Taxed as

Benefit-in-Kind

Driven by

CO2 & P11D

BIK capped at

37%

A company car is rarely "free" — it is taxed on the value of private use. This guide explains exactly how Benefit-in-Kind tax is calculated, why electric cars are so much cheaper to tax, and what to check before you accept a company car or salary sacrifice deal.

A company car can feel like a valuable workplace benefit — but it can also create a surprisingly large tax bill. In the UK, company cars are usually taxed as a Benefit-in-Kind when they are available for private use, including commuting.

The amount of tax you pay depends on the car's list price, CO2 emissions, fuel type, electric range, your income tax band and whether your employer also provides private fuel. These factors combine into a single taxable figure that is added to your income and taxed at your marginal rate.

This guide explains how company car tax works in the 2025/26 tax year, how Benefit-in-Kind tax is calculated, why electric cars are usually much cheaper to tax, how fuel benefit works, and what to check before accepting a company car or salary sacrifice car.

The short answer

- When do you pay it?

- Company car tax is usually paid when your employer provides a car that you can use privately, including commuting. The taxable value is called a Benefit-in-Kind.

- The basic formula

- Company Car Tax = P11D value × BIK percentage × your Income Tax rate.

- Why electric wins

- Electric cars usually have much lower Benefit-in-Kind percentages than petrol or diesel cars, which is why they are often significantly cheaper for employees.

What is company car tax?

Company car tax is not a separate tax. It is Income Tax charged on the value of a workplace benefit. HMRC treats the private use of an employer-provided car as a "benefit in kind" — something of value you receive on top of your salary.

If your employer gives you access to a car and you can use it privately, HMRC puts a cash value on that private use and adds it to your taxable income. You then pay your normal rate of Income Tax on that value.

Commuting usually counts as private use

When do you pay company car tax?

You normally pay company car tax if all of the following apply:

- Your employer provides a car for you to use.

- It is available for private use, not just business journeys.

- You or your family can use it outside business travel.

- You commute in it between home and a permanent workplace.

- The employer reports it through payroll or on a P11D.

Genuine pool cars are different

How Benefit-in-Kind tax works

The taxable value of the company car benefit depends on several factors working together:

- The car's P11D value — broadly its list price when new.

- CO2 emissions — the main driver of the BIK percentage.

- Fuel type — petrol, diesel, hybrid or electric.

- Electric range for plug-in hybrids — a longer electric-only range usually means a lower percentage.

- How long the car was available to you during the tax year.

- Any employee contribution you pay towards private use.

- Your marginal tax rate — 20%, 40% or 45%.

The company car tax formula

Step 1 — the taxable benefit

Company Car Benefit = P11D value × BIK percentage

Step 2 — the tax you pay

Company Car Tax Payable = Company Car Benefit × Income Tax rate

Here is a simple worked example using the formula:

- P11D value: £40,000

- BIK percentage: 25%

- Taxable benefit: £40,000 × 25% = £10,000

- Basic-rate (20%) taxpayer: £10,000 × 20% = £2,000 tax per year

- Higher-rate (40%) taxpayer: £10,000 × 40% = £4,000 tax per year

Check How a Company Car Affects Your Take-Home Pay

Use our free UK Take-Home Pay Calculator to estimate Income Tax, National Insurance, student loan deductions and pension contributions — and see how a workplace benefit may affect your tax position.

What is P11D value?

P11D value is usually the car's list price when new, including VAT and certain accessories — not necessarily what your employer actually paid, and not what the car is worth now.

This catches a lot of people out, because the figure that drives your tax bill can be much higher than the deal your employer negotiated.

- Discounts do not usually reduce the P11D value — even a heavily discounted car is taxed on its full list price.

- Second-hand value does not reduce the benefit — depreciation is ignored for company car tax.

- Optional extras can increase the figure — fitted accessories above a small threshold are added on.

The list price is what matters

CO2 emissions and BIK percentage

The BIK percentage is largely driven by CO2 emissions and fuel type. The more a car emits, the higher the percentage of its P11D value that becomes taxable.

- Higher-emission cars usually have higher taxable percentages.

- Low-emission and electric cars are treated far more favourably.

For cars with 75g/km CO2 or above, company car tax percentages increased by 1 percentage point for 2025/26 and are capped at 37%, according to GOV.UK guidance. So even the most polluting cars cannot be taxed on more than 37% of their P11D value.

Electric cars and plug-in hybrids

Electric cars usually have the lowest BIK percentages of any vehicle type, which is the main reason fully electric company cars are so popular — the taxable benefit is small relative to the car's value.

Plug-in hybrids are more complicated. Their BIK percentage depends heavily on:

- CO2 emissions — lower emissions mean a lower percentage.

- Electric-only range — a longer zero-emission range usually means a lower percentage.

- Registration details — the rules can differ depending on when and how the car is registered.

- Whether the car qualifies under the relevant low-emission rules.

Electric vehicles can be very tax-efficient when provided through salary sacrifice, but the total cost must still be compared with cash salary, charging costs, insurance, mileage and your personal circumstances before you decide.

Diesel cars and fuel type rules

Diesel cars may be treated differently from petrol cars depending on their emissions and whether they meet the Euro 6d standard. Older or non-compliant diesels can attract a surcharge that increases the taxable percentage.

GOV.UK says employers should use fuel type "F" for diesel cars that meet the Euro 6d standard, and "D" for other diesel cars, when using the HMRC company car tax calculator. The fuel type you enter directly affects the BIK percentage applied.

Check the fuel type code

Company car fuel benefit

If your employer also pays for fuel used on private journeys, there may be a separate fuel benefit charge on top of the car benefit. This is calculated using a fixed multiplier and the same BIK percentage as the car.

- Car fuel benefit is often expensive unless you do a large amount of private mileage.

- Many employees are better off paying for private fuel themselves and claiming only business mileage, depending on the car and usage.

Fuel cards can be costly

Worked examples

These examples show how the same formula produces very different bills depending on the car and your tax band. Figures are illustrative and rounded to show the principle.

Example A — electric company car

- P11D value: £45,000

- BIK percentage: a low EV rate (around 3%)

- Taxable benefit: £45,000 × 3% = £1,350

- Basic-rate taxpayer: £1,350 × 20% ≈ £270 a year

- Higher-rate taxpayer: £1,350 × 40% ≈ £540 a year

Example B — petrol company car

- P11D value: £35,000

- BIK percentage: a mid-to-high rate (around 30%)

- Taxable benefit: £35,000 × 30% = £10,500

- Basic-rate taxpayer: £10,500 × 20% ≈ £2,100 a year

- Higher-rate taxpayer: £10,500 × 40% ≈ £4,200 a year

Example C — higher-emission diesel car

- P11D value: £40,000

- BIK percentage: a high rate near the 37% cap

- Taxable benefit: £40,000 × 37% = £14,800

- Higher-rate taxpayer: £14,800 × 40% ≈ £5,920 a year

- Why it's expensive: a high P11D value combined with a near-maximum BIK percentage produces one of the largest possible bills.

Example D — company car with fuel benefit

- Petrol car (Example B): car benefit tax of around £4,200 a year for a higher-rate taxpayer.

- Plus fuel benefit: the same 30% BIK percentage applied to the fixed fuel benefit multiplier adds a further taxable amount, often £2,000–£3,000+ of tax depending on the year's figures.

- Total: the combined car and fuel benefit can easily exceed £6,000–£7,000 of tax a year — rarely worthwhile unless private mileage is very high.

Example E — salary sacrifice EV

- Lower salary: you give up part of your gross pay in exchange for the car.

- Company car benefit: you pay BIK tax, but at the low EV percentage the taxable benefit is small.

- Potential tax savings: the sacrificed salary avoids Income Tax and National Insurance, often making the net cost lower than leasing privately.

- Reduced take-home pay: your monthly net pay falls because gross salary is lower.

- Affordability considerations: a lower gross salary can affect pension contributions and mortgage borrowing — weigh these before committing.

The key takeaway

Company car vs car allowance

Some employers let you choose between a company car and a cash car allowance paid as extra salary. The right choice depends on the car you'd pick, your tax band and how you value convenience.

| Feature | Company car | Car allowance |

|---|---|---|

| Who chooses the car | Employer (from a list) | Employee |

| Maintenance & insurance | Often included | Your responsibility |

| How it's taxed | BIK tax on private use | Income Tax + National Insurance as salary |

| Best for | Efficient for EVs | Flexibility & cheaper cars |

| Effect on pension | No change to salary | May affect pensionable pay (employer rules vary) |

A common mistake is comparing the company car against the gross allowance. Always compare against the net allowance — what's left after Income Tax and National Insurance — because that's the cash you actually have to run your own car.

Salary sacrifice and company cars

A salary sacrifice car scheme means giving up part of your gross salary in exchange for a car benefit. This can be tax-efficient for electric vehicles because:

- Salary is reduced before tax and NI, so you save Income Tax and National Insurance on the sacrificed amount.

- The EV company car BIK rate is relatively low, so the taxable benefit is small.

- Your employer may include insurance, servicing and maintenance in the package.

Weigh the trade-offs first

- Salary Sacrifice Explained — how the wider mechanics work.

- Adjusted Net Income Explained — how sacrifice can change your tax position.

- £100k Salary After Tax UK — take-home pay at £100,000.

- £120k Salary After Tax UK — take-home pay at £120,000.

Common mistakes

- Assuming a company car is free — it's a taxable benefit, not a perk with no cost.

- Ignoring the P11D value — this, not the lease price, drives the tax.

- Using the discounted lease price instead of the full list price.

- Forgetting fuel benefit — free private fuel is a separate, often expensive charge.

- Not checking CO2 emissions — they directly set the BIK percentage.

- Assuming all hybrids are cheap to tax — only those with low emissions and long electric range are.

- Ignoring your marginal tax rate — the same car costs a higher-rate taxpayer twice as much.

- Not checking how the benefit affects your tax code.

- Comparing the car against the gross allowance instead of the net allowance.

- Forgetting salary sacrifice can reduce pensionable salary.

How to reduce company car tax legally

- Choose a lower-emission car to bring down the BIK percentage.

- Consider a fully electric car for the lowest available rates.

- Avoid private fuel benefit unless your private mileage is genuinely high.

- Make private-use contributions where appropriate, which can reduce the taxable benefit.

- Compare car allowance vs company car on a net basis before deciding.

- Check salary sacrifice carefully — model the impact on pay, pension and borrowing.

- Keep business and private mileage records in case HMRC asks.

- Update HMRC if your car or fuel details change, so your tax code stays correct.

Finally, look at company car tax UK as part of your wider tax planning rather than in isolation. The Benefit-in-Kind value of the car adds to your taxable income, so it interacts with other reliefs and thresholds. If you are married or in a civil partnership, for example, it is worth checking whether you also qualify for Marriage Allowance, which can transfer part of one partner's Personal Allowance to the other and reduce your overall tax bill alongside any company car decision.

Check how a company car affects your take-home pay

Use the Money Tools UK Take-Home Pay Calculator to model salary, pension contributions, student loans and benefits so you can understand how workplace benefits may affect your tax position.

Related guides

Company car tax is one piece of the wider UK tax picture. These guides help you understand how salary, benefits and take-home pay fit together.

- Salary Sacrifice Explained — cut Income Tax and National Insurance with sacrifice, including a salary sacrifice car scheme.

- Adjusted Net Income Explained — the hidden number that controls your tax bill.

- Child Benefit Tax Charge Explained — how higher income can claw back Child Benefit.

- Marriage Allowance Explained — transfer Personal Allowance between partners to cut tax.

- £100k Salary After Tax UK — take-home pay and the 60% tax trap.

- £120k Salary After Tax UK — take-home pay inside the allowance taper.

- How Bonuses Are Taxed in the UK — Income Tax, NI and take-home pay.

Sources & references

This guide reflects official UK government and HMRC guidance on company cars and Benefit-in-Kind tax for the 2025/26 tax year.

- GOV.UK — Tax on company benefits: company cars

- GOV.UK — Calculate tax on employees' company cars

- GOV.UK — Check or update your company car tax

- GOV.UK — Company car tax appropriate percentages (2025 to 2026)

- HMRC — P11D working sheet 2: car and car fuel benefit

Last updated

This article was last reviewed on 18 June 2026 and reflects UK company car tax, Benefit-in-Kind and HMRC company car rules for the 2025/26 tax year. We refresh this guide each time HMRC publishes a material change.

Reviewed by Money Tools UK Editorial Team

This guide was reviewed for accuracy against HMRC and GOV.UK guidance for the 2025/26 tax year. We regularly update our salary and tax content when thresholds, percentages or eligibility rules change.

Last reviewed: 18 June 2026

Disclaimer

Money Tools UK provides educational content and calculators only. Figures are estimates based on standard 2025/26 UK tax rules and assume eligibility conditions are met. Individual circumstances vary. For regulated tax or financial advice, please speak to a qualified accountant or independent financial adviser.

Get new UK finance and property guides from Money Tools UK

Plain-English UK finance insights, tax updates and property investing guides.

Related calculators

UK Take-Home Pay Calculator

The exact calculator this article is built around — open it and run your own numbers.

Open calculatorFrequently asked questions

Related guides

More flagship guides and tools from Money Tools UK.

A plain-English UK guide to checking if HMRC owes you a tax refund: why overpayments happen, how to use your Personal Tax Account, P800 and Simple Assessment, when refunds are automatic, how to claim, and how to avoid tax refund scams.

Read guide

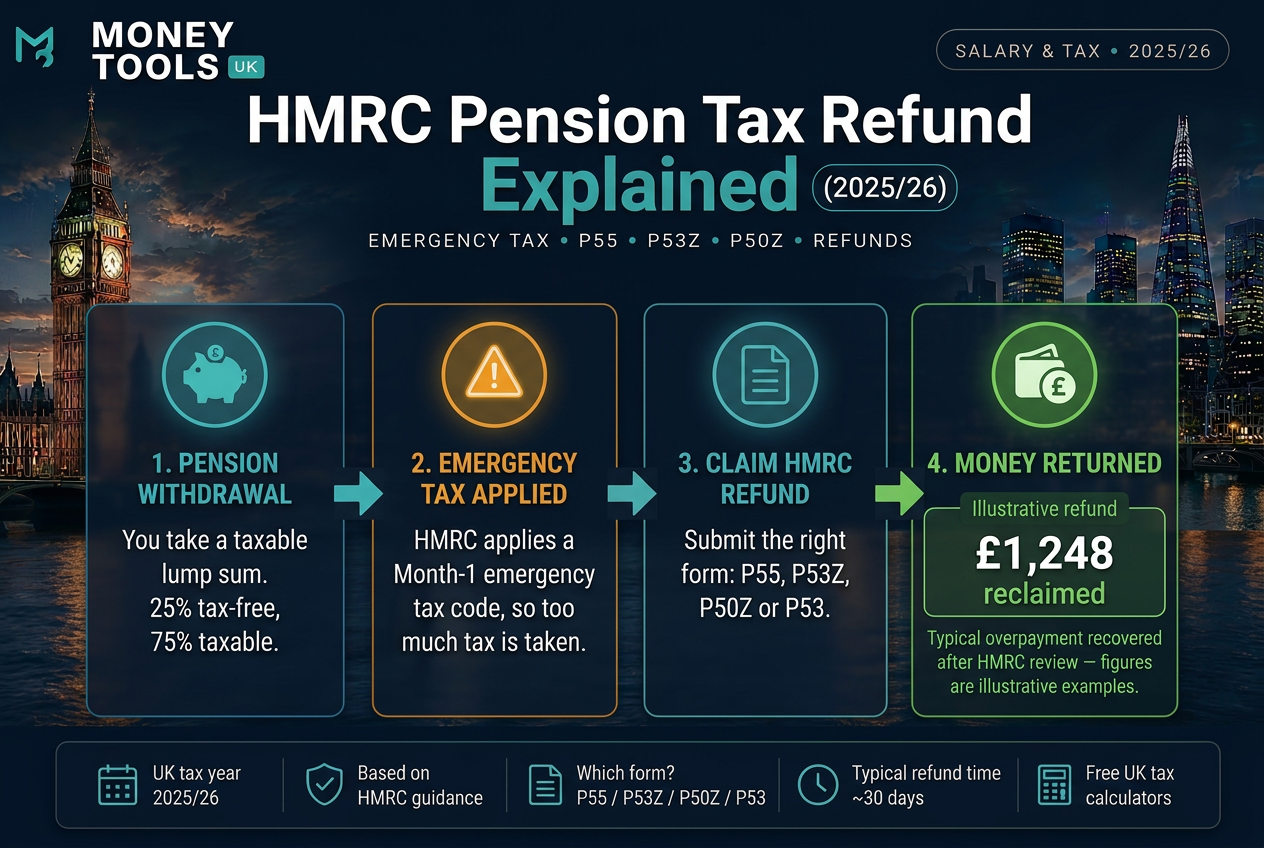

Why HMRC overtaxes pension withdrawals with emergency tax, how pension tax refunds work, and which form to use — P55, P53Z, P50Z or P53 — to reclaim overpaid tax for 2025/26.

Read guide

Learn how Plan 2 student loan repayments work in the UK for the 2025/26 tax year. Discover repayment thresholds, interest rates, salary examples and whether overpaying makes sense.

Read guideDisclaimer: This content is for informational purposes only and should not be treated as financial, tax, mortgage, investment or legal advice.