Why it happens

Emergency tax

Can you reclaim?

Usually yes

Typical refund time

~30 days

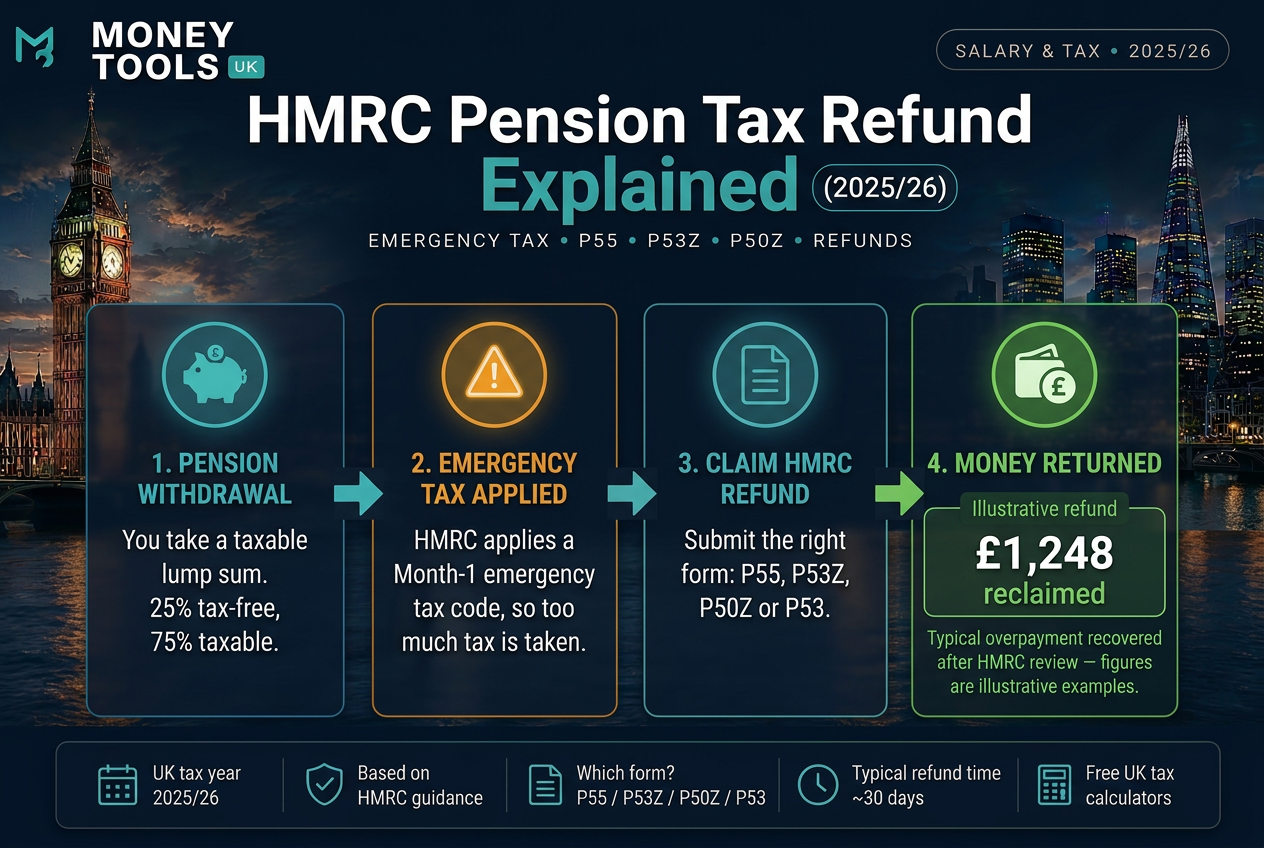

HMRC often deducts too much tax from your first pension withdrawal. The good news: if you have been overtaxed, you can usually claim the money back — and the right form (P55, P53Z, P50Z or P53) depends on your exact situation.

If you have taken money out of a pension for the first time and the tax looked frighteningly high, you are not alone. HMRC frequently applies an emergency tax code to the first flexible pension withdrawal, which can lead to hundreds or even thousands of pounds of tax being deducted that you may not actually owe. This is one of the most common — and most misunderstood — quirks of the UK pension freedoms system.

The reassuring part is that an HMRC pension tax refund is a normal, well-established process. HMRC expects these overpayments to happen and provides specific reclaim forms to get your money back quickly. This guide explains, in plain English, why the overtaxation happens, how emergency tax on pensions works, and exactly which refund route — P55, P53Z, P50Z or P53 — applies to you.

Everything here reflects HMRC guidance for the 2025/26 tax year. Figures in worked examples are illustrative, and this guide is educational rather than personal tax advice.

The quick answer

When you take a taxable lump sum from a defined contribution pension, your pension provider usually has no up-to-date tax code for that payment, so HMRC tells them to apply an emergency tax code on a “Month 1” basis. This treats a one-off payment as if you will receive it every month for a year, so far too much tax is deducted.

Key point

If you have been overtaxed, you can reclaim the money. Use P55 if you took only part of your pot, P53Z if you emptied the whole pot and still have other income, and P50Z if you emptied the whole pot and have no other income. P53 covers small pots and trivial commutation lump sums. Refunds are typically paid within about 30 days.

Why HMRC overtaxes pension withdrawals

Since the pension freedoms were introduced in April 2015, most people aged 55 or over (rising to 57 from 2028) can access a defined contribution pension flexibly. You can normally take 25% of your pot tax-free, with the remaining 75% taxed as income when you withdraw it.

The problem is not the tax rules themselves — it is the tax code used at the moment of your first withdrawal. When your provider makes a flexible payment, they generally do not hold a current cumulative tax code for you. HMRC instructs them to use an emergency tax code instead, and to apply it on a non-cumulative “Month 1” basis.

- No P45 for the payment — the provider has nothing telling them how much of your allowances you have already used.

- Emergency code applied — you get only a slice of your personal allowance against that single payment.

- Payment annualised — the system assumes the same amount will be paid every month, pushing a one-off lump sum into higher tax bands.

What GOV.UK says

How emergency tax on pensions works

In short: emergency pension tax is a temporary overpayment that happens when your provider has no up-to-date tax code for your first flexible withdrawal, so HMRC tells them to apply an emergency code. It is not a penalty or a higher rate — and the excess is reclaimable.

Emergency tax is not a penalty and it is not a special higher rate of tax. It is simply what happens when the payroll system does not have enough information about your income, so it errs on the side of deducting more rather than less. With pensions, this most often affects the very first taxable withdrawal.

How a pension withdrawal gets overtaxed

What the Month-1 basis actually does

In short: the Month-1 (non-cumulative) basis taxes a payment as if it were just one month’s income. You get only 1/12 of your personal allowance and 1/12 of each tax band against that payment, which pushes much of a one-off lump sum into higher tax bands.

The Month-1 basis is the single biggest reason pension withdrawals look so heavily taxed. Instead of looking at your income for the whole year, it treats the payment as if it were one month’s worth of a much larger annual income.

In practice, that means for a single taxable payment you only get:

- 1/12 of your personal allowance (roughly £1,048 of tax-free income for that payment in 2025/26, based on the standard £12,570 allowance).

- 1/12 of the basic-rate band before higher-rate tax starts to apply.

- 1/12 of the higher-rate band before additional-rate tax applies.

Because a lump sum is usually far bigger than one month’s income, large chunks of it are pushed into the 40% and even 45% bands — even though your actual annual income might keep you firmly in the basic-rate band. That gap between the tax deducted and the tax you truly owe is what you reclaim.

This is why the deduction looks alarming

Worked example: a £30,000 withdrawal

The figures below are illustrative only and use the standard 2025/26 personal allowance and England, Wales and Northern Ireland tax bands. They show the principle rather than your exact outcome.

Sarah takes a £30,000 taxable lump sum

| £30,000 taxable withdrawal | Emergency Month-1 basis | Tax Sarah actually owes* |

|---|---|---|

| Tax-free slice applied | 1/12 of allowance (~£1,048) | Full unused allowance |

| Bands used | Mostly 40%, some 45% | Mostly 20% (if a basic-rate taxpayer) |

| Approximate tax deducted | ~£11,000 | ~£6,000 |

| Reclaimable difference | ~£5,000 potentially refundable | |

*Sarah’s real tax bill depends on her other income for the year. The point is the direction of travel: the emergency deduction is far higher than the tax genuinely due, and the difference is what a pension tax refund returns to her.

Money Tools UK tip

Who is most likely to be overtaxed?

Emergency tax can affect almost anyone taking a flexible pension payment for the first time, but the impact is largest for:

- People taking a big one-off lump sum — the larger the payment, the more of it is forced into higher bands under Month-1.

- Basic-rate taxpayers — the gap between the emergency deduction and the tax actually owed is often widest here.

- People with little or no other income — much of the personal allowance is unused, so more tax is reclaimable.

- Anyone making their first flexible withdrawal in a tax year — before HMRC has issued the provider a correct code.

Real-life scenarios

These short, illustrative examples show how emergency tax and the reclaim route change depending on your situation. Figures are examples only and depend on your total income for the year.

First withdrawal, still working

Priya, 58, takes a one-off £8,000 taxable payment but keeps her salary and most of her pot. An emergency Month-1 code overtaxes the payment. Because she left money invested, she reclaims the excess with a P55 and gets it back in about a month.

Just retired, no other income

David, 66, has stopped work and empties his small remaining pot as one lump sum. With no other taxable income for the rest of the year, much of his allowance is unused, so he claims with a P50Z and recovers a large share of the tax deducted.

Made redundant, other income continues

Marcus, 60, is made redundant and withdraws his entire pot to tide him over, but still receives another workplace pension. Because he has other taxable income, the correct reclaim form is a P53Z, which uses that income to work out the refund.

Small pot taken as cash

Anne, 57, cashes in a small, low-value pension as a lump sum and sees emergency tax deducted. Because this is a small-pot payment rather than a flexible-access withdrawal, she reclaims using a P53.

How pension tax refunds work

How long do pension tax refunds take? If you claim actively with the right HMRC form, refunds are typically paid within about 30 days. If you do nothing, HMRC reconciles your tax automatically after the tax year ends, which can take several months.

A pension tax refund simply returns the difference between the tax deducted under the emergency code and the tax you actually owe. There are two routes:

- Claim it now — complete the relevant HMRC form (P55, P53Z, P50Z or P53). HMRC aims to process refunds within around 30 days.

- Do nothing and wait — HMRC automatically reconciles your tax after the end of the tax year and sends any refund due, but this can take several months.

Money Tools UK tip

P55, P53Z, P50Z and P53 compared

The form you need depends on two questions: did you take only part of your pot or empty it completely? and do you have other taxable income this year?

| Form | Use it when… | Pot status | Other income? |

|---|---|---|---|

| P55 | You took a flexible payment but are not taking regular withdrawals and your provider cannot refund you. | Partly used — money still left in the pot | Any |

| P53Z | You emptied your whole pot as a lump sum and still receive other taxable income (job, other pension, taxable benefits). | Fully emptied | Yes |

| P50Z | You emptied your whole pot as a lump sum and have no other taxable income for the rest of the tax year. | Fully emptied | No |

| P53 | You took a small pension pot or a trivial commutation lump sum and were overtaxed. | Small pot / trivial commutation | Any |

Check before you file

P55: part of your pot, still invested

Use P55 when you have taken a flexible one-off payment from your pension, you are not taking regular payments, you have not emptied the whole pot, and your pension provider cannot refund the overpaid tax for you. This is the most common form for someone who dipped into their pension once and left the rest invested.

P53Z: whole pot emptied, other income

Use P53Z when you have withdrawn your entire pension pot as a lump sum and you still have other taxable income this tax year — for example a salary, another pension in payment, or taxable state benefits. HMRC uses your other income to work out the correct tax and refunds the excess.

P50Z: whole pot emptied, no other income

Use P50Z when you have emptied your whole pension pot as a lump sum and you have no other taxable income for the rest of the tax year — for example if you have stopped working and are not yet drawing any other taxable income. Because more of your personal allowance is unused, the refund can be substantial.

P53: small pots and trivial commutation

Use P53 when you have taken a small pension pot lump sum or a trivial commutation lump sum (typically small, low-value pensions taken as cash) and too much tax was deducted. This is a separate route from the flexible-access forms above.

Which form should you use? Decision tree

Step 1 — Was it a small pot or trivial commutation?

If yes → use P53. If no, go to Step 2.

Step 2 — Did you empty the whole pot?

If no (money still left, no regular payments) → use P55. If yes, go to Step 3.

Step 3 — Do you have other taxable income this year?

If yes → use P53Z. If no → use P50Z.

Refund route at a glance

How to claim your refund step by step

Your refund checklist

- ✓Confirm you were overtaxed — compare the tax deducted with the tax you actually owe for the year

- ✓Identify the right form using the decision tree (P55, P53Z, P50Z or P53)

- ✓Gather details of the payment, your provider and any other income for the year

- ✓Complete the form online with a Government Gateway account, or by post

- ✓Submit to HMRC and keep a copy of your reference

- ✓Wait for the refund — HMRC aims to process claims within about 30 days

You can complete the forms on GOV.UK using a Government Gateway account, or download and post them. HMRC pays the refund directly to you or to a nominated bank account.

Sense-check the tax you should really pay

Use the Money Tools UK Take-Home Pay Calculator to see how your income is taxed across the 2025/26 bands, so you can gauge whether a pension withdrawal has been overtaxed.

What happens if you do nothing?

You are not required to submit a reclaim form. If you do nothing, HMRC will normally reconcile your tax automatically after the end of the tax year and send any refund due, often via a P800 tax calculation. However, this can take several months, and you are effectively lending HMRC your money in the meantime. For most people who have clearly overpaid, claiming actively is the better option.

How to avoid being overtaxed in the first place

- Take a small first withdrawal — a modest initial payment can trigger HMRC to issue your provider a correct tax code before you take the bulk of your money.

- Spread larger withdrawals — taking income in stages across tax years can keep more of it in lower bands and reduce emergency-tax shocks.

- Check your tax code — once your provider has an updated code, later payments in the same tax year are usually taxed correctly.

- Mind the £100k taper and higher bands — a big taxable withdrawal can push your income into higher-rate tax or the personal allowance taper. See our personal allowance taper guide.

Money Tools UK tip

Common mistakes to avoid

Assuming the deduction is correct

Emergency tax on a first withdrawal is frequently too high. Always check before accepting it as final.

Using the wrong form

P55, P53Z, P50Z and P53 are not interchangeable. Using the wrong one can delay your refund.

Forgetting other income

Whether you have other taxable income decides between P53Z and P50Z — and affects the refund amount.

Taking a huge lump sum first

A large first withdrawal maximises the emergency overpayment. A small test payment first can avoid it.

Money Tools UK warning

What should I do next?

Money Tools UK summary

- Why: HMRC applies an emergency Month-1 tax code to your first flexible pension withdrawal, usually overtaxing it.

- Fix: reclaim the overpayment with the right form — P55, P53Z, P50Z or P53.

- Speed: active claims are typically paid within about 30 days; doing nothing means waiting for year-end reconciliation.

- Avoid it: take a small first withdrawal, spread income across tax years, and check your tax code.

The key lesson is reassuring: a frightening tax deduction on your first pension withdrawal is usually temporary, not final. Emergency tax is a quirk of how the payroll system handles a one-off payment, and HMRC fully expects these overpayments to be put right. Once you know which form fits your situation, reclaiming the money is a straightforward, well-trodden process.

Before you draw on your pension, sense-check the tax you should really pay, choose the correct HMRC form for your circumstances, and keep a copy of your claim reference. Then explore the related Money Tools UK calculators and guides below to plan your withdrawals with confidence and keep more of your retirement income where it belongs — with you.

Plan your withdrawals with confidence

Model how income is taxed across the 2025/26 bands before you draw on your pension, so a big withdrawal doesn't tip you into higher-rate tax unexpectedly.

Related guides

These Money Tools UK guides explain the tax rules that most often affect pension withdrawals and retirement planning.

- Salary Sacrifice Explained — how pension contributions reduce the tax you pay now.

- The Personal Allowance Taper Explained — how a large withdrawal can erode your allowance above £100k.

- How Bonuses Are Taxed in the UK — why one-off payments are often overtaxed at first, just like pensions.

- Adjusted Net Income Explained — the income measure behind allowances and charges.

- Marriage Allowance Explained — a simple way some couples reduce their tax bill.

Related calculators

- Take-Home Pay Calculator — see how income is taxed across the 2025/26 bands.

- Salary to Hourly Calculator — convert income figures when planning your retirement budget.

- Budget Planner — plan monthly income and outgoings around a pension withdrawal.

- Student Loan Calculator — check how repayments interact with taxable income.

Sources & references

This guide reflects official UK government and HMRC guidance on pension freedoms, emergency tax on pension withdrawals and pension tax refund claims for the 2025/26 tax year.

- GOV.UK — Claim back tax on a flexibly accessed pension overpayment (P55)

- GOV.UK — Claim a tax refund when you've flexibly accessed all of your pension (P53Z)

- GOV.UK — Claim back tax when you've stopped work and flexibly accessed all your pension (P50Z)

- GOV.UK — Claim a tax refund if you've taken a small pension lump sum (P53)

- GOV.UK — Claim a tax refund

- GOV.UK — Tax when you get a pension

- GOV.UK — Income Tax rates and Personal Allowances

- GOV.UK — Tax codes: emergency tax codes

Last updated

This article was last reviewed on 7 July 2026 and reflects UK pension freedoms, emergency tax and pension tax refund rules (P55, P53Z, P50Z and P53) for the 2025/26 tax year. We refresh this guide each time HMRC publishes a material change.

Reviewed by Money Tools UK Editorial Team

This guide was reviewed for accuracy against HMRC and GOV.UK guidance on pension withdrawals, emergency tax and tax refund claims for the 2025/26 tax year. We regularly update our tax content when thresholds, rates or forms change.

Last reviewed: 7 July 2026

Disclaimer

Money Tools UK provides educational information and calculators only. This article is not tax, accounting, legal or financial advice, and it does not promise a refund. Pension tax treatment depends on your income, the size and type of withdrawal, your provider’s processes and your personal circumstances. Always check current HMRC guidance and speak to a qualified accountant or regulated financial adviser before making pension decisions.

Get new UK finance and property guides from Money Tools UK

Plain-English UK finance insights, tax updates and property investing guides.

Related calculators

Take-Home Pay Calculator

The exact calculator this article is built around — open it and run your own numbers.

Open calculatorFrequently asked questions

Related guides

Disclaimer: This content is for informational purposes only and should not be treated as financial, tax, mortgage, investment or legal advice.