thresholds (England, Wales and Northern Ireland) remain frozen. The personal allowance is £12,570 — you pay no Income Tax on this slice at all. The basic-rate band then runs up to £50,270, taxed at 20%. A £35,000 salary sits entirely inside the basic-rate band, so no higher-rate (40%) tax applies.

This is exactly why £35k is considered a relatively tax-efficient salary: every taxable pound is charged at just 20%, and National Insurance stays at the main 8% rate. There are no allowance tapers, higher-rate jumps or 60% traps to worry about — the maths is refreshingly simple.

Income tax on £35,000

Your taxable income is gross salary minus the personal allowance: £35,000 − £12,570 = £22,430. All of that sits inside the basic-rate band:

- Basic rate (20%): £22,430 × 20% = £4,486

- Higher rate (40%): £0 — you're £15,270 below the higher-rate threshold

That's approximately £4,486 in Income Tax for the year, or about £374 a month deducted via PAYE.

National Insurance on £35,000

Employee Class 1 National Insurance for 2025/26 is 8% on earnings between £12,570 and £50,270. On a £35,000 salary:

- NI'able earnings: £35,000 − £12,570 = £22,430

- NI at 8%: £22,430 × 8% = £1,794

So you'll pay around £1,794 in National Insurance across the year — roughly £150 a month.

Putting it together: £35,000 − £4,486 Income Tax − £1,794 NI = £28,720 net pay a year, or about £2,393 a month.

Monthly and weekly take-home pay

Here's the full breakdown of a £35,000 salary in 2025/26 with a standard tax code and no other deductions:

- Gross salary: £35,000

- Income Tax: −£4,486

- National Insurance: −£1,794

- Annual take-home: £28,720

- Monthly take-home: ~£2,393

- Weekly take-home: ~£552

Your effective tax rate — total Income Tax and NI as a share of gross pay — is around 17.9%. In other words, you keep roughly 82p of every pound you earn, which is comparatively light thanks to staying inside the basic-rate band.

What can a £35,000 salary support?

With roughly £2,393 a month landing in your account, a £35k salary can support a comfortable lifestyle across much of the UK — provided you budget thoughtfully. Here is what that typically looks like in practice.

Mortgage borrowing potential

UK lenders typically offer mortgages worth 4–4.5× your annual salary. On £35,000 that means potential borrowing of around £140,000–£157,500, depending on your existing outgoings and credit history. In lower-cost regions, that can cover a starter home; in expensive areas, it usually means a flat or a property as part of a couple. Use the Mortgage Affordability Calculator to see your exact borrowing range.

Monthly budgeting

A common rule of thumb is to spend no more than 30% of net pay on housing — roughly £720/month on £35k. Outside London that comfortably covers a one-bedroom flat or a room in a shared house with money to spare. After rent, typical single-person outgoings (utilities, transport, food, phone, council tax) run around £700–£1,000/month, leaving room for discretionary spending and saving.

Pension contributions

Auto-enrolment means at least 8% of qualifying earnings (including 3% from your employer) goes into your pension. At £35k, increasing your own contribution to 5% of gross salary adds roughly £146/month to your pension while reducing take-home by only about £117–£125/month depending on whether you use relief at source or salary sacrifice. Over a working lifetime, that extra compounding makes a significant difference.

Emergency fund building

Financial advisers typically recommend an emergency fund of 3–6 months of essential expenses. On £35k, three months of bare-bones living costs might be roughly £4,500–£6,000. Saving £200/month from your net pay would build a £4,800 fund in two years — a realistic goal that provides genuine peace of mind if your circumstances change.

Saving for a house deposit

A 10% deposit on a £180,000 property is £18,000. Saving £300/month into a Lifetime ISA attracts a 25% government bonus (up to £1,000/year), meaning your £3,600 annual saving becomes £4,500 with the bonus. At that pace, you could reach £18,000 in roughly four years. If you're buying with a partner who also saves, the timeline halves.

This is guidance, not advice

See your own number in seconds

Model your exact £35k take-home with pension, student loan and bonus options using the UK Take-Home Pay Calculator.

£35k take-home with pension contributions

Pension contributions are the single most effective long-term lever a £35k earner has. How they affect your take-home depends on whether your scheme uses relief at source or salary sacrifice.

5% relief-at-source example

Most workplace pensions use relief at source: contributions come from your net pay and HMRC tops them up by 20%. A 5% contribution on £35k is £1,750/year, which reduces your take-home to around £26,970/year (~£2,248/month). Once the basic-rate top-up is added, roughly £2,188 lands in your pension.

5% salary sacrifice example

With salary sacrifice, the same 5% (£1,750) comes out of your gross salary before tax and NI. You save the 20% Income Tax and the 8% National Insurance, so your take-home only falls to around £27,110/year (~£2,259/month) for the same £1,750 going into your pension. That's roughly £140/year more in your pocket than relief at source — which is why salary sacrifice can effectively increase your net pay for the same level of saving.

If your employer offers salary sacrifice, it's one of the most tax-efficient workplace benefits available. Read our guide to Salary Sacrifice Explained to see exactly how the savings work in practice.

£35k take-home with a student loan

Student loan repayments are deducted via PAYE as a percentage of income above a plan-specific threshold. They don't reduce your tax, but they do shrink your payslip. Here's how a £35,000 salary looks under each plan for 2025/26:

- Plan 1 (started uni before Sept 2012, England/Wales): threshold £26,065, 9%. Annual repayment ≈ £804 (~£67/month) → take-home ~£27,916/year.

- Plan 2 (started 2012–2023, England/Wales): threshold £28,470, 9%. Annual repayment ≈ £588 (~£49/month) → take-home ~£28,132/year.

- Plan 4 (Scotland): threshold £32,745, 9%. Annual repayment ≈ £203 (~£17/month) → take-home ~£28,517/year.

- Plan 5 (started uni from Sept 2023): threshold £25,000, 9%. Annual repayment ≈ £900 (~£75/month) → take-home ~£27,820/year.

- Postgraduate Loan: threshold £21,000, 6%. Annual repayment ≈ £840 (~£70/month) → take-home ~£27,880/year.

If you hold both an undergraduate and a postgraduate loan, both are deducted at the same time — worth budgeting for from day one.

Full payslip comparison at £35k

Here's how the most common scenarios compare for a £35,000 gross salary in 2025/26:

- No pension, no student loan: £28,720/year → £2,393/month

- 5% pension (relief at source): ~£26,970/year → ~£2,248/month

- 5% pension (salary sacrifice): ~£27,110/year → ~£2,259/month

- Plan 2 student loan: ~£28,132/year → ~£2,344/month

- Plan 2 + 5% salary sacrifice: ~£26,522/year → ~£2,210/month

| Scenario | Annual take-home | Monthly take-home |

|---|---|---|

| No pension, no student loan | £28,720 | £2,393 |

| 5% pension (relief at source) | £26,970 | £2,248 |

| 5% pension (salary sacrifice) | £27,110 | £2,259 |

| Plan 2 student loan | £28,132 | £2,344 |

| Plan 2 + salary sacrifice | ~£26,522 | ~£2,210 |

How much more do you take home on £40k?

The extra £5,000 of gross pay is still taxed entirely within the basic-rate band, so most of it lands in your bank account. Here's the side-by-side comparison:

| Metric | £35,000 | £40,000 | Difference |

|---|---|---|---|

| Annual take-home | £28,720 | £32,320 | +£3,600 |

| Monthly take-home | £2,393 | £2,693 | +£300 |

Eyeing a pay rise? Read the full £40k Salary After Tax UK guide for a complete payslip breakdown, pension scenarios and budgeting guidance.

See your exact take-home pay

Run your exact salary, pension, student loan and bonus details through the UK Take-Home Pay Calculator to get a personalised payslip breakdown.

Common mistakes people make at £35k

- Thinking all your salary is taxed. The first £12,570 is tax-free, and only income above that is charged at 20% — your effective rate is closer to 18%, not 20%.

- Ignoring pension tax relief. Opting out of auto-enrolment throws away employer matching and 20% tax relief — the highest guaranteed return you'll ever get.

- Forgetting student loan deductions. Plan 5 quietly takes ~£75/month and Plan 2 ~£49/month before you've seen the money.

- Budgeting from gross pay instead of net pay. A £35k offer is not £2,917/month in your account — the real figure is closer to £2,393/month.

- Not checking workplace pension contribution levels. Many employers match above the 3% minimum, so contributing more can unlock free money you'd otherwise leave on the table.

How to legitimately keep more of your £35k

- Pension contributions. Every contribution gets at least 20% basic-rate tax relief, and capturing employer matching is the highest guaranteed return available.

- Salary sacrifice. Where offered, it saves both Income Tax and National Insurance — see Salary Sacrifice Explained.

- Marriage Allowance. If your partner earns under £12,570, they can transfer £1,260 of allowance to you, worth up to £252 a year.

- Cycle-to-work schemes. Buy a bike and equipment from pre-tax salary, cutting tax and NI on something you'd buy anyway.

- Gift Aid. Charitable donations are made from taxed income, so make sure you claim Gift Aid and keep records.

Want your exact take-home pay?

Use the UK Take-Home Pay Calculator to include:

- pension contributions

- student loans (Plan 1, 2, 4, 5 and Postgraduate)

- bonuses

- salary sacrifice

- benefits-in-kind

- side income

See your exact take-home pay

Run your exact salary, pension, student loan and bonus details through the UK Take-Home Pay Calculator to get a personalised payslip breakdown.

Related guides

- £30k Salary After Tax UK — the step below, also fully inside the basic-rate band.

- £40k Salary After Tax UK — the next major milestone, still inside the basic-rate band.

- Salary Sacrifice Explained — how to cut tax and NI while boosting your pension.

- UK Take-Home Pay Calculator — model your exact £35k take-home in seconds.

Sources & references

This guide references current HMRC and GOV.UK guidance for the 2025/26 UK tax year.

- HMRC — Income Tax rates and Personal Allowances

- HMRC — National Insurance: how much you pay

- Student Loans Company — Repaying your student loan: what you pay

- GOV.UK — Salary sacrifice guidance for employers

Last updated

This article was last reviewed on 26 May 2026 and reflects the UK tax thresholds, National Insurance rates and student loan plans confirmed for the 2025/26 tax year. We refresh this guide each time HMRC publishes a material change.

Disclaimer

Money Tools UK provides educational content and calculators only. The figures above are estimates based on standard 2025/26 UK tax rules for England, Wales and Northern Ireland (with Scottish rates noted where relevant) and assume a single PAYE employment and a standard 1257L tax code. They do not account for benefits in kind, taxable expenses, pension annual-allowance limits, or personal circumstances that may change your actual liability. For regulated tax or financial advice, please speak to a qualified accountant or independent financial adviser.

Get new UK finance and property guides from Money Tools UK

Plain-English UK finance insights, tax updates and property investing guides.

Related Salary Guides

Explore nearby salary levels to compare take-home pay, Income Tax, National Insurance, student loan deductions and pension contributions.

Related calculators

UK Take-Home Pay Calculator

The exact calculator this article is built around — open it and run your own numbers.

Open calculatorFrequently asked questions

Related guides

More flagship guides and tools from Money Tools UK.

A plain-English UK guide to checking if HMRC owes you a tax refund: why overpayments happen, how to use your Personal Tax Account, P800 and Simple Assessment, when refunds are automatic, how to claim, and how to avoid tax refund scams.

Read guide

Why HMRC overtaxes pension withdrawals with emergency tax, how pension tax refunds work, and which form to use — P55, P53Z, P50Z or P53 — to reclaim overpaid tax for 2025/26.

Read guide

Learn how UK company car tax works in 2025/26, including Benefit-in-Kind tax, P11D value, CO2 emissions, electric cars, fuel benefit and salary sacrifice examples.

Read guideDisclaimer: This content is for informational purposes only and should not be treated as financial, tax, mortgage, investment or legal advice.