A £120,000 salary sits deep inside one of the most punishing zones in the entire UK tax system — the personal allowance taper. At this income level your tax-free personal allowance is almost entirely wiped out, every extra pound between £100,000 and £125,140 is taxed at an effective 60%, and yet salary sacrifice becomes far more powerful than at any salary below it. This guide explains exactly how much you take home from £120k in the 2025/26 tax year, how income tax and National Insurance are calculated, why the taper matters so much, and how pension contributions can restore your personal allowance and save you thousands.

Updated for 2025/26

The short answer

Quick facts: £120k after tax

Gross Salary

£120,000

Gross annual salary

Annual Take-Home

~£76,160

Estimated annual net pay

Monthly Take-Home

~£6,346

Approximate monthly pay

Weekly Take-Home

~£1,465

Approximate weekly pay

Marginal Tax Rate

62%

Marginal rate in the taper zone

Personal Allowance

Fully lost

Personal allowance removed

Tax Band

Higher rate

Top tax band reached

Tax Year

2025/26

Current UK tax year

Figures assume standard PAYE employment with no pension or student loan deductions. The personal allowance is reduced to almost nothing at £120,000 and disappears entirely at £125,140.

Why £120k is such an important salary

£120,000 is one of the most important salary levels in the UK because of where it sits relative to the £100,000 threshold. Once your income passes £100,000, the tax system changes shape dramatically:

- Your personal allowance is fully removed by the time you reach £125,140 — and at £120,000 only a sliver remains.

- Earnings between £100,000 and £125,140 face an effective 60% income tax rate because of the taper.

- National Insurance still applies on top of income tax.

- Many professionals use salary sacrifice to reduce their adjusted net income back below £100,000 and reclaim the full allowance.

If you are not yet familiar with how this zone begins, it is worth reading our guide to the £100k tax trap first — £120k is simply the point where that trap is biting hardest.

How a £120,000 salary is taxed in 2025/26

For England, Wales and Northern Ireland, income tax in 2025/26 is charged across these bands:

- Personal Allowance: £12,570 (taxed at 0%) — but reduced above £100,000

- Basic rate (20%): £12,571 to £50,270

- Higher rate (40%): £50,271 to £125,140

- Additional rate (45%): above £125,140

At £120,000 you have not quite reached the additional rate threshold (£125,140), so your top tax band is the higher rate. But because your income is above £100,000, the personal allowance taper removes £1 of allowance for every £2 earned over £100,000. At £120,000 that means £20,000 over the threshold → £10,000 of allowance lost → your personal allowance falls from £12,570 to just £2,570. National Insurance follows a separate structure: 8% between £12,570 and £50,270, then just 2% on everything above £50,270.

Income tax on £120,000

Your taxable income is gross salary minus the tapered personal allowance: £120,000 − £2,570 = £117,430. That amount is split across two rate bands:

- Basic rate (20%): £37,700 × 20% = £7,540

- Higher rate (40%): £79,730 × 40% = £31,892

- Total income tax: £39,432 a year (~£3,286 a month)

That is an effective income-tax rate of about 32.9% across the whole salary — but the marginal rate on the slice between £100,000 and £120,000 is the punishing 60% that makes this income band so notorious.

National Insurance on £120,000

- Main rate (8%): £50,270 − £12,570 = £37,700 → ×8% = £3,016

- Upper rate (2%): £120,000 − £50,270 = £69,730 → ×2% = £1,395

- Total NI: about £4,411 a year (~£368 a month)

Monthly and weekly take-home pay

With no pension contributions and no student loan, a £120,000 salary in 2025/26 lands in your bank account as follows:

- Gross salary: £120,000

- Income tax: −£39,432

- National Insurance: −£4,411

- Annual take-home: about £76,157

- Monthly take-home: about £6,346

- Weekly take-home: about £1,465

That is an effective tax-and-NI rate of around 36.5%. For most people at this level, pension contributions or salary sacrifice arrangements will substantially improve efficiency — because of what the personal allowance taper does between £100,000 and £125,140.

See your exact £120k take-home in seconds

Run your salary, pension, salary sacrifice, bonus and student loan through the UK Take-Home Pay Calculator for a full payslip-style breakdown.

Why the personal allowance taper matters

The personal allowance taper is the single most important thing to understand at £120k. The rule is simple but brutal:

The taper rule

Here is how the allowance and tax change as salary climbs through the taper zone:

| Salary | Personal allowance | Income tax | Annual take-home |

|---|---|---|---|

| £100,000 | £12,570 | £27,432 | £68,557 |

| £110,000 | £7,570 | £33,432 | £72,357 |

| £120,000 | £2,570 | £39,432 | £76,157 |

| £125,140 | £0 | £42,516 | £78,111 |

Worked example: £110k → £120k

What if your salary rises?

Estimated take-home

£45,357

Marginal tax rate

42%

Extra tax vs £50k

£4,162

Crossing £50,270 pushes additional earnings into the higher-rate tax band (40% income tax + 2% NI).

£120k take-home with pension contributions

Pension contributions are exceptionally powerful at £120k. They reduce your adjusted net income, which both lowers your tax bill and — once you bring adjusted net income back below £100,000 — restores your personal allowance pound for pound. Here is how common contribution levels affect your take-home:

| Scenario | Income tax | NI | Annual take-home |

|---|---|---|---|

| No pension | £39,432 | £4,411 | £76,157 |

| 5% pension (£6,000) | £35,832 | £4,291 | £73,877 |

| 10% pension (£12,000) | £32,232 | £4,171 | £71,597 |

| £20,000 salary sacrifice | £27,432 | £4,011 | £68,557 |

Note how the £20,000 salary sacrifice row produces the same figures as a £100,000 salary — because that is exactly what it achieves. The £20,000 goes into your pension, your take-home only falls by around £7,600 versus the no-pension scenario, and you reclaim your full personal allowance along the way. That is roughly 62% effective relief on the contribution.

The £120k pension lever

What happens if you increase your pension?

New annual take-home

£73,877

Tax & NI saved

£3,720

Into your pension

£6,000

Assumes relief-at-source contributions on a £120,000 salary, no student loan. Higher-rate relief shown as combined tax & NI saved versus 0% pension.

Salary sacrifice at £120k

Salary sacrifice is especially powerful at £120k for two reasons. First, it reduces your taxable salary, saving both income tax and National Insurance. Second — and uniquely valuable in this income band — it reduces your adjusted net income, which can restore your personal allowance and lift you out of the 60% trap entirely.

Many higher earners use salary sacrifice arrangements for pensions, electric vehicles and cycle-to-work precisely because of this allowance-restoring effect.

Worked example: £120k salary with £20k salary sacrifice

- £120,000 salary, sacrifice £20,000 into your pension

- Adjusted net income falls to £100,000

- Personal allowance is fully restored to £12,570

- Income tax falls from £39,432 to £27,432 — a £12,000 saving

- National Insurance also falls (lower taxable pay)

- £20,000 lands in your pension at a net cost of only ~£7,600

This is the single most efficient move available at £120k — roughly 62% effective relief on every pound sacrificed in the taper zone.

Full payslip comparison at £120k

Here is how the most common scenarios compare side by side for a £120,000 gross salary in 2025/26 (illustrative figures):

| Scenario | Annual take-home | Monthly take-home | Tax paid | NI paid |

|---|---|---|---|---|

| No pension | £76,157 | £6,346 | £39,432 | £4,411 |

| 5% pension | £73,877 | £6,156 | £35,832 | £4,291 |

| 10% pension | £71,597 | £5,966 | £32,232 | £4,171 |

| £20k salary sacrifice | £68,557 | £5,713 | £27,432 | £4,011 |

| £20k sacrifice + £10k bonus | ~£74,300 | ~£6,192 | ~£33,432 | ~£4,211 |

Salary sacrifice figures assume the sacrificed amount is paid into your pension; the bonus row assumes a £10,000 bonus paid on top of the sacrificed salary. Use the calculator to model your exact scheme.

Common mistakes people make at £120k

- Ignoring the personal allowance taper. Many people do not realise their tax-free allowance has almost vanished by £120k.

- Not understanding adjusted net income. Get this calculation wrong and you misjudge both the taper and any benefit charges.

- Taking bonuses inefficiently. A bonus paid in the taper zone is taxed at an effective 60–62% unless it is sacrificed into a pension.

- Missing pension opportunities. Pension relief at the 60% marginal rate is the most valuable lever available at this salary.

- Ignoring childcare and benefit implications. Adjusted net income above £100,000 also removes access to tax-free childcare and the 30 free hours scheme.

How to legitimately keep more of your £120k

- Pension contributions (relief at source or salary sacrifice).

- Salary sacrifice arrangements to reduce adjusted net income.

- Gift Aid donations (extend your basic-rate band).

- Charitable donations.

- Electric vehicle salary sacrifice.

- Cycle-to-work schemes.

For most people at this level, reducing adjusted net income below £100,000 produces the largest single tax saving by restoring the full personal allowance and escaping the 60% trap. Use the calculator to calculate your exact take-home pay and test different pension and sacrifice levels.

Want your exact £120k take-home pay?

Use the UK Take-Home Pay Calculator to include:

- pension contributions

- salary sacrifice

- student loans

- bonuses

- benefits-in-kind

- company car tax

- multiple income streams

Convert your £120k salary to an hourly rate

See what £120,000 a year works out at per hour, per day and per week with the Salary to Hourly Calculator.

Sources & references

This guide references current HMRC and GOV.UK guidance for the 2025/26 UK tax year.

- HMRC — Income Tax rates and Personal Allowances

- HMRC — National Insurance: how much you pay

- GOV.UK — Personal Allowance for income over £100,000

- GOV.UK — Salary sacrifice guidance

Last updated

This article was last reviewed on 7 June 2026 and reflects current UK income tax thresholds, National Insurance rates, personal allowance taper rules and salary sacrifice guidance for the 2025/26 tax year. We review and update this guide whenever HMRC or GOV.UK publishes a material change affecting salary calculations.

Disclaimer

Money Tools UK provides educational content and calculators only. The figures above are estimates based on standard 2025/26 UK tax rules for England, Wales and Northern Ireland (with Scottish rates noted where relevant) and assume a single PAYE employment with a standard tax code. Individual circumstances may vary. For regulated tax or financial advice, please speak to a qualified accountant or independent financial adviser.

Compare other salary levels

Understanding how tax changes at different salary levels helps put £120k earnings into context.

Get new UK finance and property guides from Money Tools UK

Plain-English UK finance insights, tax updates and property investing guides.

Related Salary Guides

Explore nearby salary levels to compare take-home pay, Income Tax, National Insurance, student loan deductions and pension contributions.

Related calculators

UK Take-Home Pay Calculator

The exact calculator this article is built around — open it and run your own numbers.

Open calculatorFrequently asked questions

Related guides

More flagship guides and tools from Money Tools UK.

A plain-English UK guide to checking if HMRC owes you a tax refund: why overpayments happen, how to use your Personal Tax Account, P800 and Simple Assessment, when refunds are automatic, how to claim, and how to avoid tax refund scams.

Read guide

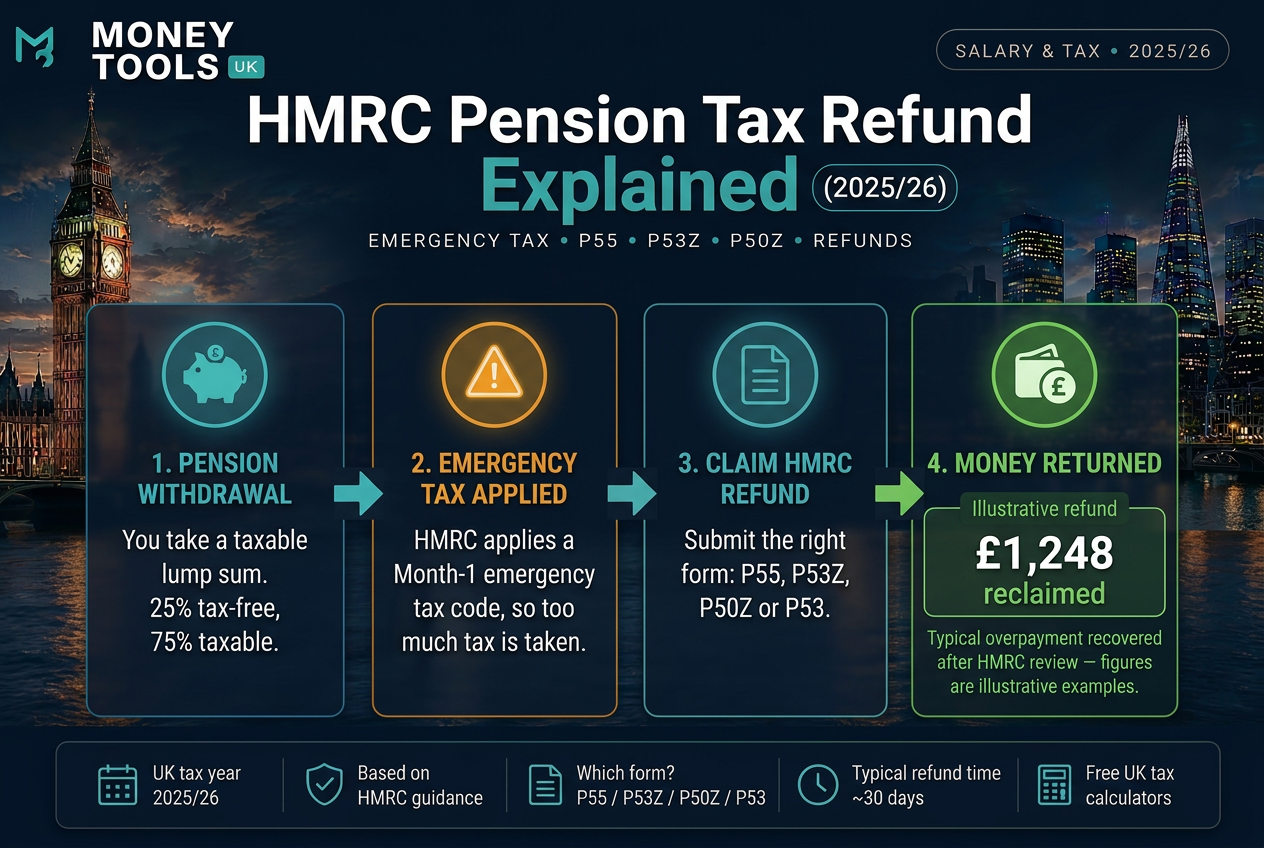

Why HMRC overtaxes pension withdrawals with emergency tax, how pension tax refunds work, and which form to use — P55, P53Z, P50Z or P53 — to reclaim overpaid tax for 2025/26.

Read guide

Learn how UK company car tax works in 2025/26, including Benefit-in-Kind tax, P11D value, CO2 emissions, electric cars, fuel benefit and salary sacrifice examples.

Read guideDisclaimer: This content is for informational purposes only and should not be treated as financial, tax, mortgage, investment or legal advice.