Annual take-home

£62,757

Monthly take-home

£5,230

You keep

~70p / £1

You keep approximately 70p of every £1 earned on a £90,000 salary. Because every pound above £50,270 is taxed at 40% plus 2% National Insurance, pension contributions and salary sacrifice are the most powerful tax-planning tools at this income level — and they become even more valuable as you approach the £100,000 personal allowance taper.

A £90,000 salary places you among the UK's highest earners. It sits well above the median full-time salary of around £37,000, puts you comfortably inside the top 5% of earners, and means a large slice of your pay is taxed at the 40% higher rate. Crucially, £90k still sits below the £100,000 point where your personal allowance begins to taper — so with smart planning you can avoid the effective 60% tax trap entirely.

At this level, tax planning becomes increasingly important. Pension contributions, salary sacrifice, bonuses, benefits-in-kind and the High Income Child Benefit Charge can each swing your real take-home pay by thousands of pounds a year. This guide breaks down exactly how a £90,000 salary is taxed in the 2025/26 tax year — and how to keep more of it.

Updated for 2025/26

The short answer

Why £90,000 Is a Key Salary Milestone in the UK

£90,000 is one of the most important salary levels in the UK tax system. It is the point where tax planning shifts from useful to essential, because the decisions you make here directly shape how much of your income you keep as you edge towards the £100,000 personal allowance taper. At this level a £90,000 salary sits firmly inside the 40% higher-rate band, so every pound above £50,270 is taxed at 40% plus 2% National Insurance — yet you still keep your full £12,570 personal allowance, because the taper only bites once adjusted net income exceeds £100,000.

Crucially, £90,000 sits roughly £10,000 below that £100,000 threshold. That small gap is what makes this milestone so strategic: you are close enough to the danger zone for planning to matter, but far enough below it to act before the effective 60% marginal rate between £100,000 and £125,140 takes hold. It is often the last straightforward opportunity to make pension and salary sacrifice decisions before that trap begins.

This is why pension contributions become so valuable at £90k. Higher-rate relief means every £1,000 paid in costs a higher-rate taxpayer only £600 in take-home pay, with the government adding the rest.Salary sacrifice goes further still, cutting both income tax and National Insurance while reducing the adjusted net income HMRC tests against the taper. Parents should also understand the High Income Child Benefit Charge, which can claw back Child Benefit unless contributions bring adjusted net income down. Many professionals earning £90k are approaching the point where poor planning becomes genuinely expensive — and where smart choices materially increase real take-home pay.

Key takeaway

At a glance — £90,000 salary (2025/26)

Annual take-home

£62,757

Monthly take-home

£5,230

Weekly take-home

£1,207

Effective tax rate

~30%

Key takeaway: For most employees earning £90,000 in 2025/26, take-home pay will be approximately £62,757 per year before pension contributions and student loan deductions. With £90k sitting just £10,000 below the £100,000 taper, pension contributions are the single most valuable tax-planning tool at this income level.

Annual Take-Home

£62,757

Estimated annual net pay

Monthly Take-Home

£5,230

Approximate monthly pay

Weekly Take-Home

£1,207

Approximate weekly pay

Marginal Tax Rate

42%

40% tax + 2% NI above £50,270

Figures assume standard PAYE employment with no pension or student loan deductions.

How a £90,000 salary is taxed in 2025/26

For England, Wales and Northern Ireland in 2025/26 the income tax thresholds are frozen. The personal allowance is £12,570, the basic rate (20%) runs from £12,571 to £50,270, and the higher rate (40%) applies from £50,271 to £125,140. Because £90,000 is well above the higher-rate threshold, a substantial part of your income is taxed at 40%.

Importantly, £90,000 is still below £100,000, so you keep your full personal allowance — the taper that creates the 60% effective rate only begins above £100,000. National Insurance follows a similar split: you pay 8% between £12,570 and £50,270, then just 2% on every pound above £50,270.

Income tax on £90,000

Your taxable income is gross salary minus the personal allowance: £90,000 − £12,570 = £77,430. That amount is split across two rate bands:

- Basic rate (20%): £37,700 × 20% = £7,540

- Higher rate (40%): £39,730 × 40% = £15,892

- Total income tax: £23,432 a year (~£1,953 a month)

National Insurance on £90,000

- Main rate (8%): £50,270 − £12,570 = £37,700 → ×8% = £3,016

- Upper rate (2%): £90,000 − £50,270 = £39,730 → ×2% = £795

- Total NI: about £3,811 a year (~£318 a month)

What most £90k earners actually take home

With no pension contributions and no student loan, a £90,000 salary in 2025/26 lands in your bank account as follows:

- Gross salary: £90,000

- Income tax: −£23,432

- National Insurance: −£3,811

- Annual take-home: about £62,757

- Monthly take-home: about £5,230

- Weekly take-home: about £1,207

That's an effective tax-and-NI rate of around 30% — higher than the ~29% paid on £80k, because the extra £10,000 of gross pay is taxed almost entirely at 40% income tax plus 2% NI.

See your exact £90k take-home in seconds

Run your salary, pension, student loan, bonus and salary sacrifice through the UK Take-Home Pay Calculator for a full payslip-style breakdown.

Monthly take-home pay breakdown

Pension contributions and student loans change the picture considerably at £90k. Here are five worked examples for the 2025/26 tax year:

- No pension, no student loan: ~£62,757/year (~£5,230/month).

- 5% pension (relief at source): £4,500 contribution → effective take-home ~£60,057/year (~£5,005/month) once higher-rate relief is claimed.

- 5% salary sacrifice pension: £4,500 sacrificed pre-tax and pre-NI → take-home ~£60,147/year (~£5,012/month), with £4,500 going straight into your pension.

- Plan 2 student loan: ~£5,537/year (~£461/month) → take-home ~£57,220/year (~£4,768/month).

- Postgraduate loan: ~£4,140/year (~£345/month) → take-home ~£58,617/year (~£4,885/month).

Higher-rate tax explained

The single most misunderstood number on a UK payslip is the marginal tax rate. Earning £90,000 does not mean all your income is taxed at 40% — only the slice above £50,270 is charged at the higher rate. The UK income tax structure works like a stack of layers:

- Personal allowance (0%): the first £12,570 is tax-free.

- Basic-rate band (20%): the next £37,700 (up to £50,270) is taxed at 20%.

- Higher-rate band (40%): everything from £50,270 to £90,000 — £39,730 — is taxed at 40%.

On £90k, the next £1 you earn is taxed at:

- 40% income tax

- 2% employee National Insurance

- 9% Plan 2 student loan (if applicable)

- = 42% — or 51% with Plan 2 marginal deductions

A common misunderstanding

How Take-Home Pay Changes Between £80k, £90k and £100k

| Salary | Annual Take-Home | Monthly Take-Home | Additional Net Income |

|---|---|---|---|

| £80,000 | £56,957 | £4,746 | — |

| £90,000 | £62,757 | £5,230 | +£5,800 |

| £100,000 | £68,557 | £5,713 | +£5,800 |

Although salary increases appear large on paper, much of each additional £10,000 falls into the higher-rate tax band. Moving from £80,000 to £90,000 increases gross pay by £10,000 but only adds around £5,800 to annual take-home pay. The same is broadly true when moving from £90,000 to £100,000.

This illustrates why pension contributions and salary sacrifice become increasingly valuable at higher income levels. Once earnings exceed £100,000, the withdrawal of the personal allowance creates an effective marginal tax rate of 60%, making tax planning even more important.

£100k Salary After Tax UK

What If Your Salary Increases to £95,000?

A £5,000 pay rise from £90,000 to £95,000 sounds substantial, but the tax system takes a meaningful slice. Most of that additional income falls into the 40% income tax band, and because you are already above the National Insurance upper earnings limit, the extra £5,000 also attracts 2% NI. Taken together, approximately £2,900 of the £5,000 increase is retainedafter Income Tax and National Insurance — around 58p of every extra pound earned.

The shift is not just about take-home pay. Adjusted net income moves closer to the £100,000 personal allowance taper, the point where the UK's most expensive tax band begins. At £95,000 you are only £5,000 below that threshold, so pension contributions become increasingly valuable as earnings rise toward six figures. A £5,000 pension contribution could bring adjusted net income back to £90,000, preserving the full personal allowance and securing higher-rate tax relief at an effective rate that only improves as you approach the trap.

Salary sacrifice is particularly powerful here, because it reduces both income tax and National Insurance while lowering the adjusted net income HMRC tests against the £100,000 limit. For many employees, this is the income level where tax planning shifts from occasional consideration to a regular part of financial decision-making.

Planning ahead

You’re Closer to the £100k Tax Trap Than You Think

A £90,000 salary may feel comfortably distant from the highest tax brackets, but in reality you are only £10,000 below the £100,000 threshold where the personal allowance begins to taper. Once adjusted net income crosses £100,000, every additional £1 earned begins reducing your £12,570 personal allowance at a rate of £1 for every £2 of income. The taper runs all the way to £125,140, where the personal allowance disappears completely.

Between £100,000 and £125,140 this creates an effective60% marginal tax rate:

- 40% income tax on the extra £1 earned

- 20% lost personal allowance (because £1 of the allowance is withdrawn for every £2 over £100,000)

- Together, that £1 costs 60p in tax — plus 2% National Insurance on top

Current Salary

£90,000

Distance to Taper

£10,000

The good news is that at £90,000 you still have room to manoeuvre.Pension contributions and salary sacrifice reduce your adjusted net income, which is the figure HMRC uses to test the £100,000 threshold. A £10,000 pension contribution, for example, could bring a £95,000 salary back below the taper point — preserving the full £12,570 personal allowance and avoiding the 60% effective rate entirely. Salary sacrifice is even more efficient, because it also reduces employer and employee National Insurance.

For anyone earning between £90,000 and £100,000, the combination of higher-rate tax relief and taper avoidance makes pension contributions one of the most valuable financial decisions you can make.

You’re Only £10,000 Away from the £100k Tax Trap

UK Tax Threshold Milestones

At £90,000 you are firmly inside the higher-rate tax band, but more importantly you sit just £10,000 below the £100,000 threshold where the personal allowance begins to taper. This is one of the most consequential distances in the UK tax system.

Once adjusted net income exceeds £100,000, every additional £2 earned removes £1 of the £12,570 personal allowance. The taper continues all the way to £125,140, where the allowance disappears entirely. Between those two figures, the combined effect of 40% income tax and the withdrawn allowance creates an effective marginal tax rate of 60%.

That means someone earning £105,000 could pay £3,000 in extra tax on the final £5,000 alone — an extraordinary burden that can be avoided with careful planning.

The most effective strategy is to reduce adjusted net income through pension contributions or salary sacrifice. Because these arrangements lower the income figure HMRC uses to test the £100,000 threshold, a £10,000 contribution can keep someone on £95,000 below the taper point entirely. Many high earners between £90,000 and £110,000 routinely use this approach to preserve their personal allowance, protect their Child Benefit and build retirement wealth at a fraction of the real cost.

Key takeaway

Pension optimisation at £90k

At £90,000, pension contributions are the most powerful tax-planning tool available to you — both because of generous higher-rate relief and because they keep your adjusted net income down as you approach the £100,000 taper and the High Income Child Benefit Charge thresholds.

Why pension contributions are so valuable at £90k

Higher-rate tax relief. At £90,000 your top slice of income is taxed at 40%. Every £1,000 of pension contribution attracts £400 of relief, so the real cost of building retirement savings is far lower than at basic-rate income levels.

National Insurance savings through salary sacrifice. Above £50,270 employee NI is 2%. Salary sacrifice removes the contribution before NI is calculated, adding a further saving that relief-at-source pensions don't capture — and many employers pass on part of their own NI saving too.

Reducing adjusted net income. Pension contributions lower your adjusted net income pound for pound. That protects your full personal allowance as you near £100,000 and can restore Child Benefit lost to the High Income Child Benefit Charge.

Preparing for the £100k threshold. Because £90,000 sits just £10,000 below the £100,000 taper, professionals routinely use pension contributions to stay below it and avoid the effective 60% marginal rate that bites between £100,000 and £125,140.

Worked pension example

What happens if you increase your pension?

New annual take-home

£60,147

Tax & NI saved

£1,890

Into your pension

£4,500

Assumes relief-at-source contributions on a £90,000 salary, no student loan. Higher-rate relief shown as combined tax & NI saved versus 0% pension.

Money Tools UK Insight

The High Income Child Benefit Charge at £90k

If you or your partner claim Child Benefit, £90k is an important number. For 2024/25 onwards, the High Income Child Benefit Charge (HICBC) starts at £60,000 of adjusted net income and fully claws back the benefit by £80,000. At £90,000 you are above the top of the taper, so — left unmanaged — the charge wipes out 100% of your Child Benefit.

- The charge removes 1% of Child Benefit for every £200 of adjusted net income above £60,000.

- By £80,000 of adjusted net income the full amount is reclaimed, so at £90,000 you lose all of it unless you reduce your adjusted net income.

- Pension contributions reduce adjusted net income. Sacrificing £10,000 brings your adjusted net income to £80,000, and a larger contribution down to £60,000 restores your Child Benefit in full.

Why £90k earners get caught out

Bonuses and company benefits

At £90k, bonuses and benefits-in-kind sit entirely in the higher-rate band, so they're taxed harder than your base salary feels like it should be — and a large bonus can even tip your adjusted net income over £100,000.

- Annual bonuses: a £10,000 bonus on £90k is taxed at 40% income tax + 2% NI, landing as about £5,800 net — or as little as ~£4,900 with a Plan 2 student loan. Paying the bonus into a pension via salary sacrifice avoids the deductions entirely and keeps you below £100,000.

- Company car tax: a petrol or diesel car with high CO₂ emissions can add £6,000+ of "benefit in kind" to your taxable income — taxed at 40%. Electric vehicles are taxed at far lower BIK rates (3% for 2025/26), making them dramatically more tax-efficient.

- Electric vehicle benefits: EV salary sacrifice lets you lease an electric car from gross pay before tax and NI, combining a tiny benefit-in-kind charge with 42% savings on the lease cost.

- Private medical insurance: employer-paid health cover is a taxable benefit. £1,000 of cover adds £1,000 to your taxable income, costing ~£400 in higher-rate tax.

- P11D implications: benefits-in-kind are reported on your P11D each year, often reducing your tax code and increasing PAYE deductions across the following year.

Student loan impact at £90k

Student loan repayments are calculated by HMRC as a percentage of income above a plan-specific threshold and deducted via PAYE. They don't reduce your tax, but they do shrink your payslip — and at £90k they're substantial. 2025/26 figures:

- Plan 1: threshold £26,065, 9%. Annual ≈ £5,754 (~£480/month) → take-home ~£57,003/year.

- Plan 2: threshold £28,470, 9%. Annual ≈ £5,537 (~£461/month) → take-home ~£57,220/year.

- Plan 4 (Scotland): threshold £32,745, 9%. Annual ≈ £5,152 (~£429/month) → take-home ~£57,605/year.

- Plan 5 (from Sept 2023): threshold £25,000, 9%. Annual ≈ £5,850 (~£488/month) → take-home ~£56,907/year.

- Postgraduate Loan: threshold £21,000, 6%. Annual ≈ £4,140 (~£345/month) → take-home ~£58,617/year.

If you hold both an undergraduate plan and a postgraduate loan, both are deducted simultaneously. On £90k that easily reaches £800+ a month of combined repayments, dramatically reducing take-home pay. To see how each plan affects your deductions, you can estimate your student loan repayments for the 2025/26 tax year.

Lifestyle and affordability on £90k

A £90,000 salary supports a comfortable, flexible lifestyle across most of the UK, but the gap between London and the regions remains stark.

- Mortgage affordability: at 4–4.5× income, a single £90k salary supports roughly £360,000–£405,000 of borrowing — comfortable for most regional markets, tighter in London and the South East.

- Savings potential: with disciplined budgeting, a £90k earner can realistically save 20–30% of net pay while maintaining a strong standard of living outside the capital.

- Investing and pension funding: higher earners benefit most from maximising pension input — both for the 40% relief and to manage adjusted net income for Child Benefit and the £100k taper.

- London vs regional UK: rent or mortgage costs in London can consume 35–45% of net pay, whereas the same salary in the North or Midlands leaves far more disposable income.

- Household budgeting: a couple where one partner earns £90k may be better off rebalancing pension and ISA contributions to stay below key thresholds.

You can also use our Mortgage Affordability Calculator to estimate how much you may be able to borrow on a £90,000 salary based on current lending multiples and affordability rules.

Common mistakes people make at £90k

- Misunderstanding higher-rate tax. Believing the whole salary is taxed at 40% — only the slice above £50,270 is.

- Ignoring salary sacrifice. Choosing relief at source over sacrifice leaves the 2% NI saving on the table and forces you to reclaim higher-rate relief via Self Assessment.

- Failing to plan for £100k. A bonus or pay rise that pushes adjusted net income over £100,000 triggers the 60% tax trap — easily avoided with a pension contribution.

- Overlooking the Child Benefit charge. At £90k the HICBC removes 100% of Child Benefit unless you reduce adjusted net income with pension contributions.

- Underestimating student loan deductions. A Plan 2 loan removes £460+/month, and multiple loans can exceed £800/month.

- Forgetting benefit-in-kind taxation. A high-CO₂ company car or private medical cover can quietly add thousands of taxable income, all charged at 40%.

Full payslip comparison at £90k

Here's how the most common scenarios compare side by side for a £90,000 gross salary in 2025/26 (illustrative figures):

| Scenario | Annual take-home | Monthly take-home |

|---|---|---|

| No pension, no student loan | ~£62,757 | ~£5,230 |

| 5% pension (relief at source) | ~£60,057 | ~£5,005 |

| 5% salary sacrifice | ~£60,147 | ~£5,012 |

| Plan 2 student loan | ~£57,220 | ~£4,768 |

| Plan 2 + 5% salary sacrifice | ~£55,015 | ~£4,585 |

Compare with £80k — and the £100k tax trap

Moving from £80,000 to £90,000 adds £10,000 of gross pay, but you keep less of it than you might expect. Because the whole extra slice sits in the 40% / 2% zone, the £10,000 rise lifts annual take-home from about £56,957 to £62,757 — a net gain of roughly £5,800, or about £484 a month. See the full breakdown in our £80k after tax guide.

Approaching the £100k tax trap

Calculate your exact £90k take-home pay

Use the UK Take-Home Pay Calculator to include:

- bonuses

- pension contributions

- salary sacrifice

- student loans

- company car tax

- benefits-in-kind

- side hustle income

Get a personalised payslip-style breakdown based on your exact circumstances.

Convert your salary into an hourly rate

See what your £90k salary works out at per hour, per week and per month after factoring in your working hours and weeks.

How we calculate these figures

Every figure in this guide is calculated for a single PAYE employment in England, Wales or Northern Ireland for the 2025/26 tax year, using HMRC's published thresholds. We apply a £12,570 personal allowance, 20% basic-rate tax to £50,270, 40% higher-rate tax to £125,140, and Class 1 employee National Insurance at 8% between £12,570 and £50,270 and 2% above. The personal allowance is tapered by £1 for every £2 of adjusted net income over £100,000. Pension and salary-sacrifice examples state which relief method they assume, and student loan figures use the relevant plan threshold. Results are rounded estimates and your payslip may differ depending on your tax code, benefits in kind and other circumstances.

Sources & references

This guide references current HMRC and GOV.UK guidance for the 2025/26 UK tax year.

- HMRC — Income Tax rates and bands

- HMRC — National Insurance rates and thresholds

- GOV.UK — Student loan repayment thresholds and rates

- GOV.UK — High Income Child Benefit Charge

- GOV.UK — Pension tax relief

- HMRC — PAYE thresholds and income over £100,000

Last updated

This article was last reviewed on 1 June 2026 and reflects UK tax thresholds, National Insurance rates and student loan repayment rules for the 2025/26 tax year. We refresh this guide each time HMRC publishes a material change.

Reviewed by Money Tools UK Editorial Team

This guide was reviewed for accuracy against HMRC and GOV.UK guidance for the 2025/26 tax year. We regularly update our salary and tax content when tax thresholds, National Insurance rates or student loan repayment rules change.

Last reviewed: 1 June 2026

Disclaimer

Money Tools UK provides educational content and calculators only. Figures are estimates based on standard 2025/26 UK tax rules for England, Wales and Northern Ireland (with Scottish rates noted where relevant) and assume a single PAYE employment with a standard tax code. Individual circumstances may vary. For regulated tax or financial advice, please speak to a qualified accountant or independent financial adviser.

Salary Milestone Comparison: How £90,000 Compares

As income rises, tax rates, National Insurance, pension planning and student loan repayments can have a significant impact on take-home pay. Comparing salary milestones helps you understand how much extra income you actually keep as your earnings increase.

| Salary | Annual Take-Home | Monthly Take-Home | Key Tax Milestone | Full Guide |

|---|---|---|---|---|

| £25,000 | £21,520 | £1,793 | Basic-rate band | Calculate £25k take-home pay |

| £30,000 | £25,120 | £2,093 | Basic-rate band | Calculate £30k take-home pay |

| £35,000 | £28,720 | £2,393 | Below higher-rate threshold | Calculate £35k take-home pay |

| £40,000 | £32,320 | £2,693 | Basic-rate taxpayer | View £40k Salary After Tax GuideSee exactly how a basic-rate salary is taxed and your monthly take-home. |

| £45,000 | £35,920 | £2,993 | Approaching higher rate | Calculate £45k take-home pay |

| £50,000 | £39,520 | £3,293 | Edge of the £50,270 threshold | View £50k Salary After Tax GuideLearn what happens as you reach the £50,270 higher-rate threshold. |

| £60,000 | £45,357 | £3,780 | Higher-rate taxpayer; HICBC begins | View £60k Salary After Tax GuideUnderstand higher-rate tax and how the Child Benefit charge starts to bite. |

| £70,000 | £51,157 | £4,263 | Deep in the higher-rate band | View £70k Salary After Tax GuideSee how take-home grows once you're firmly in the higher-rate band. |

| £80,000 | £56,957 | £4,746 | Higher-rate; nearing the £100k taper | View £80k Salary After Tax GuideDiscover your real take-home as you approach the £100k allowance taper. |

| £90,000This guide | £62,757 | £5,230 | Approaching the £100k taper | You are here |

| £100,000 | £68,557 | £5,713 | Personal allowance taper / 60% trap | View £100k Salary After Tax GuideMaster the 60% tax trap and the personal allowance taper above £100k. |

| £120,000 | £78,157 | £6,513 | Inside the 60% trap; allowance nearly gone | Calculate £120k take-home pay |

Estimates assume a single PAYE employment for the 2025/26 tax year in England, Wales or Northern Ireland, with no pension contributions or student loan deductions. Your exact figures will vary.

Many readers compare multiple salary levels before negotiating a pay rise, changing jobs or making pension contribution decisions. Use the guides above to see how take-home pay changes across different income bands.

Get new UK finance and property guides from Money Tools UK

Plain-English UK finance insights, tax updates and property investing guides.

Related Salary Guides

Explore nearby salary levels to compare take-home pay, Income Tax, National Insurance, student loan deductions and pension contributions.

Related calculators

UK Take-Home Pay Calculator

The exact calculator this article is built around — open it and run your own numbers.

Open calculatorFrequently asked questions

Related guides

More flagship guides and tools from Money Tools UK.

A plain-English UK guide to checking if HMRC owes you a tax refund: why overpayments happen, how to use your Personal Tax Account, P800 and Simple Assessment, when refunds are automatic, how to claim, and how to avoid tax refund scams.

Read guide

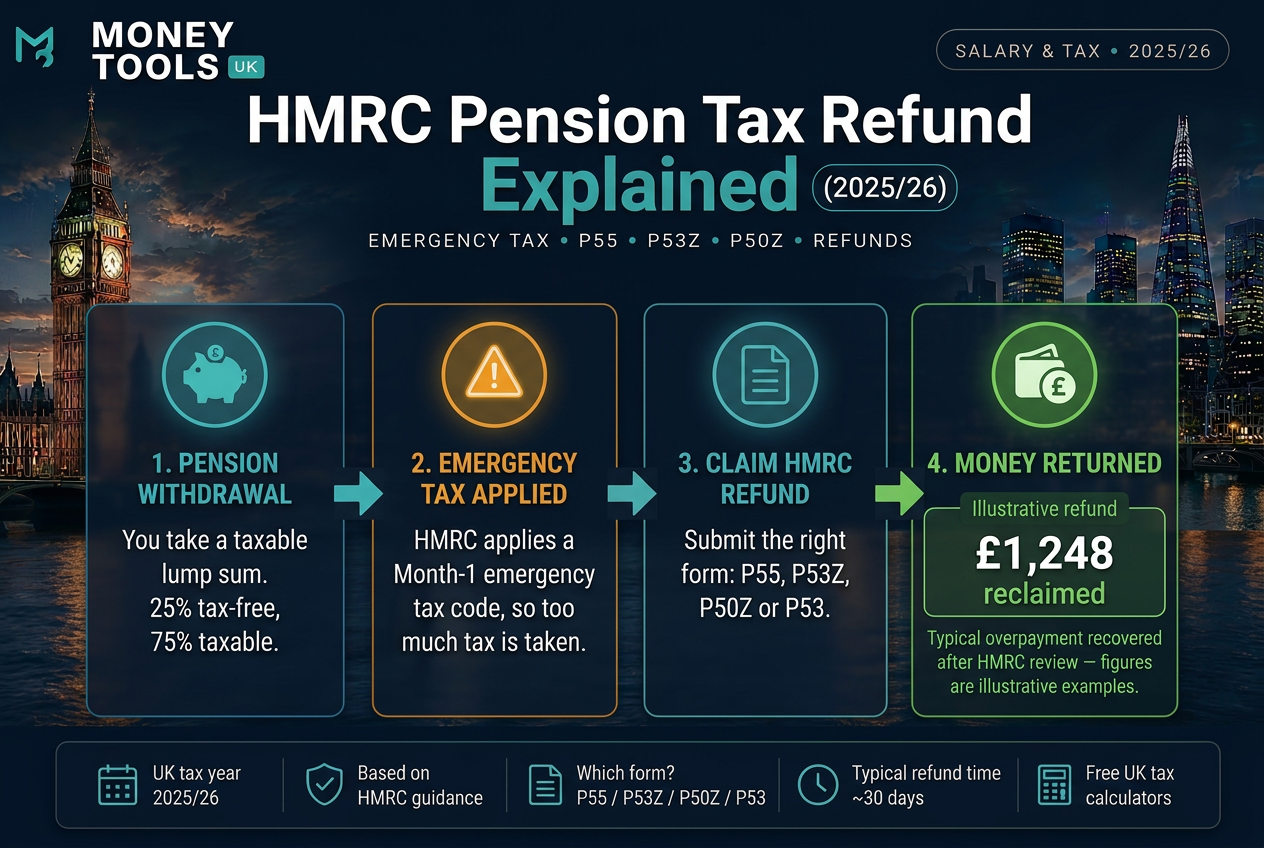

Why HMRC overtaxes pension withdrawals with emergency tax, how pension tax refunds work, and which form to use — P55, P53Z, P50Z or P53 — to reclaim overpaid tax for 2025/26.

Read guide

Learn how UK company car tax works in 2025/26, including Benefit-in-Kind tax, P11D value, CO2 emissions, electric cars, fuel benefit and salary sacrifice examples.

Read guideDisclaimer: This content is for informational purposes only and should not be treated as financial, tax, mortgage, investment or legal advice.