Annual take-home

£56,957

Monthly take-home

£4,746

You keep

~71p / £1

You keep approximately 71p of every £1 earned on an £80,000 salary. Because every pound above £50,270 is taxed at 40% plus 2% National Insurance, pension contributions and salary sacrifice are the most powerful tax-planning tools at this income level — and they become even more valuable as you approach the £100,000 personal allowance taper.

A £80,000 salary places you comfortably within the higher-rate tax band in the UK. While it offers a substantial income, a significant portion of your earnings is subject to 40% income tax, making it important to understand exactly how much you'll take home after deductions.

This guide breaks down how an £80,000 salary is taxed in the 2025/26 tax year, including income tax, National Insurance, pension contributions and student loan repayments.

Updated for 2025/26

The short answer

At a glance — £80,000 salary (2025/26)

Annual take-home

£56,957

Monthly take-home

£4,746

Weekly take-home

£1,095

Effective tax rate

~29%

Key takeaway: For most employees earning £80,000 in 2025/26, take-home pay will be approximately £56,957 per year before pension contributions and student loan deductions. Pension contributions can significantly improve tax efficiency at this income level.

Annual Take-Home

£56,957

Estimated annual net pay

Monthly Take-Home

£4,746

Approximate monthly pay

Weekly Take-Home

£1,095

Approximate weekly pay

Marginal Tax Rate

42%

40% tax + 2% NI above £50,270

Figures assume standard PAYE employment with no pension or student loan deductions.

How an £80,000 salary is taxed in 2025/26

For England, Wales and Northern Ireland in 2025/26 the income tax thresholds are frozen. The personal allowance is £12,570, the basic rate (20%) runs from £12,571 to £50,270, and the higher rate (40%) applies from £50,271 to £125,140. Because £80,000 exceeds the higher-rate threshold, a large part of your income is taxed at 40%.

National Insurance follows a similar split: you pay 8% between £12,570 and £50,270, then 2% on every pound above £50,270. The lower National Insurance rate above £50,270 helps reduce the impact of higher-rate tax on the upper slice of your salary.

Income tax on £80,000

Your taxable income is gross salary minus the personal allowance: £80,000 − £12,570 = £67,430. That amount is split across two rate bands:

- Basic rate (20%): £37,700 × 20% = £7,540

- Higher rate (40%): £29,730 × 40% = £11,892

- Total income tax: £19,432 a year (~£1,619 a month)

National Insurance on £80,000

- Main rate (8%): £50,270 − £12,570 = £37,700 → ×8% = £3,016

- Upper rate (2%): £80,000 − £50,270 = £29,730 → ×2% = £595

- Total NI: about £3,611 a year (~£301 a month)

Monthly and weekly take-home pay

With no pension contributions and no student loan, an £80,000 salary in 2025/26 lands in your bank account as follows:

- Gross salary: £80,000

- Income tax: −£19,432

- National Insurance: −£3,611

- Annual take-home: about £56,957

- Monthly take-home: about £4,746

- Weekly take-home: about £1,095

That's an effective tax-and-NI rate of around 29%.

Where your £80,000 salary goes

For every £1 you earn, roughly 71p ends up in your bank account. The remaining 29p goes to HMRC through income tax and National Insurance. Here is the complete breakdown for an £80,000 salary in 2025/26:

Gross salary

£80,000

100%

Income tax

£19,432

24.3%

National Insurance

£3,611

4.5%

Annual take-home pay

£56,957

71.2%

of gross salary

This means for every £1 you earn, approximately 71p is yours to keep after income tax and National Insurance. The other 29p funds public services through HMRC. Student loan repayments, pension contributions or salary sacrifice would further adjust these figures — use our calculator to model your exact situation.

Why £80k is a significant salary level

At £80,000:

- A large portion of your earnings is taxed at 40%.

- Pension contributions become increasingly valuable.

- Bonuses may face a marginal tax rate of 42% (40% tax plus 2% NI).

- You are only £20,000 away from the £100,000 personal allowance taper.

As income rises further, many higher earners begin planning around the £100k tax trap, where the personal allowance starts to taper away and effective marginal tax rates can rise significantly.

Many professionals earning around £80k begin using salary sacrifice and pension planning to improve tax efficiency.

Career progression beyond £80,000

In the UK, salaries around £80,000 are common in senior roles across several sectors. Typical examples include experienced software engineers, management consultants, senior NHS staff, legal associates, and qualified accountants or surveyors. At this level, professionals often move from purely focusing on earning more to thinking about how to keep more of what they earn.

Tax planning becomes increasingly relevant because a large share of additional income is taxed at 40%, with National Insurance adding another 2% in the higher-rate band. Pension contributions therefore offer strong value: every £1 contributed into a salary sacrifice arrangement saves 42p in combined tax and NI. For someone considering a move from £80k towards £100k, the marginal tax cost of extra earnings rises even further once the personal allowance taper begins at £100,000, creating an effective 60% rate up to £125,140.

Understanding these thresholds early allows professionals to structure pay rises, bonuses and pension contributions in a tax-efficient way before crossing into the taper zone. If you are moving up from a lower salary, it can help to compare the take-home pay on a £70,000 salary to see how much of each pay rise you actually keep.

£80k take-home with pension contributions

On £80,000 every pound above £50,270 is taxed at 40% income tax plus 2% National Insurance, so a pension contribution is one of the few levers that meaningfully reduces your tax bill. The figures below are all calculated on an £80,000 salary for the 2025/26 tax year, with no student loan, and reconcile with the £56,957 baseline take-home used throughout this guide.

Relief-at-source pension (5%)

Most workplace pensions use relief at source. A 5% contribution is £4,000 of gross pension, but you only pay 80% (£3,200) from your take-home — the pension provider adds 20% basic-rate relief automatically. As a higher-rate taxpayer you can reclaim a further 20% (£800) through your tax return or tax code.

- Gross pension contribution: £4,000

- Paid from your net pay: £3,200

- Basic-rate relief added by provider: £800

- Higher-rate relief you reclaim: £800

- Effective cost to you: £2,400 for £4,000 in your pension

Your monthly take-home falls by roughly £267 (the £3,200 net contribution spread over the year), leaving around £53,757 a year (~£4,480 a month) in cash, with the £800 higher-rate relief recovered separately.

Salary sacrifice pension (5%)

With salary sacrifice you give up £4,000 of gross salary in exchange for an employer pension contribution, so the money never appears on your payslip. Your taxable salary falls to £76,000 and the £4,000 escapes both 40% income tax and 2% higher-rate National Insurance.

- Salary sacrificed: £4,000 (paid straight into your pension)

- Income tax saved: £1,600

- National Insurance saved: £80

- Combined tax & NI saved: £1,680

Annual take-home lands at about £54,637 (~£4,553 a month) — higher than relief at source for the same £4,000 contribution, because salary sacrifice also saves the 2% National Insurance that relief at source does not.

Pension contribution comparison at £80k

The table below uses salary sacrifice on an £80,000 salary (2025/26, no student loan). The estimated tax saved is the combined income tax and National Insurance reduction versus making no contribution.

| Scenario | Pension contribution | Annual take-home | Monthly take-home | Est. tax & NI saved |

|---|---|---|---|---|

| No pension | £0 | £56,957 | £4,746 | — |

| 5% salary sacrifice | £4,000 | £54,637 | £4,553 | £1,680 |

| 10% salary sacrifice | £8,000 | £52,317 | £4,360 | £3,360 |

| 15% salary sacrifice | £12,000 | £49,997 | £4,166 | £5,040 |

Every £1,000 sacrificed reduces annual take-home by about £580, because £420 of each £1,000 is tax and NI you would otherwise have paid — money that goes into your pension instead of to HMRC.

Why pension contributions become increasingly valuable at £80k

Higher-rate tax relief. At £80,000 your top slice of income is taxed at 40%. Every £1,000 of pension contribution attracts £400 of relief, so the real cost of building retirement savings is far lower than at basic-rate income levels.

National Insurance savings through salary sacrifice. Above £50,270 employee NI is 2%. Salary sacrifice removes the contribution before NI is calculated, adding a further saving that relief-at-source pensions do not capture — and many employers also pass on part of their own NI saving.

Long-term retirement benefits. Contributions grow free of UK income and capital gains tax inside the pension wrapper, and 25% can usually be taken tax-free later, so the benefit compounds well beyond the upfront relief.

A practical tax-planning tool. Because £80,000 sits just £20,000 below the £100,000 personal allowance taper, professionals routinely use pension contributions to keep adjusted net income down and avoid the effective 60% marginal rate that bites between £100,000 and £125,140.

Figures are illustrative estimates for the 2025/26 tax year (England, Wales and Northern Ireland) and assume no student loan unless stated. Individual circumstances, employer pension schemes and the annual allowance vary — this is general information, not financial advice.

£80k take-home with a student loan

Student loans can have a noticeable impact on take-home pay.

Plan 2

- Threshold: £28,470

- Repayment rate: 9%

- Annual repayment: approximately £4,638

- Take-home pay: approximately £52,319

Plan 5

- Threshold: £25,000

- Repayment rate: 9%

- Annual repayment: approximately £4,950

- Take-home pay: approximately £52,000

Postgraduate Loan

- Threshold: £21,000

- Repayment rate: 6%

- Annual repayment: approximately £3,540

This applies in addition to undergraduate student loans.

Full payslip comparison at £80k

Here's how the different scenarios compare for an £80,000 gross salary in 2025/26 (illustrative figures):

| Scenario | Annual take-home | Monthly take-home |

|---|---|---|

| No pension, no student loan | ~£56,957 | ~£4,746 |

| 5% pension (relief at source) | ~£54,557 | ~£4,546 |

| 5% salary sacrifice | ~£54,637 | ~£4,553 |

| Plan 2 student loan | ~£52,319 | ~£4,360 |

| Postgraduate Loan only | ~£53,417 | ~£4,451 |

| Plan 2 + 5% salary sacrifice | ~£50,360 | ~£4,197 |

Postgraduate loans are deducted in addition to undergraduate student loans and can materially reduce take-home pay for higher earners. Even if you have already repaid your undergraduate loan, a postgraduate loan will continue to be deducted at 6% of income above the £21,000 threshold until it is fully repaid. To see how each plan affects your deductions, you can estimate your student loan repayments for the 2025/26 tax year.

Does Scotland change the picture?

Yes. Scotland operates its own income tax system and higher-rate thresholds. Someone earning £80,000 in Scotland will typically pay more income tax than a taxpayer earning the same salary in England, Wales or Northern Ireland. National Insurance and student loan rules remain the same throughout the UK.

Common mistakes people make at £80k

- Ignoring pension tax relief opportunities.

- Underestimating the impact of bonuses.

- Forgetting student loan deductions.

- Confusing gross income with take-home pay.

- Overlooking salary sacrifice schemes.

- Failing to plan ahead for the £100k tax threshold.

- Forgetting side-hustle tax. Selling on eBay, Vinted, Etsy or freelance platforms can trigger additional tax once you exceed the £1,000 trading allowance — and at £80k that extra income is usually taxed at your 40% higher-rate marginal rate (plus 9% student loan deductions if applicable), not 20%.

How to legitimately keep more of your £80k

- Increase pension contributions.

- Use salary sacrifice arrangements.

- Consider cycle-to-work schemes.

- Use electric vehicle salary sacrifice where available.

- Make Gift Aid donations.

- Optimise bonus timing where possible.

For many people earning £80,000, pension contributions provide the largest tax-saving opportunity.

For a personalised breakdown including pension contributions, salary sacrifice, bonuses, benefits-in-kind and student loans, you can calculate your exact take-home pay using our calculator.

Tax planning opportunities at £80,000

At £80,000 you are in the higher-rate tax band, so every pound you can remove from taxable income saves you 40% in income tax plus 2% in National Insurance. Here are the most practical strategies for this salary level.

Pension contributions

Contributing to a pension is the most straightforward way to reduce your tax bill. For a higher-rate taxpayer, every £1 contributed under relief-at-source costs you only 60p in net terms because HMRC refunds 40p via tax relief. With salary sacrifice the saving is even greater at 58p, because you also avoid the 2% National Insurance on the sacrificed amount.

Who it suits: Almost everyone at this income level, especially if you are not already contributing enough to receive full employer matching.

Impact: A £4,000 annual contribution (5% of £80k) typically reduces your taxable income by £4,000, saving approximately £1,680 in combined tax and NI.

Salary sacrifice

Salary sacrifice means agreeing to reduce your gross salary in exchange for a non-cash benefit — most commonly pension contributions, but also cycle-to-work schemes and electric vehicle leases. The sacrificed amount is never subject to income tax or National Insurance.

Who it suits: Employees whose employer offers a salary sacrifice scheme and who can afford a lower gross salary.

Impact: Sacrificing £4,000 of an £80,000 salary saves 42% (£1,680) compared with making the same contribution from net pay. It also reduces your student loan repayment if applicable.

Electric vehicle salary sacrifice

An increasingly popular benefit, EV salary sacrifice lets you lease an electric car through your employer. The monthly lease cost is deducted from gross pay before tax and NI, and as a zero-emission vehicle it attracts minimal benefit-in-kind tax (2% in 2025/26).

Who it suits: Drivers who would lease a car anyway and want to pay for it from pre-tax income.

Impact: On a typical £400/month lease, salary sacrifice saves around £168 per month in tax and NI compared with paying from take-home pay. The low benefit-in-kind rate means the tax charge on the car itself is negligible.

Gift Aid donations

When you make a charitable donation through Gift Aid, the charity can claim 25p from HMRC for every £1 you give. As a higher-rate taxpayer, you can claim back the additional 20% relief through your self-assessment tax return, meaning a £100 donation costs you only £60 after all reliefs.

Who it suits: Anyone who already supports charities or wants to reduce their tax bill while giving.

Impact: Donations do not reduce PAYE deductions during the year, but they reduce your final tax liability through self-assessment, generating a refund.

Bonus planning

Bonuses are taxed in the month they are paid, which can push you into a higher marginal rate temporarily. If you can influence timing, consider whether delaying a bonus into a tax year where you expect lower income (for example, if moving to part-time) could reduce the tax rate applied.

Who it suits: Employees with discretionary bonuses or those whose income fluctuates year to year.

Impact: A £10,000 bonus at £80,000 faces 42% marginal tax and NI (£4,200), leaving £5,800. If pushed into a basic-rate year, the same bonus would face only 33.25% (£3,325), saving nearly £900.

Individual circumstances vary

Approaching £100k?

Want your exact take-home pay?

Use the UK Take-Home Pay Calculator to include:

- pension contributions

- student loans

- bonuses

- salary sacrifice

- benefits-in-kind

- company car tax

- multiple income sources

Get a personalised payslip-style breakdown based on your exact circumstances.

Convert your salary into an hourly rate

See what your £80k salary works out at per hour, per week and per month after factoring in your working hours and weeks.

How we calculate these figures

Every figure in this guide is calculated for a single PAYE employment in England, Wales or Northern Ireland for the 2025/26 tax year, using HMRC's published thresholds. We apply a £12,570 personal allowance, 20% basic-rate tax to £50,270, 40% higher-rate tax to £125,140, and Class 1 employee National Insurance at 8% between £12,570 and £50,270 and 2% above. The personal allowance is tapered by £1 for every £2 of adjusted net income over £100,000. Pension and salary-sacrifice examples state which relief method they assume, and student loan figures use the relevant plan threshold. Results are rounded estimates and your payslip may differ depending on your tax code, benefits in kind and other circumstances.

Sources & references

This guide references current HMRC and GOV.UK guidance for the 2025/26 UK tax year.

- HMRC — Income Tax rates and bands

- HMRC — National Insurance contributions

- GOV.UK — Student loan repayment thresholds

- GOV.UK — Salary sacrifice guidance

- HMRC — Higher-rate tax guidance

Last updated

This article was last reviewed on 31 May 2026 and reflects UK tax thresholds, National Insurance rates and student loan repayment rules for the 2025/26 tax year. We refresh this guide each time HMRC publishes a material change.

Reviewed by Money Tools UK Editorial Team

This guide was reviewed for accuracy against HMRC and GOV.UK guidance for the 2025/26 tax year. We regularly update our salary and tax content when tax thresholds, National Insurance rates or student loan repayment rules change.

Last reviewed: 31 May 2026

Disclaimer

Money Tools UK provides educational content and calculators only. Figures are estimates based on standard 2025/26 UK tax rules for England, Wales and Northern Ireland (with Scottish rates noted where relevant) and assume a single PAYE employment with a standard tax code. Individual circumstances may vary. For regulated tax or financial advice, please speak to a qualified accountant or independent financial adviser.

Salary Milestone Comparison: How £80,000 Compares

As income rises, tax rates, National Insurance, pension planning and student loan repayments can have a significant impact on take-home pay. Comparing salary milestones helps you understand how much extra income you actually keep as your earnings increase.

| Salary | Annual Take-Home | Monthly Take-Home | Key Tax Milestone | Full Guide |

|---|---|---|---|---|

| £25,000 | £21,520 | £1,793 | Basic-rate band | Calculate £25k take-home pay |

| £30,000 | £25,120 | £2,093 | Basic-rate band | Calculate £30k take-home pay |

| £35,000 | £28,720 | £2,393 | Below higher-rate threshold | Calculate £35k take-home pay |

| £40,000 | £32,320 | £2,693 | Basic-rate taxpayer | View £40k Salary After Tax GuideSee exactly how a basic-rate salary is taxed and your monthly take-home. |

| £45,000 | £35,920 | £2,993 | Approaching higher rate | Calculate £45k take-home pay |

| £50,000 | £39,520 | £3,293 | Edge of the £50,270 threshold | View £50k Salary After Tax GuideLearn what happens as you reach the £50,270 higher-rate threshold. |

| £60,000 | £45,357 | £3,780 | Higher-rate taxpayer; HICBC begins | View £60k Salary After Tax GuideUnderstand higher-rate tax and how the Child Benefit charge starts to bite. |

| £70,000 | £51,157 | £4,263 | Deep in the higher-rate band | View £70k Salary After Tax GuideSee how take-home grows once you're firmly in the higher-rate band. |

| £80,000This guide | £56,957 | £4,746 | Higher-rate; nearing the £100k taper | You are here |

| £90,000 | £62,757 | £5,230 | Approaching the £100k taper | View £90k Salary After Tax GuideFind out how to plan pension contributions before the 60% trap hits. |

| £100,000 | £68,557 | £5,713 | Personal allowance taper / 60% trap | View £100k Salary After Tax GuideMaster the 60% tax trap and the personal allowance taper above £100k. |

| £120,000 | £78,157 | £6,513 | Inside the 60% trap; allowance nearly gone | Calculate £120k take-home pay |

Estimates assume a single PAYE employment for the 2025/26 tax year in England, Wales or Northern Ireland, with no pension contributions or student loan deductions. Your exact figures will vary.

Many readers compare multiple salary levels before negotiating a pay rise, changing jobs or making pension contribution decisions. Use the guides above to see how take-home pay changes across different income bands.

Get new UK finance and property guides from Money Tools UK

Plain-English UK finance insights, tax updates and property investing guides.

Related Salary Guides

Explore nearby salary levels to compare take-home pay, Income Tax, National Insurance, student loan deductions and pension contributions.

Related calculators

UK Take-Home Pay Calculator

The exact calculator this article is built around — open it and run your own numbers.

Open calculatorFrequently asked questions

Related guides

More flagship guides and tools from Money Tools UK.

A plain-English UK guide to checking if HMRC owes you a tax refund: why overpayments happen, how to use your Personal Tax Account, P800 and Simple Assessment, when refunds are automatic, how to claim, and how to avoid tax refund scams.

Read guide

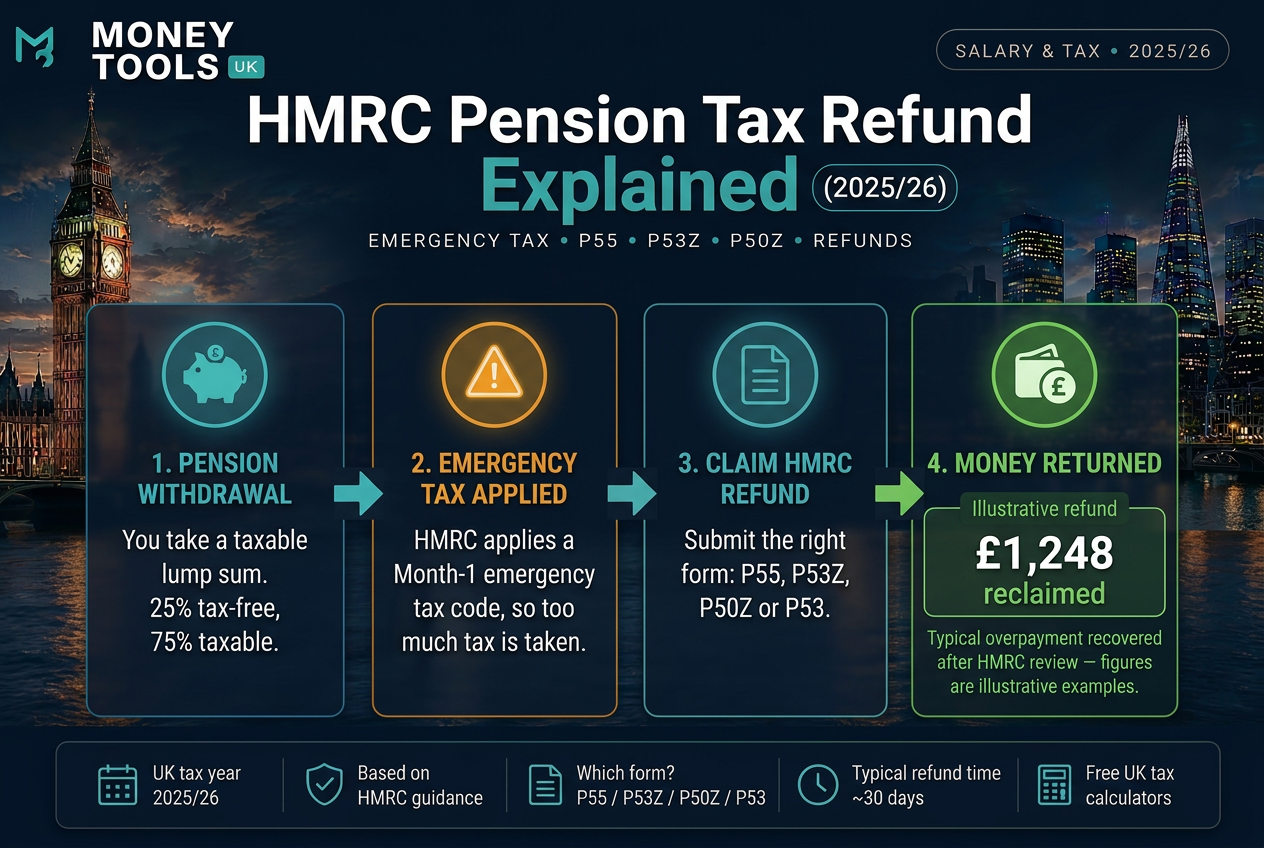

Why HMRC overtaxes pension withdrawals with emergency tax, how pension tax refunds work, and which form to use — P55, P53Z, P50Z or P53 — to reclaim overpaid tax for 2025/26.

Read guide

Learn how UK company car tax works in 2025/26, including Benefit-in-Kind tax, P11D value, CO2 emissions, electric cars, fuel benefit and salary sacrifice examples.

Read guideDisclaimer: This content is for informational purposes only and should not be treated as financial, tax, mortgage, investment or legal advice.