You can transfer

£1,260

Annual saving

Up to £252

Backdate up to

4 years

Marriage Allowance is one of the simplest tax reliefs in the UK — yet millions of eligible couples have never claimed it. This guide explains exactly how it works, who qualifies, how much you could save and how to apply in minutes.

Many couples are unknowingly paying more tax than necessary. Marriage Allowance allows eligible married couples and civil partners to transfer part of their Personal Allowance from the lower earner to the higher earner, potentially reducing their annual tax bill.

Despite being one of the most straightforward tax reliefs available, millions of eligible couples either do not know about it or have never got around to claiming. Worse still, many who could claim assume the process is complicated — it isn't. A claim takes minutes and, once made, usually renews automatically each year.

This guide explains exactly how Marriage Allowance works, who qualifies, how much you can save and how to apply. Every figure reflects the 2025/26 tax year for England, Wales and Northern Ireland (Scottish taxpayers can also claim, with the same £1,260 transfer).

The short answer

- What is Marriage Allowance?

- A tax relief that lets the lower-earning partner transfer 10% of their Personal Allowance (£1,260 in 2025/26) to their spouse or civil partner.

- Who benefits?

- The higher-earning partner receives the tax reduction. The couple must be married or in a civil partnership — cohabiting couples cannot claim.

- How much can you save?

- Up to approximately £252 per tax year. Claims can also be backdated up to four years, potentially worth over £1,000.

What is Marriage Allowance?

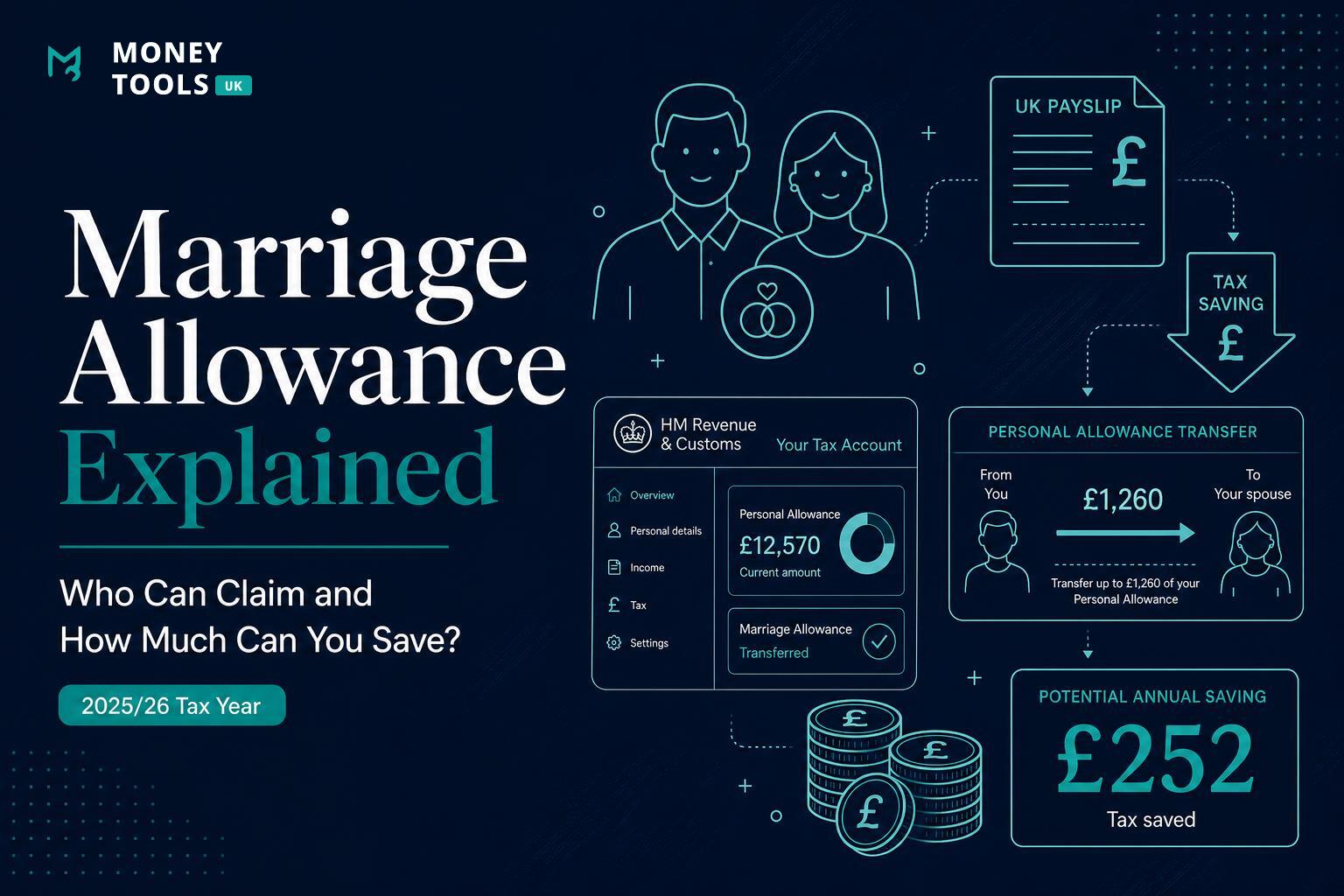

Marriage Allowance was introduced by HMRC to help lower-income married couples and civil partners keep more of their household income. It works by allowing the partner who earns the least — typically someone who doesn't use all of their tax-free Personal Allowance — to transfer part of that unused allowance to the higher earner.

In 2025/26 the standard Personal Allowance is £12,570 — the amount of income you can receive before paying any Income Tax. Marriage Allowance lets the lower earner give up 10% of this allowance (£1,260) and pass it to their partner, reducing the partner's tax bill.

- Introduced by HMRC to support lower-income couples.

- Available to married couples and civil partners only.

- Not available to unmarried couples, even if you live together or have children.

- Renews automatically each year once claimed, unless your circumstances change.

In plain English

How much can you save?

Transferred allowance

£1,260

10% of the £12,570 Personal Allowance, moved from the lower earner to the higher earner.

Potential tax reduction

£252

The higher earner's tax bill falls by 20% of £1,260 for the 2025/26 tax year.

The saving is calculated simply: the recipient is a basic-rate (20%) taxpayer, so transferring £1,260 of tax-free allowance reduces their tax bill by 20% × £1,260 = £252. The exact figure can vary by a pound or two depending on rounding, but £252 is the headline saving for 2025/26.

Calculate Your Take-Home Pay

Every salary and tax situation is different. Use our free UK Take-Home Pay Calculator to estimate Income Tax, National Insurance, student loan deductions and pension contributions — and see where Marriage Allowance fits in.

Who can claim?

To qualify for Marriage Allowance in 2025/26, you must be married or in a civil partnership and meet two income conditions between you.

Partner A (transfers allowance)

- Income below the £12,570 Personal Allowance (a non-taxpayer).

- Has unused Personal Allowance to give away.

Partner B (receives allowance)

- A basic-rate (20%) taxpayer, with income between £12,571 and £50,270.

- Receives the £1,260 allowance and pays less tax.

In short: one partner earns under the Personal Allowance, the other is a basic-rate taxpayer. If that describes you, you almost certainly qualify. (In Scotland the recipient must pay the starter, basic or intermediate rate, broadly matching the same income band.)

Who cannot claim?

Marriage Allowance is deliberately targeted at lower-income couples, so several groups are excluded.

- Higher-rate taxpayers — if the recipient earns more than £50,270, they pay tax at 40% and are not eligible.

- Additional-rate taxpayers — those earning above £125,140 cannot claim.

- Unmarried couples — cohabiting partners, regardless of how long they've lived together or whether they have children, cannot claim.

- Couples where both pay tax at the basic rate and neither has spare allowance — there is nothing to transfer.

Watch the higher-rate cut-off

Example — does not qualify: Sam earns £58,000 (a higher-rate taxpayer) and his husband earns £9,000. Even though one partner has spare allowance, the recipient is a higher-rate taxpayer, so they cannot claim.

How the transfer works

The mechanics are simple. The lower earner applies to give up £1,260 of their Personal Allowance, HMRC moves it to the higher earner, and the higher earner's tax-free allowance increases — reducing their tax bill.

- Partner A has a £12,570 Personal Allowance (unused)

- Transfer £1,260 to Partner B

- Partner B's allowance rises to £13,830

- Partner B pays £252 less tax this year

Importantly, the transfer is a fixed £1,260 — you cannot choose a smaller amount. The lower earner's own allowance falls to £11,310, but because their income is below that figure they usually pay no extra tax.

Worked examples

These examples show how Marriage Allowance plays out for three typical couples in 2025/26.

Example 1 — £10,000 and £30,000

- Partner A: £10,000 income — below the £12,570 allowance, pays no tax, has spare allowance to transfer.

- Partner B: £30,000 income — a basic-rate taxpayer.

- Result: Partner A transfers £1,260. Partner B's allowance rises to £13,830, saving the couple £252. Partner A still pays no tax.

Example 2 — £8,000 and £40,000

- Partner A: £8,000 income — well below the allowance.

- Partner B: £40,000 income — comfortably a basic-rate taxpayer.

- Result: The £1,260 transfer reduces Partner B's tax by £252. Partner A's reduced £11,310 allowance still comfortably covers their £8,000 income, so they pay no tax.

Example 3 — £12,000 and £50,000

- Partner A: £12,000 income — just under the allowance, with a small amount spare.

- Partner B: £50,000 income — still inside the basic-rate band (below £50,270), so eligible.

- Result: Partner B saves £252. Note Partner A's allowance drops to £11,310, which is below their £12,000 income, so they would pay 20% tax on the £690 difference (about £138) — but the couple is still better off overall by roughly £114.

The key takeaway

Common mistakes

- Assuming cohabiting couples qualify. You must be legally married or in a civil partnership — living together is not enough.

- Believing both partners receive tax relief. Only the higher earner's tax bill is reduced; the allowance simply moves across.

- Thinking higher-rate taxpayers qualify. If the recipient earns above £50,270, the couple is not eligible.

- Forgetting to backdate claims. You can usually claim for up to four previous tax years, which many people overlook.

- Not cancelling after a change. If you separate or the recipient becomes a higher-rate taxpayer, the claim should be stopped.

How to apply

Applying is free and quick. The lower-earning partner must make the claim, because they are the one giving up part of their allowance.

- 1Go to the official GOV.UK Marriage Allowance service and start the online application.

- 2Sign in with (or create) your Government Gateway ID. You'll need both partners' National Insurance numbers and a form of ID.

- 3Confirm your income details so HMRC can check eligibility, and submit.

- 4HMRC updates the recipient's tax code (usually adding an "M" suffix). The relief then appears automatically through PAYE.

Once approved, the allowance is usually applied within a couple of months and the claim renews automatically each year — you do not need to reapply unless your circumstances change.

Backdating claims

One of the most valuable — and most overlooked — features of Marriage Allowance is that eligible couples can usually backdate a claim for up to four previous tax years, provided they were eligible in those years. HMRC pays any refund for past years as a lump sum or via a tax-code adjustment.

Backdating example

A couple who were eligible but never claimed could backdate four years:

4 years × £252 = £1,008

Plus the current year's £252, that's a potential £1,260 back in total. (The exact saving per year reflects that year's rates, which were very similar.)

Marriage Allowance and PAYE

For most employees the relief is delivered automatically through PAYE. When a claim is approved, HMRC changes the recipient's tax code — most commonly adding the letter M (for the partner receiving the allowance) or N (for the partner transferring it).

- Tax code changes: the recipient's code rises (e.g. from 1257L to 1383M), giving more tax-free pay each period.

- How relief appears: slightly higher take-home pay, spread across the year rather than as a single refund.

- Payroll adjustments: your employer simply applies the new tax code — you don't need to do anything.

Marriage Allowance and Self Assessment

If either partner completes a Self Assessment tax return, Marriage Allowance is still claimed through the GOV.UK service (or noted on the return), and HMRC applies the relief when calculating the tax due.

- Reporting: the transfer is reflected in your Self Assessment calculation rather than only via your tax code.

- How HMRC applies it: the recipient's tax liability is reduced by up to £252, and any backdated years can be settled through the return or a separate refund.

Related guides

Marriage Allowance is one piece of the wider UK tax picture. These guides help you understand how Income Tax, allowances and take-home pay fit together.

- £20k Salary After Tax UK — take-home pay and deductions on a £20,000 salary.

- £30k Salary After Tax UK — how a basic-rate salary is taxed in full.

- £35k Salary After Tax UK — tax and take-home pay on a £35,000 salary.

- Child Benefit Tax Charge Explained — how the High Income Child Benefit Charge works.

- Salary Sacrifice Explained — cut Income Tax and National Insurance with pension sacrifice.

- Adjusted Net Income Explained — the hidden number that controls your tax bill.

Calculate Your Take-Home Pay

Use the Money Tools UK Take-Home Pay Calculator to estimate Income Tax, National Insurance, student loan deductions and pension contributions.

Sources & references

This guide reflects official UK government and HMRC guidance for the 2025/26 tax year.

- GOV.UK — Marriage Allowance

- GOV.UK — Marriage Allowance: how it works

- GOV.UK — Income Tax rates and Personal Allowances

- HMRC — Transferable tax allowances for married couples and civil partners

Last updated

This article was last reviewed on 16 June 2026 and reflects UK Income Tax, Personal Allowance and Marriage Allowance rules for the 2025/26 tax year. We refresh this guide each time HMRC publishes a material change.

Reviewed by Money Tools UK Editorial Team

This guide was reviewed for accuracy against HMRC and GOV.UK guidance for the 2025/26 tax year. We regularly update our salary and tax content when thresholds, allowances or eligibility rules change.

Last reviewed: 16 June 2026

Disclaimer

Money Tools UK provides educational content and calculators only. Figures are estimates based on standard 2025/26 UK tax rules and assume eligibility conditions are met. Individual circumstances vary. For regulated tax or financial advice, please speak to a qualified accountant or independent financial adviser.

Get new UK finance and property guides from Money Tools UK

Plain-English UK finance insights, tax updates and property investing guides.

Related calculators

UK Take-Home Pay Calculator

The exact calculator this article is built around — open it and run your own numbers.

Open calculatorFrequently asked questions

Related guides

More flagship guides and tools from Money Tools UK.

A plain-English UK guide to checking if HMRC owes you a tax refund: why overpayments happen, how to use your Personal Tax Account, P800 and Simple Assessment, when refunds are automatic, how to claim, and how to avoid tax refund scams.

Read guide

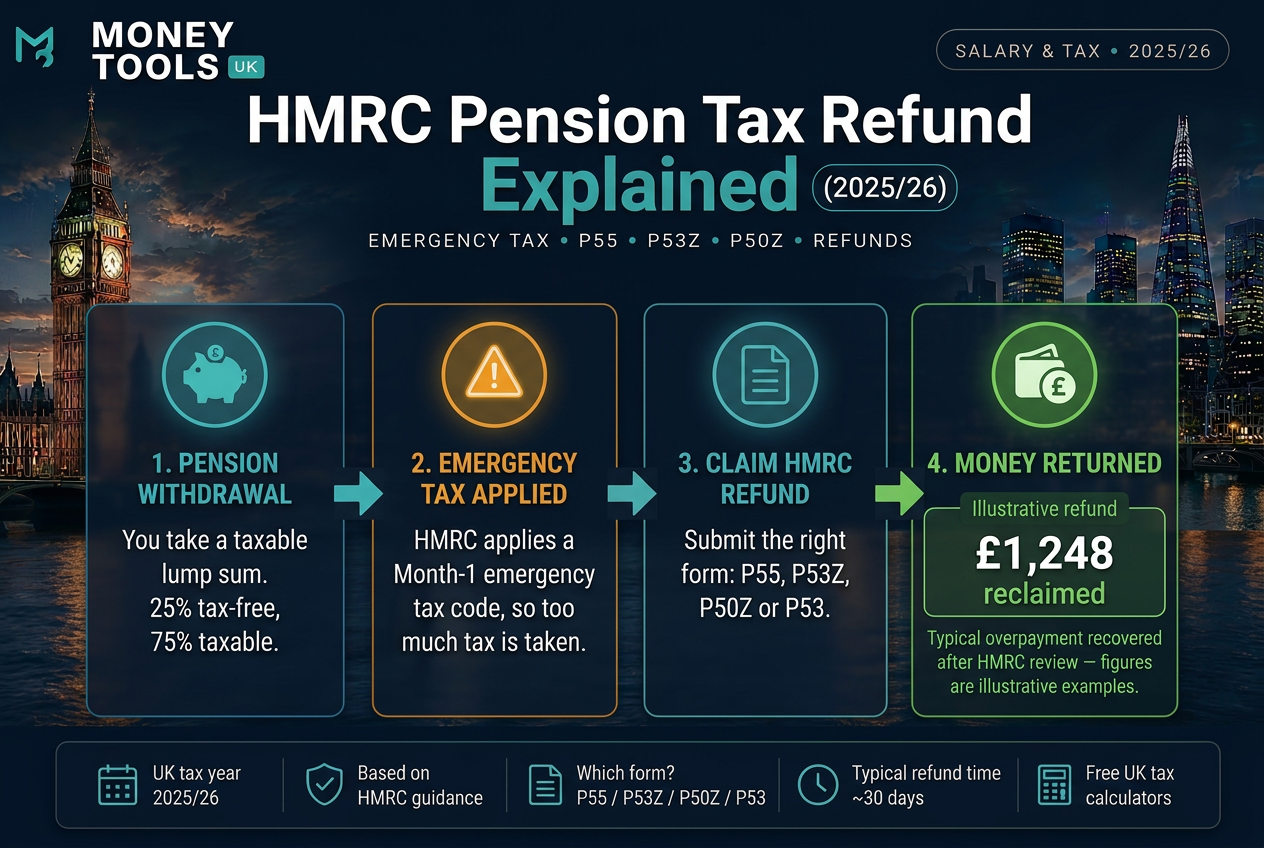

Why HMRC overtaxes pension withdrawals with emergency tax, how pension tax refunds work, and which form to use — P55, P53Z, P50Z or P53 — to reclaim overpaid tax for 2025/26.

Read guide

Learn how UK company car tax works in 2025/26, including Benefit-in-Kind tax, P11D value, CO2 emissions, electric cars, fuel benefit and salary sacrifice examples.

Read guideDisclaimer: This content is for informational purposes only and should not be treated as financial, tax, mortgage, investment or legal advice.