You can save

Tax + NI

Higher-rate relief

Up to 60%+

Pension boost

Bigger pot

Salary sacrifice is one of the few legal ways many UK employees can reduce Income Tax and National Insurance while increasing pension contributions. This guide explains exactly how it works, who benefits most, and shows the real numbers at every salary level.

Most UK employees pay more tax than they need to — not because they're doing anything wrong, but because they've never been shown the legitimate levers HMRC actually allows. Salary sacrifice is the most powerful of those levers. It lets you give up part of your gross (pre-tax) salary in exchange for a non-cash benefit — almost always an employer pension contribution — and in doing so reduces the income that Income Tax and National Insurance are calculated on.

Employers offer salary sacrifice because it benefits them too: when your contractual salary falls, so does the employer's National Insurance bill (15% in 2025/26 on most earnings above the secondary threshold). Many good employers pass some or all of that saving straight into your pension, which makes salary sacrifice even more generous than standard pension tax relief. The result is a rare win-win: you keep more of your pay today and build a larger pension for tomorrow.

This is a long, detailed guide written to be the clearest free explanation of salary sacrifice available in the UK. Complete beginners will understand it; experienced professionals and higher-rate taxpayers will find genuine tax-planning ideas. Every figure reflects the 2025/26 tax year for England, Wales and Northern Ireland.

Who Benefits Most From Salary Sacrifice?

- Employees earning £50,270+ — every pound sacrificed avoids 40% Income Tax and 2% employee NI, plus your employer may add their 15% NI saving to your pension.

- Parents affected by the High Income Child Benefit Charge — reducing taxable income below £60,000 can wipe out the charge entirely, keeping thousands in household income.

- Employees earning £100,000–£125,140 — salary sacrifice softens the 60% effective tax trap caused by the personal allowance taper, often the highest marginal rate in the UK.

- Bonus and commission earners — sacrificing variable pay locks in tax and NI savings on lump sums that would otherwise be taxed at your highest marginal rate.

- Employees whose employer shares NI savings — when employers pass on part or all of their 15% NI reduction, the total pension contribution can exceed what tax relief alone provides.

If you fall into any of these groups, the calculator at the top of this page will show exactly how much you could save.

The short answer

- What is salary sacrifice?

- A formal agreement to give up part of your gross salary in return for a benefit — usually a larger employer pension contribution. Because the sacrifice happens before tax, your taxable pay falls.

- Does it save tax?

- Yes. You don't pay Income Tax on the sacrificed amount — saving 20%, 40% or 45% depending on your band, and up to an effective 60% near the £100,000 personal allowance taper.

- Does it save National Insurance?

- Yes — and this is the key advantage over ordinary pension tax relief. You avoid employee NI (8% or 2%) on the sacrificed amount, and your employer may add their 15% NI saving to your pension too.

- Is it worth it?

- For most basic and higher-rate taxpayers who can afford a slightly lower take-home, yes — it's one of the most tax-efficient ways to save. It's rarely worth it if it drops your pay near the National Minimum Wage or you urgently need the cash.

- Who benefits most?

- Higher-rate taxpayers (£50,270+), parents affected by the High Income Child Benefit Charge, and anyone earning between £100,000 and £125,140 fighting the 60% tax trap.

Calculate Your Salary Sacrifice Savings

Every salary, pension scheme and tax situation is different. Use our free UK Take-Home Pay Calculator to compare your take-home pay with and without salary sacrifice, including Income Tax, National Insurance, pension contributions and student loan deductions.

How salary sacrifice works

Normally, your employer pays you a salary, HMRC takes Income Tax and National Insurance, your own pension contribution comes out, and you keep what's left. With salary sacrifice, you agree to a lower contractual salary and your employer redirects the difference into your pension before tax and NI are applied. The diagram below shows the same £60,000 earner with and without a £3,000 sacrifice.

Without salary sacrifice

- £60,000 salary

- Income Tax (full)

- National Insurance (full)

- You pay pension from net pay

- Take-home pay

With salary sacrifice

- £57,000 salary

- Lower Income Tax

- Lower National Insurance

- Employer pays £3,000 into pension

- Higher pension value + similar take-home

The key insight

Real-world worked examples

Figures below use 2025/26 thresholds: a £12,570 personal allowance, the 40% higher rate starting at £50,270, employee NI at 8% up to £50,270 and 2% above, and the personal allowance taper between £100,000 and £125,140. Each example shows what the sacrifice costs your take-home versus what lands in your pension.

Example A — £40,000 salary, 5% sacrifice (£2,000)

A basic-rate taxpayer sacrifices £2,000 of salary into their pension.

- Income Tax saved: 20% × £2,000 = £400

- National Insurance saved: 8% × £2,000 = £160

- Into the pension: £2,000 (before any employer NI top-up)

- Real cost to take-home: £2,000 − £400 − £160 = £1,440

A £2,000 pension contribution costs this employee just £1,440 — an immediate 28% boost before any investment growth.

Example B — £60,000 salary, £6,000 sacrifice

A higher-rate taxpayer sacrifices £6,000, all of which sits above the £50,270 higher-rate threshold.

- Income Tax saved: 40% × £6,000 = £2,400

- National Insurance saved: 2% × £6,000 = £120

- Into the pension: £6,000

- Real cost to take-home: £6,000 − £2,400 − £120 = £3,480

£6,000 in the pension for £3,480 out of pocket — a 42% uplift, and the sacrifice also reduces the income exposed to the High Income Child Benefit Charge.

Example C — £80,000 salary, £10,000 sacrifice

- Income Tax saved: 40% × £10,000 = £4,000

- National Insurance saved: 2% × £10,000 = £200

- Into the pension: £10,000

- Real cost to take-home: £10,000 − £4,000 − £200 = £5,800

At £80,000 the NI saving is small (only 2% applies this high up), but the 40% Income Tax relief is substantial: a £10,000 pension contribution for £5,800 of net pay.

Example D — £110,000 salary, £10,000 sacrifice (avoiding the 60% trap)

This is where salary sacrifice becomes spectacular. An employee earning £110,000 sacrifices £10,000, dropping their adjusted net income to £100,000 — the exact point where the personal allowance stops tapering.

- Income Tax saved on the £10,000: 40% = £4,000

- Personal allowance restored: £5,000 (the taper removes £1 for every £2 over £100k), taxed at 40% = a further £2,000 saved

- National Insurance saved: 2% × £10,000 = £200

- Total tax & NI saved: £4,000 + £2,000 + £200 = £6,200

- Real cost to take-home: £10,000 − £6,200 = £3,800

Effective relief of around 62%

Worked example — employer shares 50% of their NI saving

- Employee's tax and NI savings on the £10,000 stay exactly the same

- Pension contribution rises from £10,000 to £10,750

- The extra £750 costs the employee nothing — it is pure employer NI sharing

- Effective boost: a £10,750 pension contribution for the same net cost to take-home pay

Not every employer shares their NI saving, but many do — and some pass on 100%. Ask your payroll or HR team whether your scheme includes employer NI recycling. If it does, salary sacrifice becomes even more powerful than standard pension tax relief.

Why higher-rate taxpayers love salary sacrifice

Once your income passes £50,270, every extra pound is taxed at 40% (plus 2% NI). Salary sacrifice flips that maths in your favour because the same 40% relief now works on the way out of taxation.

- 40% tax relief: Sacrifice £1,000 and you keep £400 you would otherwise have paid in Income Tax, plus £20 in NI — your pension gains £1,000 for a net cost of around £580.

- Adjusted net income: Many tax thresholds (the personal allowance taper, Child Benefit charge, tax-free childcare) are based on adjusted net income, which salary sacrifice reduces pound-for-pound. Lowering this single number can unlock several benefits at once.

- Personal allowance taper: Sacrificing income below £100,000 protects your full £12,570 allowance — see the dedicated section below.

- Child Benefit charge: Reducing adjusted net income can reduce or eliminate the High Income Child Benefit Charge entirely.

The £100k tax trap

Between £100,000 and £125,140 the UK tax system contains its most punishing quirk. For every £2 you earn over £100,000, you lose £1 of your £12,570 personal allowance. That lost allowance becomes taxed income, so each extra £1 earned is effectively taxed at 60% (40% on the pound itself plus 40% on the 50p of allowance withdrawn) — before NI.

The 60% zone — a visual map

- £50,270─────Higher-rate (40%) tax begins

- £100,000─────Personal allowance taper begins — 60% effective rate

- £110,000─────Sacrifice £10,000 here to escape the trap

- £125,140─────Personal allowance fully lost

Salary sacrifice is the cleanest escape. By sacrificing the income that falls inside the trap into your pension, you bring your adjusted net income back to £100,000, restore your personal allowance, and convert money that would have been taxed at 60% into pension savings. As Example D showed, this can mean a £10,000 pension contribution for under £3,800.

See the 60% trap in full detail

Our £100k salary guide breaks down the personal allowance taper, the 60% marginal rate and the exact pension contributions that escape it.

The High Income Child Benefit Charge

The High Income Child Benefit Charge (HICBC) claws back Child Benefit once the higher earner in a household has an adjusted net income above £60,000, with the benefit fully removed by £80,000. The charge is 1% of the Child Benefit received for every £200 of income over £60,000.

- Who it affects: Any household claiming Child Benefit where one partner earns above £60,000.

- How salary sacrifice helps: Because the charge is based on adjusted net income, sacrificing salary into a pension lowers the figure used to calculate it.

Worked example — £70,000 with two children

Does Salary Sacrifice Reduce Student Loan Repayments?

Student loan repayments are calculated on earnings above the relevant repayment threshold. Because salary sacrifice reduces your taxable earnings before the calculation is made, it can lower the amount you repay each month for Plan 1, Plan 2, Plan 4 and Postgraduate Loans.

The size of the saving depends on your salary level and loan type. Plan 2 and Plan 4 borrowers repay 9% of income above their threshold; Postgraduate borrowers repay 6%. Every pound you sacrifice is a pound that no longer counts as earnings for student loan purposes, so the reduction in repayments is immediate and automatic.

It is important to recognise that reducing repayments is not always the same as saving money. Interest may continue to accrue on your loan balance, and the eventual cost depends on whether you expect to clear the debt before it is written off. For many borrowers, especially those on Plan 2 with large balances, the primary benefit of salary sacrifice remains the pension boost and tax relief — the student loan reduction is a useful secondary effect.

Worked example — Plan 2 borrower earning £40,000

The decision should always be considered alongside pension benefits and long-term financial goals. If you are likely to repay your loan in full before write-off, the lower repayments today mean less interest accumulated tomorrow. If write-off is more likely, the reduced repayments simply improve your monthly cash flow without changing the total amount you eventually pay.

See the Combined Effect on Your Payslip

Use our Student Loan Calculator alongside the Take-Home Pay Calculator to see the combined effect of salary sacrifice on tax, National Insurance, pension contributions and student loan repayments.

Bonuses, commission and performance pay

Annual bonuses, commission and performance payments are taxed as normal earnings — and because they sit on top of your salary, they're often taxed entirely at your highest marginal rate. A bonus can also tip you over the £50,270, £60,000 or £100,000 thresholds, triggering higher-rate tax, the Child Benefit charge or the 60% trap.

Many employers allow bonus sacrifice — diverting all or part of a bonus into your pension before it's taxed. This is one of the most efficient moves available:

- A higher-rate taxpayer sacrificing a £10,000 bonus saves £4,000 Income Tax and £200 NI immediately.

- If the bonus would have pushed you into the 60% band, the relief can exceed 60%.

- Because bonuses are one-off, sacrificing them avoids the year-round cash-flow impact of regular salary sacrifice.

Company cars and other benefits

Pensions are the most common salary-sacrifice benefit, but they're not the only one. Sacrifice arrangements can also cover company cars, the Cycle to Work scheme, additional holiday and workplace nurseries.

- Electric vehicles: EV salary sacrifice is hugely popular because electric company cars carry a very low Benefit-in-Kind (BiK) rate (3% in 2025/26). You pay for the car from gross salary, saving Income Tax and NI, while the BiK tax stays tiny.

- Petrol and diesel cars: Far less attractive — high BiK rates often wipe out the sacrifice saving, so the maths rarely works.

- Private medical insurance & most benefits-in-kind: Since 2017 these are caught by "Optional Remuneration Arrangement" rules, so the tax advantage of sacrificing for them has largely been removed — you're taxed on the higher of the cash given up or the benefit value. Pensions, EVs, cycle-to-work and childcare are the exceptions that keep their full advantage.

Who Should Consider Salary Sacrifice?

Salary sacrifice is not a one-size-fits-all strategy. For some UK employees it can unlock thousands of pounds in extra pension wealth each year; for others, the trade-offs around cash flow or borrowing capacity make it less suitable. The sections below will help you decide where you sit.

Salary Sacrifice Is Often Most Valuable For

- Higher-rate taxpayers earning above £50,270

- Parents affected by the High Income Child Benefit Charge

- Employees approaching or exceeding £100,000 income

- Bonus and commission earners

- Employees whose employer shares National Insurance savings

When Salary Sacrifice May Not Be Appropriate

- People with short-term cash-flow needs

- Employees near National Minimum Wage

- People carrying expensive consumer debt

- Employees planning a mortgage application soon

- Anyone needing access to their money before retirement

Salary sacrifice is highly effective for many UK employees, but it should always be weighed alongside your personal circumstances and financial goals. If you are unsure, a financial adviser can help you model the long-term impact on your pension, tax and day-to-day cash flow before you commit.

Advantages at a glance

| Benefit | Who benefits | Potential saving |

|---|---|---|

| Lower Income Tax | All taxpayers | 20%–45% of sacrificed amount |

| Lower National Insurance | All employees | 8% (basic) or 2% (higher) |

| Larger pension pot | Everyone saving for retirement | Often a 28%–60%+ instant uplift |

| Reduced adjusted net income | £100k+ earners | Up to 60% effective relief |

| Child Benefit protection | Parents earning £60k–£80k | Recovers up to 100% of the charge |

| Employer NI top-up | Where employer shares the saving | Extra 15% added to pension |

Disadvantages and trade-offs

Salary sacrifice is powerful, but it isn't free of downsides. A balanced decision means understanding what a lower contractual salary can affect.

- Lower contractual salary: Your "official" salary falls, which can matter for any benefit calculated on gross pay.

- Mortgage applications: Some lenders assess affordability on your reduced salary, potentially lowering how much you can borrow — though many now add pension contributions back.

- Life cover & income protection: Employer "death in service" and protection benefits set as a multiple of salary may be based on the lower figure unless your scheme uses "reference salary".

- Redundancy pay: Statutory and contractual redundancy can be calculated on the reduced salary.

- Statutory benefits: Sacrificing too much can reduce statutory maternity/paternity pay and, in extreme cases, affect State Pension qualifying earnings — you cannot sacrifice below the National Minimum Wage.

Check before you commit

When salary sacrifice may not be worth it

- Near the National Minimum Wage: You legally cannot sacrifice below NMW, and even approaching it is unwise.

- Short-term cash needs: If you need every pound now — for a deposit, a wedding or a tight budget — locking money in a pension until age 55+ (rising to 57 from 2028) may not suit you.

- High-interest debt: If you're carrying expensive credit card or loan debt, clearing it usually beats the return from sacrificing into a pension.

- Very low earnings: Below the personal allowance you pay little or no Income Tax, so there's less to save.

Common mistakes to avoid

- Confusing it with pension tax relief: Salary sacrifice saves NI as well as tax; "relief at source" contributions only reclaim Income Tax. They are not the same.

- Ignoring employer matching: Always capture the maximum employer pension match first — it's free money — before sacrificing extra.

- Sacrificing too much: Don't push your pay near the NMW or starve your day-to-day budget. Mind the £60,000 annual allowance too.

- Not checking mortgage implications: If you're applying for a mortgage soon, confirm how your lender treats sacrificed salary before reducing your headline pay.

- Forgetting the annual allowance: Total pension input above £60,000 a year (tapered for very high earners) can trigger a tax charge.

Savings comparison: £40k to £100k

One of the easiest ways to understand salary sacrifice is to compare what leaves your bank account with what arrives in your pension.

| Salary | Salary Sacrifice | Tax Saved | NI Saved | Real Cost | Pension Added |

|---|---|---|---|---|---|

| £40,000 | £2,000 | £400 | £160 | £1,440 | £2,000 |

| £60,000 | £6,000 | £2,400 | £120 | £3,480 | £6,000 |

| £80,000 | £10,000 | £4,000 | £200 | £5,800 | £10,000 |

| £110,000 | £10,000 | £6,200 | £200 | £3,800 | £10,000 |

Figures are illustrative and based on standard 2025/26 UK tax thresholds for a single PAYE employee with no student loan. The £110,000 row includes the personal allowance restored as adjusted net income drops back to £100,000.

As income rises, salary sacrifice generally becomes more valuable because higher-rate taxpayers save more Income Tax and can potentially avoid additional tax traps.

The table below applies a £5,000 salary sacrifice at each level (the £105k row drops the earner to £100,000 to show the taper effect). It compares the Income Tax saved, NI saved and the real cost of putting £5,000 into your pension.

| Salary | Sacrifice | Income Tax saved | NI saved | Net cost of £5,000 pension | Effective relief |

|---|---|---|---|---|---|

| £40,000 | £5,000 | £1,000 | £400 | £3,600 | 28% |

| £60,000 | £5,000 | £2,000 | £100 | £2,900 | 42% |

| £80,000 | £5,000 | £2,000 | £100 | £2,900 | 42% |

| £105,000 → £100,000 | £5,000 | £3,000* | £100 | £1,900 | 62% |

*Includes the personal allowance restored as income drops back to £100,000. Figures exclude any employer NI saving passed into your pension, which would improve the relief further.

Calculate your exact salary sacrifice savings

Every salary, pension scheme and tax code is slightly different. Use our free UK calculators to model your own numbers before you decide how much to sacrifice.

Take-Home Pay Calculator

See your monthly take-home with and without salary sacrifice, including Income Tax, NI, pension and student loans.

Salary to Hourly Calculator

Understand what your reduced salary means per hour and per month when planning a sacrifice.

Related salary guides

Salary sacrifice works differently at every income level. These guides show exactly how it reshapes take-home pay across the higher-rate band and into the 60% trap.

- £60k Salary After Tax UK — your first year as a higher-rate taxpayer, where the Child Benefit charge begins.

- £70k Salary After Tax UK — deep in the 40% band with strong sacrifice opportunities.

- £80k Salary After Tax UK — the point Child Benefit is fully withdrawn and the £100k taper looms.

- £90k Salary After Tax UK — just £10,000 from the trap, where planning matters most.

- £100k Salary After Tax UK — the definitive guide to the 60% tax trap and how to escape it.

Sources & references

This guide reflects official UK government and HMRC guidance for the 2025/26 tax year.

- HMRC — Salary sacrifice and the effects on PAYE

- GOV.UK — Tax on your private pension and pension tax relief

- GOV.UK — National Insurance rates and how much you pay

- GOV.UK — High Income Child Benefit Charge

- GOV.UK — Income over £100,000 and the personal allowance taper

Last updated

This article was last reviewed on 1 June 2026 and reflects UK Income Tax, National Insurance, pension and Child Benefit rules for the 2025/26 tax year. We refresh this guide each time HMRC publishes a material change.

Reviewed by Money Tools UK Editorial Team

This guide was reviewed for accuracy against HMRC and GOV.UK guidance for the 2025/26 tax year. We regularly update our salary and tax content when thresholds, National Insurance rates or benefit rules change.

Last reviewed: 1 June 2026

Disclaimer

Money Tools UK provides educational content and calculators only. Figures are estimates based on standard 2025/26 UK tax rules for England, Wales and Northern Ireland and assume a single PAYE employment with a standard tax code. Salary sacrifice can affect mortgages, benefits and protection cover — individual circumstances vary. For regulated tax or financial advice, please speak to a qualified accountant or independent financial adviser.

Get new UK finance and property guides from Money Tools UK

Plain-English UK finance insights, tax updates and property investing guides.

Related calculators

UK Take-Home Pay Calculator

The exact calculator this article is built around — open it and run your own numbers.

Open calculatorFrequently asked questions

Related guides

More flagship guides and tools from Money Tools UK.

A plain-English UK guide to checking if HMRC owes you a tax refund: why overpayments happen, how to use your Personal Tax Account, P800 and Simple Assessment, when refunds are automatic, how to claim, and how to avoid tax refund scams.

Read guide

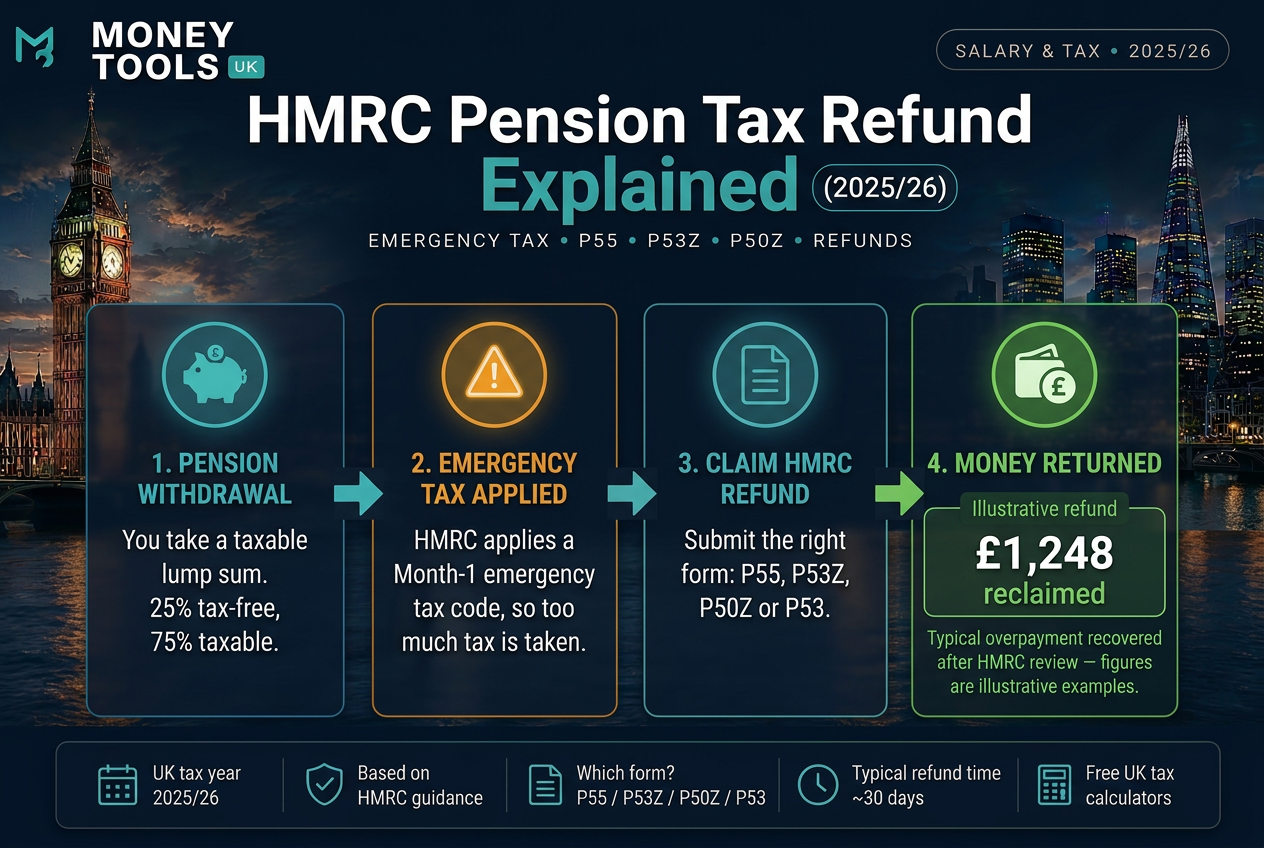

Why HMRC overtaxes pension withdrawals with emergency tax, how pension tax refunds work, and which form to use — P55, P53Z, P50Z or P53 — to reclaim overpaid tax for 2025/26.

Read guide

Learn how UK company car tax works in 2025/26, including Benefit-in-Kind tax, P11D value, CO2 emissions, electric cars, fuel benefit and salary sacrifice examples.

Read guideDisclaimer: This content is for informational purposes only and should not be treated as financial, tax, mortgage, investment or legal advice.