Student loan repayments are one of the most misunderstood deductions on a UK payslip. Many graduates believe they are paying off a traditional debt, while others assume student loan deductions are simply another tax. The reality sits somewhere in between.

Your repayment depends on:

- your student loan plan

- your earnings

- the repayment threshold

- how long you have been repaying

- whether your income increases over time

This guide explains exactly how Plan 2 student loans work in the 2025/26 tax year, how repayments are calculated, how much comes off your payslip and whether making extra repayments is worth considering.

The short answer

Plan 2 in one box

What is a Plan 2 student loan?

Plan 2 generally applies to students from England (and Wales) who started an undergraduate course between 1 September 2012 and 31 July 2023. It covers both tuition fee loans and maintenance loans taken out during that period.

The UK has several different repayment plans, each with its own threshold and rate. Knowing which one you are on matters, because it changes exactly how much comes off your pay:

| Plan | Who it typically covers | Threshold | Rate |

|---|---|---|---|

| Plan 1 | English/Welsh students who started before Sep 2012; many Northern Ireland borrowers | £26,065 | 9% |

| Plan 2 | England/Wales students who started Sep 2012 – Jul 2023 | £28,470 | 9% |

| Plan 4 | Scottish students | £32,745 | 9% |

| Plan 5 | English students who started from Aug 2023 onwards | £25,000 | 9% |

| Postgraduate Loan | Master's and doctoral loans | £21,000 | 6% |

If you have both an undergraduate Plan 2 loan and a Postgraduate Loan, the two are calculated separately and can be deducted at the same time — 9% on the Plan 2 element and 6% on the postgraduate element.

Who is on Plan 2?

You are most likely on Plan 2 if:

- you are an English or Welsh student, and

- you started an undergraduate course on or after 1 September 2012 and before 1 August 2023.

Students who started from August 2023 are usually on the newer Plan 5, and those who started before 2012 are typically on Plan 1. If you are unsure, the quickest way to confirm your plan is to sign in to your online repayment account.

How to check your plan

How repayments work

Plan 2 repayments are income-based, not a fixed monthly amount. You only repay a percentage of what you earn above the threshold, so your repayment moves with your pay:

- If your income rises — your repayments increase.

- If your income falls — your repayments decrease.

- If your earnings fall below the threshold — repayments stop entirely until you earn above it again.

Because deductions are based on each pay period, a large one-off bonus can trigger a bigger deduction that month, even if your annual salary is below the threshold. The amount is worked out by your employer through PAYE and passed to HMRC, who pass it to the Student Loans Company.

2025/26 repayment threshold

Plan 2 repayment threshold

Only income above the threshold is subject to the 9% repayment rate. Everything you earn up to £28,470 is ignored for student loan purposes — so a graduate earning exactly £28,470 repays nothing at all.

Student loan deduction formula

The Plan 2 calculation is straightforward:

Student Loan Repayment = (Earnings − £28,470) × 9%

Worked example — £35,000 salary

In practice, HMRC rounds each repayment down to the nearest whole pound in every pay period, so the exact figure on your payslip may be a few pence lower.

Salary examples

Here is how Plan 2 repayments scale across common salaries for 2025/26. Notice that repayments only ever apply to the slice of income above £28,470.

| Salary | Income above threshold | Annual repayment | Monthly repayment |

|---|---|---|---|

| £30,000 | £1,530 | £137.70 | ~£11 |

| £35,000 | £6,530 | £587.70 | ~£49 |

| £50,000 | £21,530 | £1,937.70 | ~£161 |

| £70,000 | £41,530 | £3,737.70 | ~£311 |

| £100,000 | £71,530 | £6,437.70 | ~£536 |

Why student loans feel like a tax

For many graduates, a Plan 2 loan behaves far more like an extra tax than a conventional debt — and there are good reasons for that:

- Many graduates never repay the full balance. Repayments are capped at 9% of income above the threshold, and the balance is written off after 30 years.

- Repayments are linked to income, not the size of the debt — exactly like Income Tax or National Insurance.

- Repayments stop automatically if your earnings fall below the threshold.

- The balance can be written off entirely, meaning some borrowers repay only a fraction of what they originally borrowed.

Unlike a commercial loan, missing the "full repayment" is not a default and does not damage your credit. That is why economists often describe Plan 2 repayments as a graduate contribution rather than a traditional debt.

Interest rates explained

Plan 2 interest is linked to the Retail Price Index (RPI)and varies with your income:

- While studying and until the April after you leave — RPI plus up to 3%.

- Earning under £28,470 — RPI only.

- Earning between £28,470 and £51,245 — RPI rising on a sliding scale.

- Earning above £51,245 — RPI plus 3% (the maximum).

Why some balances grow despite repayments

Example: a graduate with a £45,000 balance earning £32,000 repays around £318 a year. If interest is higher than £318 that year, the balance grows slightly — but the repayment, not the balance, is what affects their take-home pay.

When repayments stop

Plan 2 repayments stop in one of three situations:

- The loan is fully repaid — once the balance reaches zero, deductions stop.

- The write-off period is reached — Plan 2 loans are written off 30 years after the April you first became due to repay (usually the April after graduation).

- Death of the borrower — the loan is cancelled and is never recovered from your estate.

The 30-year write-off is a defining feature of Plan 2. It means a large proportion of borrowers will have their remaining balance cancelled before they ever clear it.

Common myths

Myth: student loans affect your credit score

Myth: you must repay regardless of earnings

Myth: repayments continue abroad automatically

Myth: paying extra always makes sense

Myth: a student loan is identical to commercial debt

Should you make voluntary repayments?

Whether overpaying makes sense depends almost entirely on your earnings trajectory. There is no single right answer.

Potential pros

- Clears the loan faster if you will repay it in full

- Reduces total interest paid for high earners

- Removes the monthly deduction once cleared

- Psychological relief of being debt-free

Potential cons

- Wasted money if the loan would be written off anyway

- The cash may be better in a pension, ISA or emergency fund

- No early-repayment penalty either way, but no refund once paid

- Repayments already stop if your income drops

Who may benefit: high earners on track to clear the entire balance well within 30 years, where overpaying genuinely saves interest.

Who probably should not: average and lower earners whose balance is likely to be written off — for them, the 9% deduction behaves like a time-limited tax, and spare cash usually works harder in a pension or savings.

Worked examples

These examples show the full payslip picture — Income Tax, National Insurance and the Plan 2 deduction — and the impact on take-home pay for 2025/26. Figures assume a standard tax code and no pension contributions.

Example A — £30,000 salary

- Income Tax: £3,486

- National Insurance: £1,394

- Plan 2 student loan: £137

- Take-home pay: ≈ £24,983 (about £2,082 a month)

Example B — £50,000 salary

- Income Tax: £7,486

- National Insurance: £2,994

- Plan 2 student loan: £1,937

- Take-home pay: ≈ £37,583 (about £3,132 a month)

Example C — £70,000 salary

- Income Tax: £15,432

- National Insurance: £3,410

- Plan 2 student loan: £3,737

- Take-home pay: ≈ £47,421 (about £3,952 a month)

Example D — £100,000 salary

- Income Tax: £27,432

- National Insurance: £4,010

- Plan 2 student loan: £6,437

- Take-home pay: ≈ £62,121 (about £5,177 a month)

The Plan 2 deduction is meaningful but rarely the largest line on your payslip — Income Tax and National Insurance take far more. Salary sacrifice into a pension can reduce the earnings used to calculate your student loan, lowering the deduction at the same time.

Calculate Your Exact Take-Home Pay

Use the Money Tools UK Take-Home Pay Calculator to estimate Income Tax, National Insurance, pension deductions and Plan 2 student loan repayments — and see exactly what lands in your bank account.

Related guides

- Adjusted Net Income Explained — the figure behind many UK tax thresholds.

- Child Benefit Tax Charge Explained — how income drives the £60k–£80k charge.

- Salary Sacrifice Explained — how it can reduce your student loan deduction.

- How Bonuses Are Taxed in the UK — why a bonus can spike your repayment.

- £50k Salary After Tax UK — full payslip breakdown at £50,000.

- £70k Salary After Tax UK — full payslip breakdown at £70,000.

- £100k Salary After Tax UK — full payslip breakdown at £100,000.

Sources & references

This guide references current GOV.UK and Student Loans Company guidance for the 2025/26 UK tax year.

- GOV.UK — Student finance

- GOV.UK — Repaying your student loan

- GOV.UK — What you pay (repayment thresholds and rates)

- Student Loans Company — official guidance

- GOV.UK — PAYE: student loan deductions for employers

Last updated

This article was last reviewed on 15 June 2026 and reflects Plan 2 student loan rules, repayment thresholds and PAYE deductions applicable during the 2025/26 UK tax year. We refresh this guide each time the thresholds or rules change.

Disclaimer

Money Tools UK provides educational content and calculators only. The figures above are estimates based on standard 2025/26 UK tax and student loan rules and assume straightforward circumstances. They do not account for multiple loan plans, Scottish Income Tax bands, benefits in kind, or personal circumstances that may change your actual deductions. For regulated tax or financial advice, please speak to a qualified accountant or independent financial adviser.

Get new UK finance and property guides from Money Tools UK

Plain-English UK finance insights, tax updates and property investing guides.

Related calculators

UK Take-Home Pay Calculator

The exact calculator this article is built around — open it and run your own numbers.

Open calculatorFrequently asked questions

Related guides

More flagship guides and tools from Money Tools UK.

A plain-English UK guide to checking if HMRC owes you a tax refund: why overpayments happen, how to use your Personal Tax Account, P800 and Simple Assessment, when refunds are automatic, how to claim, and how to avoid tax refund scams.

Read guide

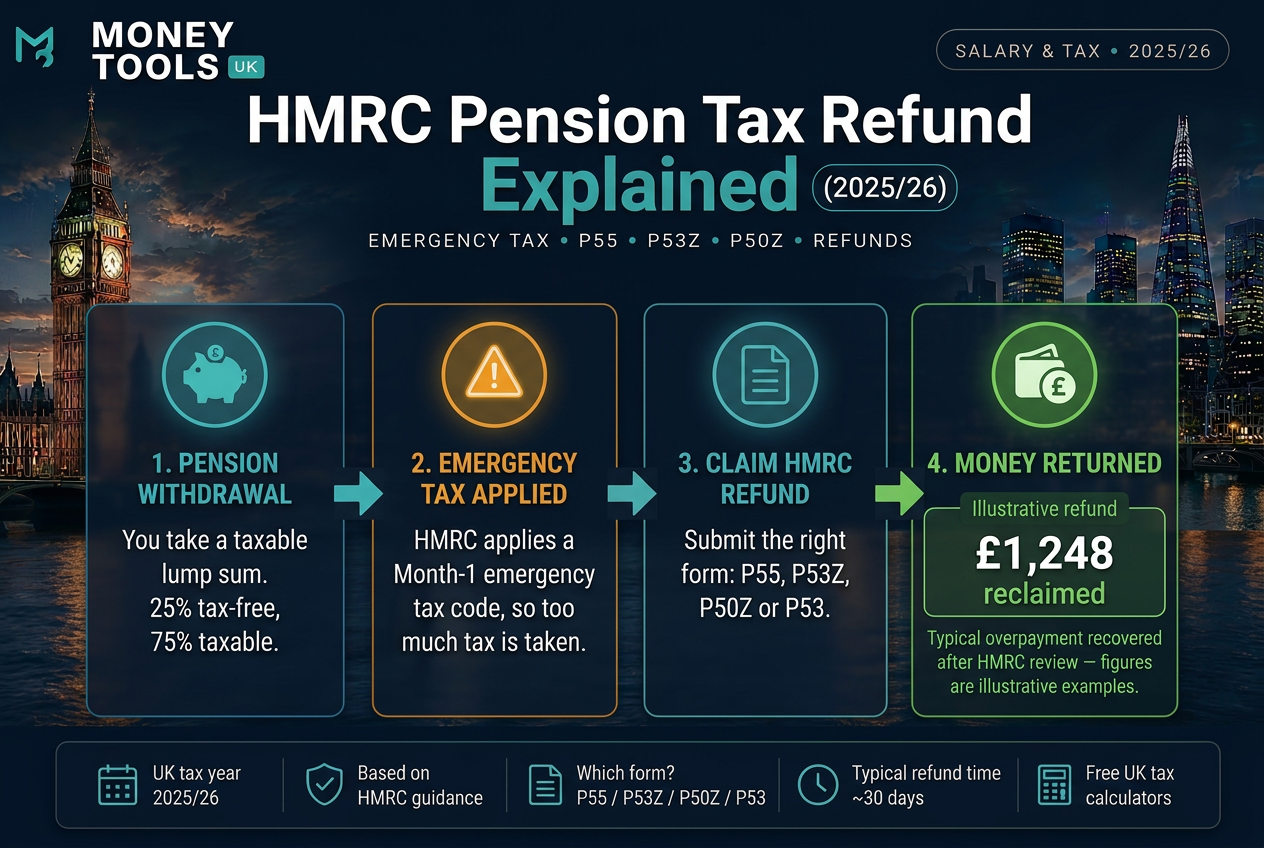

Why HMRC overtaxes pension withdrawals with emergency tax, how pension tax refunds work, and which form to use — P55, P53Z, P50Z or P53 — to reclaim overpaid tax for 2025/26.

Read guide

Learn how UK company car tax works in 2025/26, including Benefit-in-Kind tax, P11D value, CO2 emissions, electric cars, fuel benefit and salary sacrifice examples.

Read guideDisclaimer: This content is for informational purposes only and should not be treated as financial, tax, mortgage, investment or legal advice.