Most UK taxpayers have never heard of Adjusted Net Income (ANI). Yet this single figure can determine:

- Whether you lose Child Benefit

- Whether you lose your Personal Allowance

- Whether you pay the High Income Child Benefit Charge

- Whether your pension contributions reduce your tax bill

- Whether charitable donations reduce your taxable income

In many cases, two people earning the same salary can face completely different tax outcomes — simply because their Adjusted Net Income is different. This guide explains exactly what Adjusted Net Income is, how HMRC calculates it, and how understanding it can potentially save thousands of pounds in tax.

Updated for 2025/26

The short answer

Definition

- It is not the same as your salary or your gross income.

- It includes all taxable income — salary, bonuses, rental income, interest and dividends.

- It is reduced by gross pension contributions, Gift Aid donations and certain trading losses.

- It is the figure that drives the Child Benefit charge, the £100,000 Personal Allowance taper and several other tax limits.

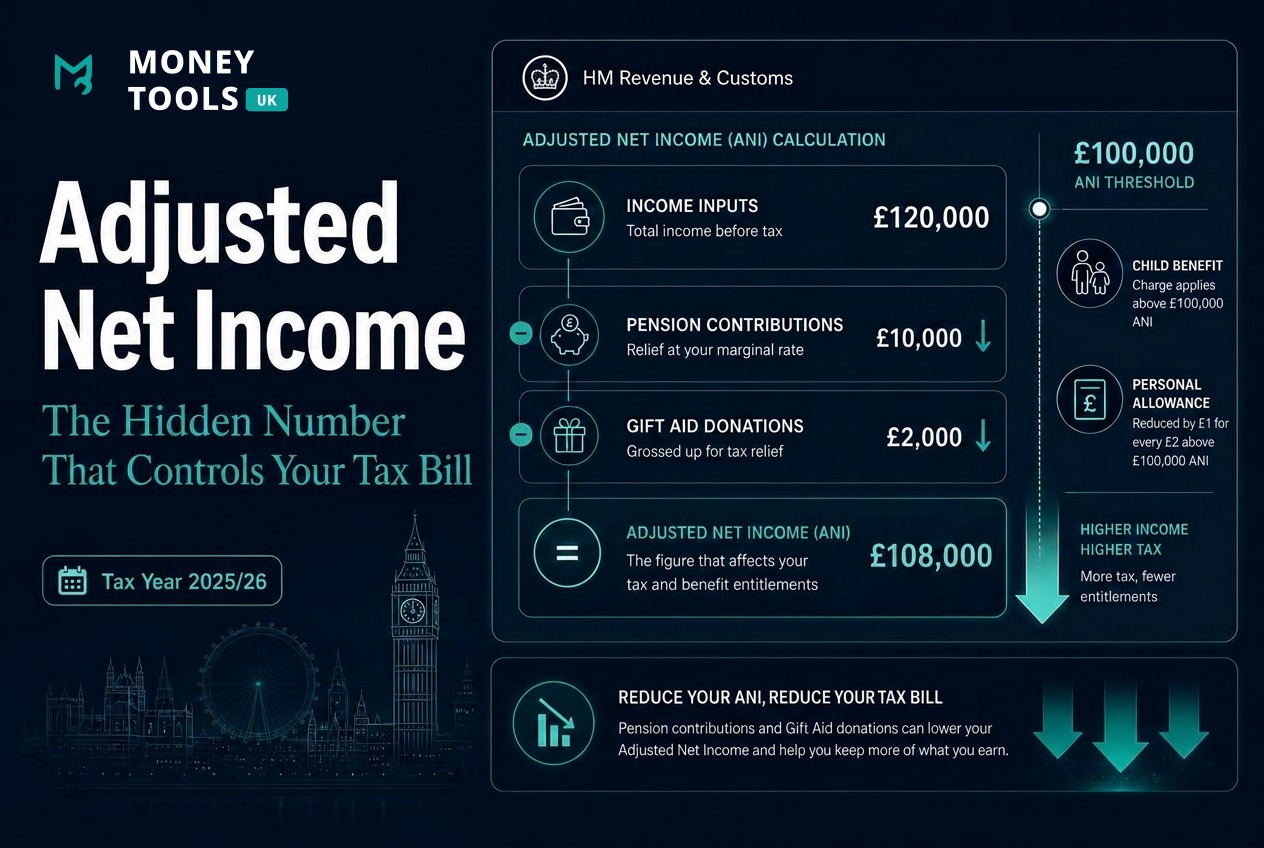

What is Adjusted Net Income?

Adjusted Net Income is a specific HMRC measure of income used to test eligibility for certain allowances and to trigger certain tax charges. It starts with your total taxable income from all sources and then subtracts a small set of tax-relievable deductions.

The key insight is that your headline salary is only the starting point. Two people on £110,000 can have wildly different Adjusted Net Income: one who pays £15,000 into a pension has an ANI of £95,000, while one who pays nothing has an ANI of £110,000. That difference decides whether they keep their Personal Allowance.

Why ANI matters

Adjusted Net Income is often more important than your headline salary, because it is the figure HMRC actually uses to decide how much tax you pay and what you can keep.

Adjusted Net Income affects:

- ✓Child Benefit

- ✓Personal Allowance

- ✓Effective tax rate

- ✓Pension planning

- ✓Gift Aid relief

- ✓Higher-rate tax planning

Because so many tax rules hinge on it, knowing your Adjusted Net Income — and being able to influence it — is one of the most powerful pieces of personal tax planning available to UK taxpayers.

How HMRC calculates ANI

The calculation follows a simple structure: add up all your taxable income, then subtract your tax-relievable deductions.

| Step | Includes |

|---|---|

| Start with total income | Employment income, bonuses, rental income, interest, dividends |

| Minus deductions | Gross pension contributions, Gift Aid donations, certain trading losses |

| Equals | Adjusted Net Income |

Worked example

In this example, bringing Adjusted Net Income down to exactly £100,000 preserves the full Personal Allowance — because the taper only begins above £100,000. The pension contribution does double duty: it builds retirement savings and protects valuable allowances.

How to Find Your Adjusted Net Income

Most employees will never see Adjusted Net Income listed on a payslip, P60 or tax code notice.

To estimate your Adjusted Net Income:

- Add together all taxable income:

- salary

- bonuses

- rental income

- dividends

- taxable savings interest

- self-employment profits

- Deduct:

- gross pension contributions

- Gift Aid donations

- eligible reliefs

- The result is your estimated Adjusted Net Income.

If you complete a Self Assessment tax return, HMRC will normally calculate this figure automatically as part of your annual tax assessment.

Tip

What counts as income?

For Adjusted Net Income, HMRC generally counts all taxable income sources. The most common are:

- Employment income — your salary and wages

- Bonuses — added to your earnings for the year

- Rental income — taxable profit from let property

- Dividends — from shares and company distributions

- Interest — taxable savings interest

- Self-employment profits — trading income after allowable expenses

As a general rule, if income is taxable, it counts towards Adjusted Net Income. Tax-free income — such as ISA interest or the tax-free element of certain benefits — does not.

What reduces ANI?

Only a small set of deductions reduce Adjusted Net Income — but they are powerful. The three main ones are:

- Pension contributions — the gross amount paid into a registered pension

- Gift Aid donations — the grossed-up value of charitable gifts

- Trading loss relief — certain losses set against income

| Increases ANI | Reduces ANI |

|---|---|

| Salary and wages | Gross pension contributions |

| Bonuses | Gift Aid donations |

| Rental, interest, dividends | Certain trading losses |

ANI and Child Benefit

The High Income Child Benefit Charge is based entirely on Adjusted Net Income — not salary, and not household income:

- ANI below £60,000 — no charge; you keep all your Child Benefit.

- ANI between £60,000 and £80,000 — a partial charge claws back 1% for every £200 over £60,000.

- ANI above £80,000 — a full charge effectively repays all of your Child Benefit.

Consider two parents, each earning £70,000. One pays £12,000 into a pension, dropping their ANI to £58,000 — so they pay no charge. The other pays nothing, keeps an ANI of £70,000, and repays 50% of their Child Benefit. Same salary, very different outcomes — driven entirely by Adjusted Net Income.

For the full mechanics, worked examples and the household income paradox, read Child Benefit Tax Charge Explained (2025/26).

ANI and the Personal Allowance taper

Once Adjusted Net Income climbs above £100,000, your Personal Allowance is reduced by £1 for every £2 of income above that threshold. By the time ANI reaches £125,140, the £12,570 Personal Allowance is lost entirely.

The 60% tax trap

Example: with an ANI of £110,000, you are £10,000 over the threshold, so you lose £5,000 of Personal Allowance — leaving just £7,570. Paying £10,000 into a pension restores the full £12,570 allowance and saves tax at that punishing 60% effective rate.

Learn more in Personal Allowance Taper Explained (2025/26).

ANI and pension contributions

Pension contributions are the single most effective way to reduce Adjusted Net Income, because the gross contribution is deducted in full:

- Salary = £110,000

- Gross pension contribution = £10,000

- Adjusted Net Income falls to £100,000

- Full Personal Allowance restored

This is why pension planning is so powerful for higher earners: the £10,000 contribution not only grows your retirement pot, it also escapes the 60% effective tax band — meaning the real cost of the contribution can be remarkably low. Salary sacrifice is often the most efficient route, as it also reduces National Insurance.

See Salary Sacrifice Explained (2025/26) for how to set this up correctly.

ANI and Gift Aid donations

Charitable donations made under Gift Aid also reduce Adjusted Net Income. HMRC counts the grossed-up value of the donation (your gift plus the basic-rate tax the charity reclaims).

Worked example

For higher and additional-rate taxpayers, Gift Aid is doubly efficient: it supports a cause you care about, reduces your ANI, and gives you extra tax relief through your tax return.

Worked examples

These examples show how Adjusted Net Income — not salary — drives the outcome.

Example 0 — £62,000 salary and Child Benefit

A parent earning £62,000 has Adjusted Net Income £2,000 above the Child Benefit threshold.

Without any planning:

- ANI = £62,000

- High Income Child Benefit Charge applies

If they make a £2,000 gross pension contribution:

- ANI falls to £60,000

- Child Benefit charge is eliminated

- Pension savings increase

This example demonstrates why understanding Adjusted Net Income can have a direct impact on family finances even when income is only slightly above a tax threshold.

Example 1 — £65,000 salary, Child Benefit recipient

A parent earning £65,000 is £5,000 over the £60,000 Child Benefit threshold, facing a 25% charge. By paying £5,000 (gross) into a pension, their Adjusted Net Income falls to £60,000 — removing the charge entirely and keeping 100% of their Child Benefit.

Example 2 — £105,000 salary, restoring the Personal Allowance

With an ANI of £105,000, this taxpayer loses £2,500 of Personal Allowance. A £5,000 gross pension contribution brings ANI back to £100,000, restoring the full £12,570 allowance and avoiding the 60% effective tax band.

Example 3 — £120,000 salary, using pension contributions

At £120,000 ANI, £20,000 over the threshold means £10,000 of Personal Allowance is lost. A £20,000 gross pension contribution reduces ANI to £100,000, fully restoring the allowance and saving tax at around 60% on the affected slice of income.

Common mistakes

- Believing salary alone determines tax charges. It's Adjusted Net Income that matters, not your headline pay.

- Ignoring bonuses. A bonus is added to income for the year and can push you over a threshold.

- Ignoring pension relief. Gross pension contributions reduce ANI — overlooking this can cost thousands.

- Confusing taxable income with ANI. ANI is taxable income minus specific deductions, not the same figure.

- Forgetting Gift Aid. Grossed-up donations also reduce ANI and are easy to miss.

How to legally reduce your ANI

Reducing your Adjusted Net Income is entirely legitimate when done through HMRC-approved reliefs. The main routes are:

- Pension contributions — the gross amount reduces ANI directly.

- Salary sacrifice — lowers taxable salary and saves National Insurance too.

- Gift Aid donations — the grossed-up value reduces ANI.

- Tax-efficient planning — timing income, bonuses and contributions across tax years.

Stay compliant

Check how pensions and bonuses change your Adjusted Net Income

Use the Money Tools UK Take-Home Pay Calculator to model your salary, bonuses, pension contributions and salary sacrifice — and see how your Adjusted Net Income affects Child Benefit and your Personal Allowance.

Related guides

- Child Benefit Tax Charge Explained — how ANI decides the £60k–£80k charge.

- Personal Allowance Taper Explained — the 60% trap above £100,000.

- Salary Sacrifice Explained — the most effective way to cut your ANI.

- How Bonuses Are Taxed in the UK — why a bonus pushes up your ANI.

- £100k Salary After Tax UK — take-home pay at the Personal Allowance taper.

- £120k Salary After Tax UK — take-home pay above the taper threshold.

Sources & references

This guide references current HMRC and GOV.UK guidance for the 2025/26 UK tax year.

- GOV.UK — Personal Allowances: adjusted net income

- HMRC — Income Tax rates and Personal Allowances

- GOV.UK — Personal Allowance for income over £100,000

- GOV.UK — High Income Child Benefit Charge

- GOV.UK — Tax relief when you donate to charity (Gift Aid)

- GOV.UK — Tax relief on private pension contributions

Last updated

This article was last reviewed on 11 June 2026 and reflects the Adjusted Net Income rules, Child Benefit thresholds and Personal Allowance taper confirmed for the 2025/26 UK tax year. We refresh this guide each time HMRC publishes a material change.

Disclaimer

Money Tools UK provides educational content and calculators only. The figures above are estimates based on standard 2025/26 UK tax rules and assume straightforward circumstances. They do not account for benefits in kind, pension annual-allowance limits, Scottish Income Tax bands, or personal circumstances that may change your actual liability. For regulated tax or financial advice, please speak to a qualified accountant or independent financial adviser.

Get new UK finance and property guides from Money Tools UK

Plain-English UK finance insights, tax updates and property investing guides.

Related calculators

UK Take-Home Pay Calculator

The exact calculator this article is built around — open it and run your own numbers.

Open calculatorFrequently asked questions

Related guides

More flagship guides and tools from Money Tools UK.

A plain-English UK guide to checking if HMRC owes you a tax refund: why overpayments happen, how to use your Personal Tax Account, P800 and Simple Assessment, when refunds are automatic, how to claim, and how to avoid tax refund scams.

Read guide

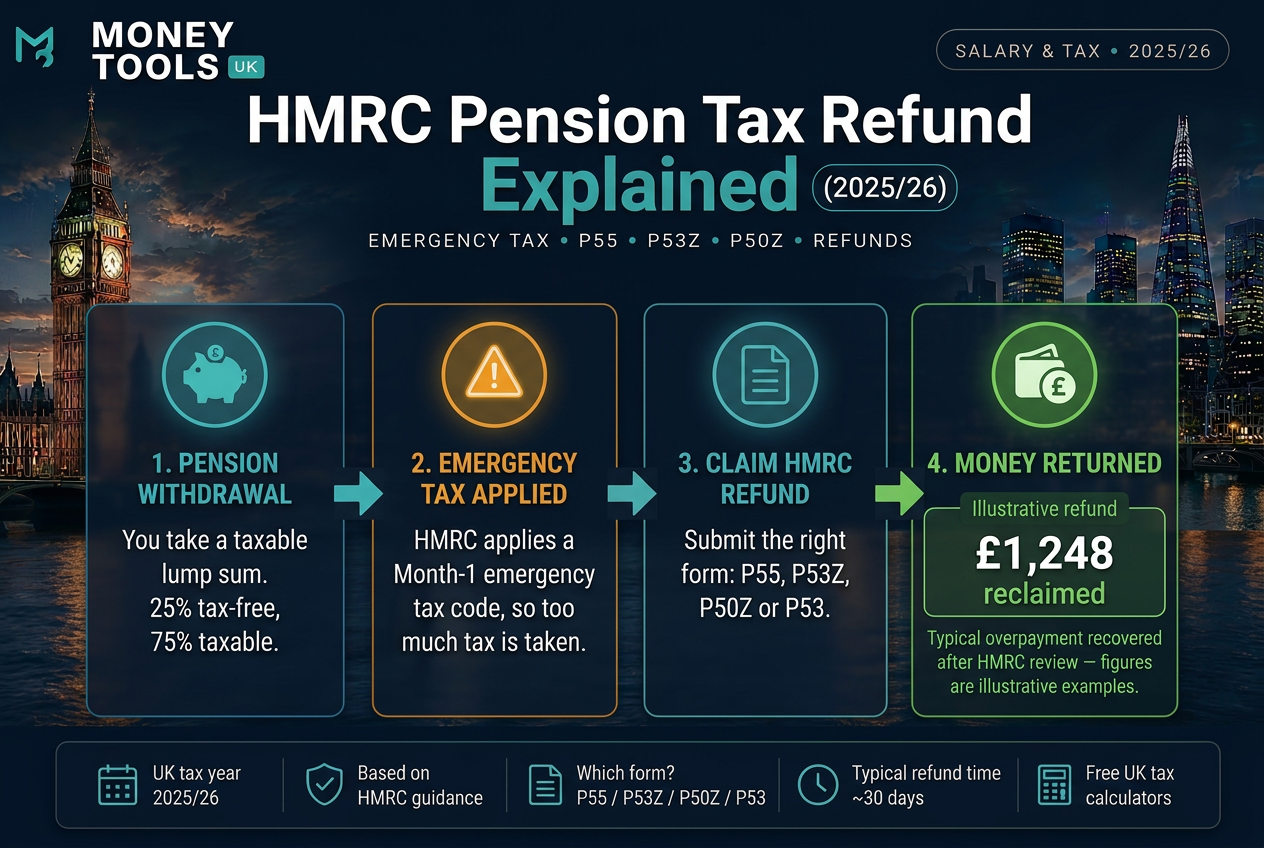

Why HMRC overtaxes pension withdrawals with emergency tax, how pension tax refunds work, and which form to use — P55, P53Z, P50Z or P53 — to reclaim overpaid tax for 2025/26.

Read guide

Learn how UK company car tax works in 2025/26, including Benefit-in-Kind tax, P11D value, CO2 emissions, electric cars, fuel benefit and salary sacrifice examples.

Read guideDisclaimer: This content is for informational purposes only and should not be treated as financial, tax, mortgage, investment or legal advice.