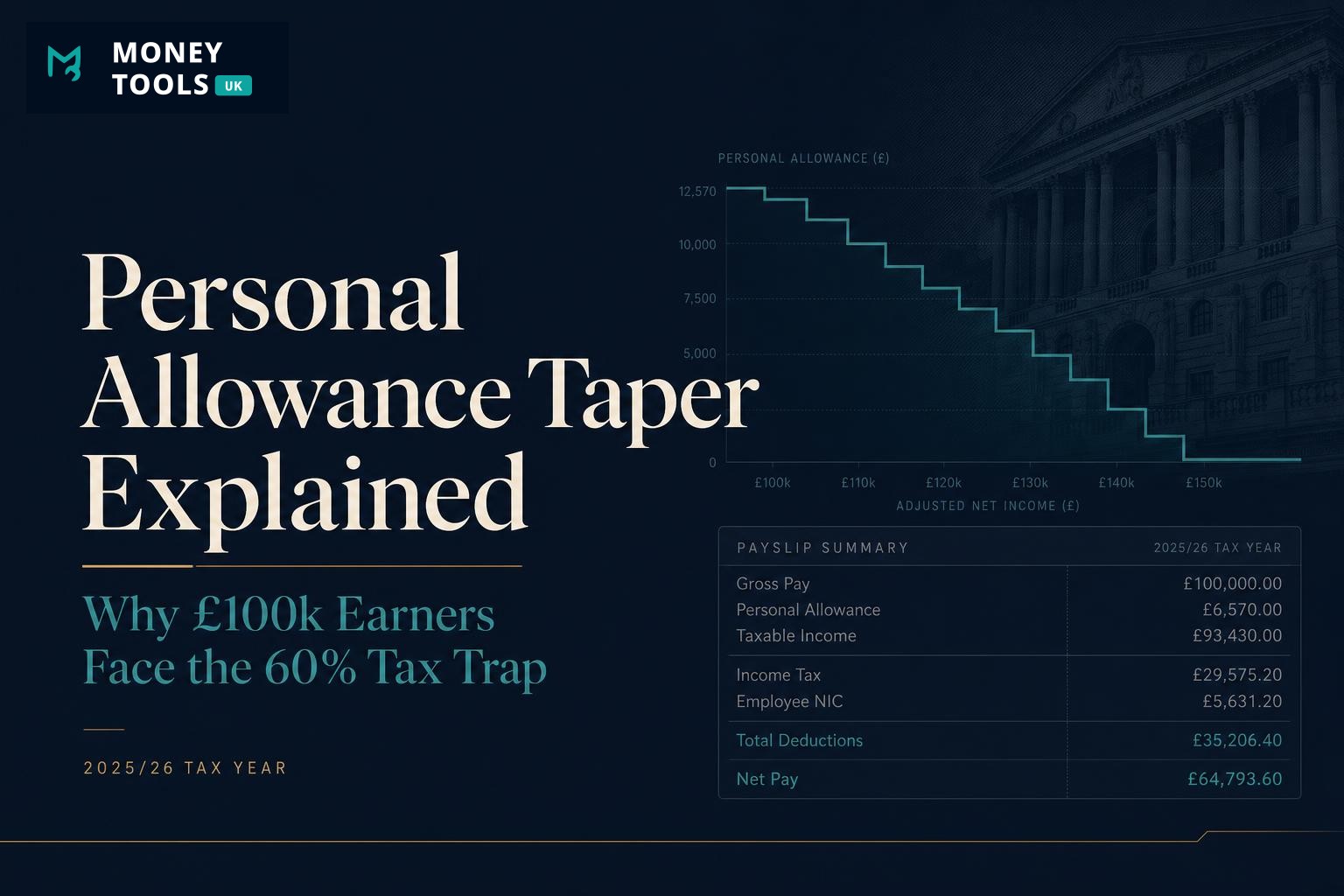

The personal allowance is the slice of income you can earn each year before paying any income tax — £12,570 in the 2025/26 tax year. For most people it simply sits in the background. But once your income climbs above £100,000, that allowance quietly starts to disappear, and the way it disappears creates one of the strangest features of the entire UK tax system: a band of income taxed at an effective 60% — the famous "60% tax trap".

This guide explains, in plain English, exactly how the personal allowance taper works, why it produces a 60% marginal rate, who is affected, and — most importantly — how pension contributions, salary sacrifice and Gift Aid can legally restore the allowance you would otherwise lose.

Updated for 2025/26

The short answer

Calculate your real take-home pay

See exactly how the £100,000 personal allowance taper affects your income. Model your salary, pension contributions, salary sacrifice, bonuses and student loans — and see how much tax you could save.

Allowance

£12,570

Full personal allowance (2025/26)

Taper Start

£100,000

Where the taper begins

Taper End

£125,140

Allowance fully withdrawn

Tax Trap

60%

Effective marginal rate in the trap

Quick summary: for every £2 earned above £100,000, £1 of allowance is lost; the allowance falls from £12,570 to £0 between £100,000 and £125,140, creating an effective 60% marginal rate.

How the personal allowance taper works

Everyone starts the tax year with the same headline allowance of £12,570. The taper is the mechanism HMRC uses to claw that allowance back from higher earners. The rule is simple to state:

- For every £2 your income rises above £100,000, you lose £1 of personal allowance.

- Because £12,570 of allowance is removed at a rate of £1 per £2, it takes exactly £25,140 of extra income to wipe it out.

- That is why the allowance reaches zero at £125,140 (£100,000 + £25,140).

Crucially, the figure that matters is your adjusted net income (explained in detail below), not simply your gross salary. A few quick examples show how the allowance shrinks:

- £100,000: full £12,570 allowance retained.

- £105,000: £5,000 over the threshold → lose £2,500 → allowance of £10,070.

- £110,000: £10,000 over → lose £5,000 → allowance of £7,570.

- £120,000: £20,000 over → lose £10,000 → allowance of £2,570.

- £125,140 and above: allowance is £0.

Why the tax trap is effectively 60%

On the surface, income between £100,000 and £125,140 sits inside the 40% higher-rate band. So why is it described as a 60% trap? The answer is that two things happen to every extra pound at once:

- The pound itself is taxed at 40% (higher rate).

- For every £2 earned, £1 of allowance is lost — and that newly unsheltered pound is also taxed at 40%.

The maths on an extra £2

- 40% on the £2 itself = 80p

- plus 40% on the £1 of allowance you just lost (which is now taxable) = 40p

- Total tax on £2 = £1.20, i.e. 60p in every £1 — a 60% effective marginal rate.

Put another way: every additional £1 you earn between £100,000 and £125,140 leaves you with only about 40p. Add a 2% National Insurance charge and the effective rate is closer to 62%; with a student loan on top it can exceed 70%. This is the single most important reason higher earners use pensions to manage income in this range.

The pay-rise that barely lands

A £10,000 pay rise from £100,000 to £110,000 sounds great — but after 40% tax, the loss of £5,000 of allowance (also taxed at 40%) and 2% National Insurance, many people keep only around £3,800–£4,000 of it. The rest disappears into the 60% trap.

What if your salary rises?

Estimated take-home

£45,357

Marginal tax rate

42%

Extra tax vs £50k

£4,162

Crossing £50,270 pushes additional earnings into the higher-rate tax band (40% income tax + 2% NI).

Example: what happens when your salary rises from £100,000 to £105,000?

The clearest way to feel the 60% trap is to follow a single £5,000 pay rise. Imagine you earn exactly £100,000 and your employer offers a rise to £105,000 — a headline increase that sounds like an extra £5,000. Here is what actually happens in 2025/26 (single PAYE employment, no pension or student loan, England/Wales/NI):

| Figure | Salary £100,000 | Salary £105,000 |

|---|---|---|

| Personal allowance | £12,570 | £10,070 |

| Allowance lost | £0 | £2,500 |

| Income tax | ~£27,432 | ~£30,432 |

| National Insurance | ~£4,011 | ~£4,111 |

| Approx annual take-home | ~£68,557 | ~£70,457 |

Here is the breakdown of where the £5,000 actually goes:

- Personal allowance lost: £5,000 over the threshold means £2,500 of allowance disappears (£1 for every £2), dropping your allowance from £12,570 to £10,070.

- Additional income tax created: roughly £3,000 — £2,000 is 40% on the £5,000 rise, and a further £1,000 is 40% on the £2,500 of allowance you just lost.

- National Insurance impact: only about £100 extra, because earnings above £50,270 are charged at just 2%.

- Approximate take-home difference: around £1,900 more per year — only about 38p of every extra £1.

In plain English: a £5,000 pay rise feels much smaller than expected because more than 60% of it never reaches your bank account. You pay 40% tax on the new income, lose tax-free allowance that is then taxed at 40% as well, and only avoid a big NI hit because you are already above the upper earnings limit. This is exactly why higher earners often redirect a rise like this straight into a pension — see Salary Sacrifice Explained for how to keep the full value.

Worked examples: £100k, £110k, £120k and £125,140

The table below shows how the personal allowance, income tax and approximate take-home pay change across the taper band in 2025/26 (single PAYE employment, no pension or student loan, England/Wales/NI):

| Salary | Allowance left | Income tax | Approx take-home |

|---|---|---|---|

| £100,000 (Example A) | £12,570 | £27,432 | ~£68,557 |

| £110,000 (Example B) | £7,570 | ~£33,432 | ~£72,557 |

| £120,000 (Example C) | £2,570 | ~£39,432 | ~£76,557 |

| £125,140 (Example D) | £0 | ~£42,516 | ~£78,775 |

Notice the pattern in Examples A to D: each £10,000 of extra salary adds only about £4,000 to take-home pay, because roughly £6,000 is lost to the combined effect of 40% tax and the disappearing allowance. From £125,140 onwards the allowance is already gone, so the marginal rate drops back to a "normal" 40% (45% above £125,140 at the additional rate) and pay rises feel meaningful again.

See your exact take-home across the taper

Model any salary between £100k and £125,140 — with pension, salary sacrifice, bonus and student loan — using the UK Take-Home Pay Calculator.

Why many people never notice the taper

For something so expensive, the taper is remarkably easy to miss. There are three main reasons:

- PAYE hides it. Tax is deducted automatically each month, so you never write a cheque to HMRC. The extra tax simply shows up as a smaller-than-expected rise in your net pay.

- Tax codes adjust quietly. HMRC reduces your tax code (for example from 1257L towards 0T) to reflect the lost allowance. The change is buried in a coding notice most people never read.

- The loss is gradual. Because the allowance erodes £1 for every £2, there is no single dramatic moment — just a steadily worsening effective rate as income rises through the band.

The first time many people realise what has happened is when a bonus or pay rise lands and they keep far less of it than expected.

How salary sacrifice can reduce the impact

Salary sacrifice means giving up part of your gross salary in exchange for a non-cash benefit. Because the sacrifice reduces your gross pay before tax, it lowers your adjusted net income — and that is exactly the figure the taper is based on. The most powerful options at this income level are:

- Pension salary sacrifice. Sacrificing salary into your pension reduces adjusted net income pound for pound, restoring lost allowance and saving income tax and National Insurance at the same time.

- Cycle-to-work. The cost of a bike and equipment is taken from gross pay, reducing taxable income (smaller amounts, but still effective).

- Electric vehicle (EV) salary sacrifice. Often a large monthly sacrifice with only a small benefit-in-kind charge, making it a tax-efficient way to lower adjusted net income.

Restoring a lost allowance

What happens if you increase your pension?

New annual take-home

£70,267

Tax & NI saved

£3,410

Into your pension

£5,500

Assumes relief-at-source contributions on a £110,000 salary, no student loan. Higher-rate relief shown as combined tax & NI saved versus 0% pension.

Adjusted net income explained

The taper is not based on your salary, or even your total taxable income — it is based on your adjusted net income (ANI). Getting this figure right is the key to managing the trap.

In simple terms, HMRC calculates adjusted net income like this:

- Start with your total taxable income — salary, bonuses, taxable benefits, rental income, dividends, savings interest and so on.

- Deduct grossed-up Gift Aid donations and certain pension contributions (relief-at-source contributions and the gross value of personal pension payments).

- The result is your adjusted net income — the number compared against the £100,000 threshold.

This is why pension contributions and Gift Aid are so powerful: they don't just attract tax relief, they actively reduce the income figure that drives the taper. Salary sacrifice works slightly differently — it lowers your gross pay at source, so the sacrificed amount never enters your adjusted net income in the first place.

Watch out for bonuses and benefits

Should you deliberately stay under £100,000?

Once people understand the 60% trap, the obvious question is whether they should actively keep their adjusted net income below £100,000. For many UK employees the answer is a qualified yes — but it is a planning decision, not a reason to turn down progression.

Why many people aim to stay under £100,000

Keeping adjusted net income at or below £100,000 preserves the full £12,570 personal allowance and avoids the 60% marginal band entirely. If you have children, it can also keep you under the £100,000 thresholds for tax-free childcare and 30 free hours, which are lost the moment adjusted net income tips over £100,000. For parents, those childcare cliff-edges can be worth thousands of pounds a year — often more than the tax itself.

When it makes sense to "pension down" to £100,000

If your income lands just inside the trap — say £100,000 to £115,000 — redirecting the excess into a pension is usually highly efficient. Every £1 contributed inside the band effectively costs you only around 40p of net pay once the restored allowance is taken into account, so you are buying pension savings at a 60% discount. This is especially compelling if you would otherwise lose childcare support, or if you are happy to lock money away until retirement. The mechanics are covered in Salary Sacrifice Explained.

When pensioning down may not make sense

Pensioning down is not always the right call. It may not suit you if you need the cash now (for a mortgage deposit, school fees or debt), if you are already close to the pension annual allowance, or if you are far from retirement and would rather keep flexible access to your money. Tying up income to dodge tax only helps if locking it away genuinely fits your plans.

Why turning down a pay rise is usually the wrong move

Crucially, the 60% trap is never a reason to refuse a pay rise or promotion. Even inside the band you keep roughly 40p of every extra pound, and once your income clears £125,140 the marginal rate falls back to the standard rates so pay rises feel normal again. A higher salary also lifts your borrowing capacity, bonus base and pension contributions. The smart approach is to accept the rise and then decide how much of it to route into a pension — not to leave money on the table.

The practical takeaway

Common mistakes people make

- Assuming all income is taxed at 60%. Only income within the £100,000–£125,140 band is hit by the trap. Income below £100,000 is taxed normally, and income above £125,140 returns to the standard higher/additional rates.

- Confusing marginal and effective rates. The 60% is a marginal rate (the tax on the next pound), not the rate on your whole salary. Your overall effective rate is much lower.

- Ignoring pension opportunities. Failing to use pension contributions in this band wastes the most valuable tax relief available to most UK employees.

- Misunderstanding bonuses. A bonus paid on top of a £95,000 salary can land squarely in the 60% band — sacrificing it into a pension is often far more efficient than taking the cash.

- Calculating adjusted net income incorrectly. Forget to include taxable benefits or investment income and you'll underestimate how deep into the trap you actually are.

How to legally reduce the tax trap

There are several entirely legitimate ways to manage — or escape — the 60% trap. They all work by reducing your adjusted net income:

- Pension contributions. The most effective lever. Personal or workplace pension contributions reduce adjusted net income and attract relief at the 60% marginal rate inside the trap.

- Salary sacrifice. Pension, EV and cycle-to-work sacrifices lower gross pay before tax and National Insurance.

- Charitable Gift Aid. Grossed-up Gift Aid donations reduce adjusted net income while supporting good causes.

- Tax planning. Timing bonuses, spreading income across tax years, and using ISAs to shelter investment income can all keep adjusted net income below key thresholds.

For many higher earners, bringing adjusted net income back to exactly £100,000 restores the full personal allowance, escapes the 60% trap and — if you have children — can also reduce or remove the High Income Child Benefit Charge at the same time.

Read next

Related £100k tax planning topics

The personal allowance taper rarely sits in isolation. If you are planning around the £100,000 threshold, these closely related topics are worth understanding together:

- Salary sacrifice — the most effective way to lower adjusted net income, restore your allowance and save National Insurance at the same time.

- Pension tax relief — pension contributions reduce adjusted net income and, inside the trap, attract relief worth up to 60%. The UK Take-Home Pay Calculator shows the effect of different contribution levels instantly.

- High Income Child Benefit Charge — a separate clawback that begins at £60,000 of adjusted net income; the same pension and Gift Aid levers that escape the taper can reduce it too.

- £100k salary after tax — a full payslip breakdown of exactly what a £100,000 earner takes home in 2025/26.

- £120k salary after tax — how the numbers look deeper inside the taper band, where most of the allowance is already gone.

Salary Milestone Comparison: How £100,000 Compares

As income rises, tax rates, National Insurance, pension planning and student loan repayments can have a significant impact on take-home pay. Comparing salary milestones helps you understand how much extra income you actually keep as your earnings increase.

| Salary | Annual Take-Home | Monthly Take-Home | Key Tax Milestone | Full Guide |

|---|---|---|---|---|

| £25,000 | £21,520 | £1,793 | Basic-rate band | Calculate £25k take-home pay |

| £30,000 | £25,120 | £2,093 | Basic-rate band | Calculate £30k take-home pay |

| £35,000 | £28,720 | £2,393 | Below higher-rate threshold | Calculate £35k take-home pay |

| £40,000 | £32,320 | £2,693 | Basic-rate taxpayer | View £40k Salary After Tax GuideSee exactly how a basic-rate salary is taxed and your monthly take-home. |

| £45,000 | £35,920 | £2,993 | Approaching higher rate | Calculate £45k take-home pay |

| £50,000 | £39,520 | £3,293 | Edge of the £50,270 threshold | View £50k Salary After Tax GuideLearn what happens as you reach the £50,270 higher-rate threshold. |

| £60,000 | £45,357 | £3,780 | Higher-rate taxpayer; HICBC begins | View £60k Salary After Tax GuideUnderstand higher-rate tax and how the Child Benefit charge starts to bite. |

| £70,000 | £51,157 | £4,263 | Deep in the higher-rate band | View £70k Salary After Tax GuideSee how take-home grows once you're firmly in the higher-rate band. |

| £80,000 | £56,957 | £4,746 | Higher-rate; nearing the £100k taper | View £80k Salary After Tax GuideDiscover your real take-home as you approach the £100k allowance taper. |

| £90,000 | £62,757 | £5,230 | Approaching the £100k taper | View £90k Salary After Tax GuideFind out how to plan pension contributions before the 60% trap hits. |

| £100,000This guide | £68,557 | £5,713 | Personal allowance taper / 60% trap | You are here |

| £120,000 | £78,157 | £6,513 | Inside the 60% trap; allowance nearly gone | Calculate £120k take-home pay |

Estimates assume a single PAYE employment for the 2025/26 tax year in England, Wales or Northern Ireland, with no pension contributions or student loan deductions. Your exact figures will vary.

Many readers compare multiple salary levels before negotiating a pay rise, changing jobs or making pension contribution decisions. Use the guides above to see how take-home pay changes across different income bands.

Model your way out of the 60% trap

Use the UK Take-Home Pay Calculator to test pension contributions, salary sacrifice, bonuses and student loans and see exactly how much allowance you can restore.

Sources & references

This guide references current HMRC and GOV.UK guidance for the 2025/26 UK tax year.

- GOV.UK — Personal Allowance for income over £100,000

- HMRC — Income Tax rates and Personal Allowances

- HMRC — Personal Allowances: adjusted net income

- GOV.UK — Salary sacrifice and the effects on PAYE

- GOV.UK — Tax relief when you donate to charity (Gift Aid)

Last updated

This article was last reviewed on 9 June 2026 and reflects current UK income tax thresholds, the personal allowance taper rules and adjusted net income guidance for the 2025/26 tax year. We review and update this guide whenever HMRC or GOV.UK publishes a material change.

Disclaimer

Money Tools UK provides educational content and calculators only. The figures above are estimates based on standard 2025/26 UK tax rules for England, Wales and Northern Ireland (with Scottish rates noted where relevant) and assume a single PAYE employment with a standard tax code. Individual circumstances may vary. For regulated tax or financial advice, please speak to a qualified accountant or independent financial adviser.

Get new UK finance and property guides from Money Tools UK

Plain-English UK finance insights, tax updates and property investing guides.

Related calculators

UK Take-Home Pay Calculator

The exact calculator this article is built around — open it and run your own numbers.

Open calculatorFrequently asked questions

Related guides

More flagship guides and tools from Money Tools UK.

A plain-English UK guide to checking if HMRC owes you a tax refund: why overpayments happen, how to use your Personal Tax Account, P800 and Simple Assessment, when refunds are automatic, how to claim, and how to avoid tax refund scams.

Read guide

Why HMRC overtaxes pension withdrawals with emergency tax, how pension tax refunds work, and which form to use — P55, P53Z, P50Z or P53 — to reclaim overpaid tax for 2025/26.

Read guide

Learn how UK company car tax works in 2025/26, including Benefit-in-Kind tax, P11D value, CO2 emissions, electric cars, fuel benefit and salary sacrifice examples.

Read guideDisclaimer: This content is for informational purposes only and should not be treated as financial, tax, mortgage, investment or legal advice.