Taxed as

PAYE employee

Key cost

Employer's NI

Typical take-home

55–65%

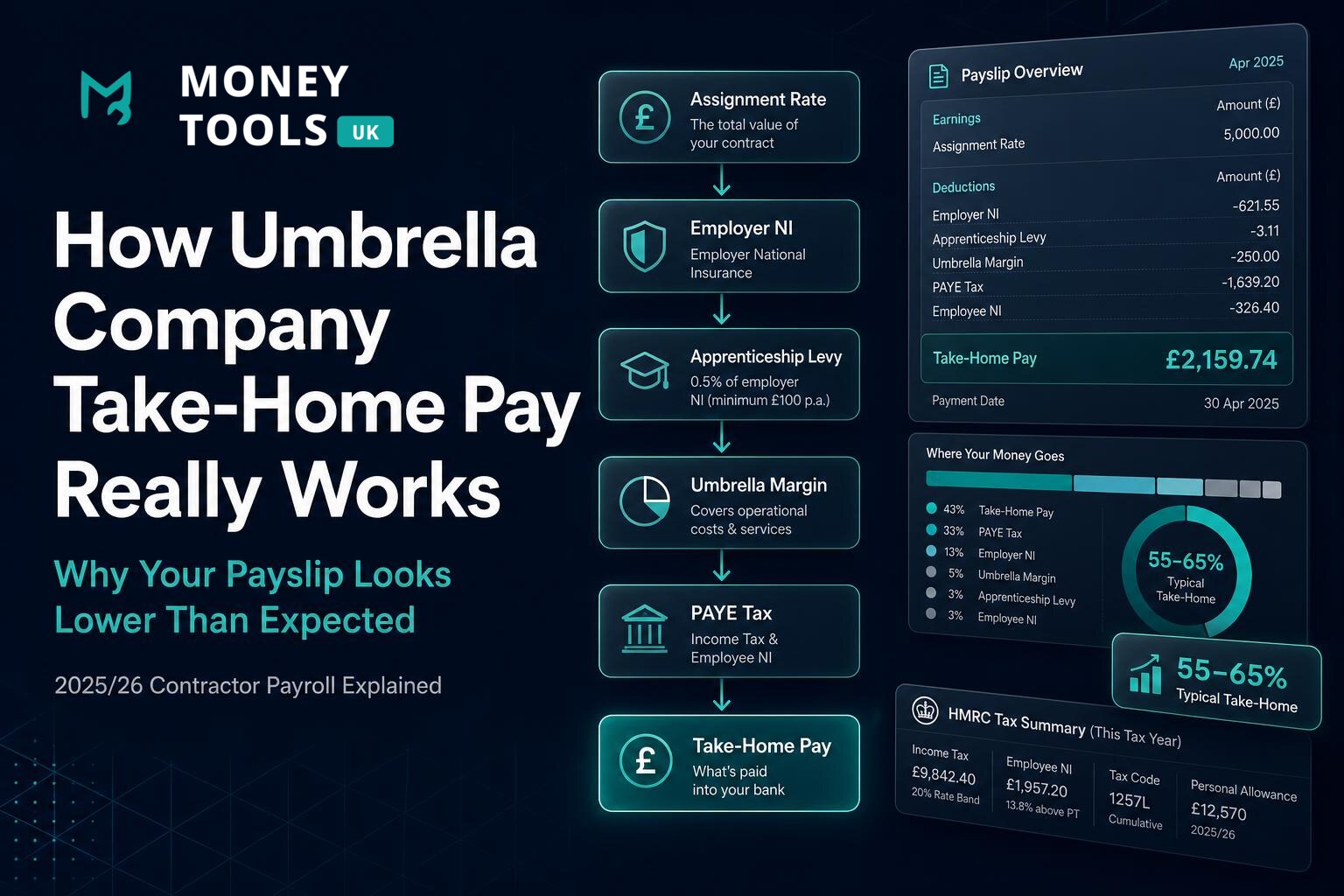

Your assignment rate is not your salary. Several employment costs come out of the contract income before any salary is calculated — which is why umbrella take-home pay is usually lower than the headline day rate suggests.

Many UK contractors are surprised when they receive their first umbrella company payslip. You might agree a contract worth £500 or £600 per day, only to discover your take-home pay is significantly lower than expected.

The reason is simple: umbrella company workers are treated as employees for tax purposes, and several deductions are applied before salary reaches your bank account.

In this guide we explain exactly how umbrella company take-home pay works in the 2025/26 tax year, including employer's National Insurance, employee National Insurance, Income Tax, the Apprenticeship Levy, umbrella margin fees, pension contributions and student loan deductions — with worked examples so you can understand where every pound goes.

The short answer

- What happens to your money?

- An umbrella company receives payment from your agency or client and processes that income through PAYE.

- Deducted before salary

- Employer's National Insurance, the Apprenticeship Levy and the umbrella margin are taken from the contract income first.

- Deducted from salary

- The remainder is your taxable salary, subject to Income Tax, employee NI, student loan repayments and pension contributions. What's left is your take-home pay.

How umbrella pay works step-by-step

Understanding the flow of money is the key to making sense of an umbrella payslip. Here is the journey your contract income takes.

Step 1: The client pays the agency

The end client pays the recruitment agency for the work you carry out.

Step 2: The agency pays the umbrella company

The agency sends your contract income to the umbrella company. This amount is usually called the assignment rate — and it is not your salary.

Step 3: Employment costs are deducted

Before calculating your salary, the umbrella company typically deducts the costs of running payroll:

- Employer's National Insurance

- Apprenticeship Levy

- Umbrella company margin

Step 4: Taxable salary is calculated

The remaining amount becomes your gross taxable salary, and PAYE is applied to it.

Step 5: PAYE deductions are applied

Your salary may then be subject to:

- Income Tax

- Employee National Insurance

- Student loan repayments (if applicable)

- Pension contributions (if applicable)

The remainder becomes your take-home pay.

See your umbrella take-home pay

Use our free Umbrella Company Calculator to estimate PAYE, employee NI, employer NI, the Apprenticeship Levy and the umbrella margin for the 2025/26 tax year.

Why umbrella payslips look confusing

Many contractors mistakenly believe that the assignment rate equals salary. This is not correct.

The assignment rate must first cover employment costs before any salary can be paid. Once you understand this distinction, most of the confusion surrounding umbrella payslips disappears.

Assignment rate ≠ salary

Example: £500 per day contractor

To see how this works in practice, consider these assumptions:

- Day rate: £500 per day

- Working pattern: 5 days per week

- Tax code: standard PAYE

- No pension salary sacrifice

- No student loan

That gives an approximate annual contract value of around £130,000. Before salary is calculated, deductions may include:

- Employer's National Insurance

- Apprenticeship Levy

- Umbrella margin

The remaining amount is then processed through PAYE. Although the exact figures vary between providers, many contractors discover their take-home pay is substantially lower than the headline contract value — typically landing around 55%–65% of the assignment rate once all deductions are applied.

Always check a Key Information Document

Why are you paying employer's National Insurance?

This is one of the most common contractor questions. Technically, the umbrella company is your employer. Because of this:

- Employer's National Insurance must be paid

- The Apprenticeship Levy may apply

- Other employment costs must be covered

These costs are generally funded from the contract income received by the umbrella company, which is why they reduce the salary available to you. In a permanent role your employer pays these costs separately; in umbrella employment they come out of the assignment rate.

What is the Apprenticeship Levy?

The Apprenticeship Levy is a UK payroll tax paid by employers. Umbrella companies often recover this cost through their payroll calculations. While the amount is relatively small, many contractors notice it as a separate line on their payslip.

Umbrella company margin fees explained

Umbrella companies charge an administration fee (their margin) for:

- Payroll processing

- HMRC reporting

- Employment administration

- Statutory employment rights

These fees are usually charged weekly or monthly. Crucially, the margin is the umbrella's actual profit — employer's NI and the Apprenticeship Levy are statutory costs, not the umbrella's fee. Always compare margins before selecting an umbrella provider.

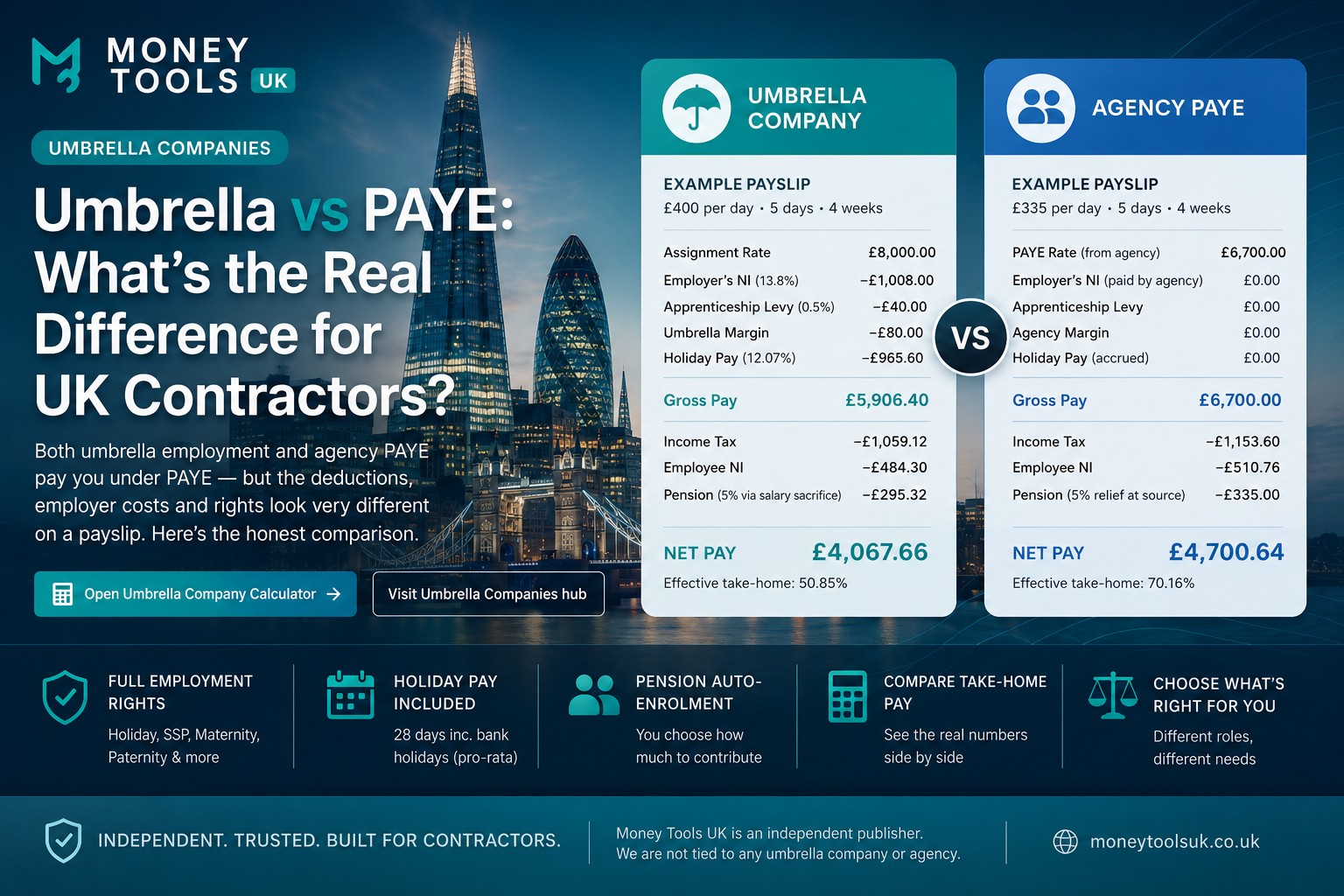

Umbrella company vs PAYE employee

Similarities

Both an umbrella worker and a standard PAYE employee pay:

- Income Tax

- National Insurance

- Student loan repayments

- Pension contributions

Differences

Umbrella workers often see:

- Employer costs shown more transparently on the payslip

- Assignment rates instead of salaries

- Additional payroll calculations

This makes umbrella payslips appear more complicated than traditional employment, even though the underlying PAYE tax treatment is the same. For a full breakdown, see our Umbrella vs PAYE Explained guide.

Umbrella company vs limited company

Umbrella company

Pros:

- Simple administration

- PAYE handled automatically

- Suitable for inside IR35 contracts

Cons:

- Lower take-home pay

- Less tax planning flexibility

Limited company

Pros:

- Greater flexibility

- Potential tax efficiencies

- Dividend planning opportunities

Cons:

- More administration

- Accountancy costs

- Additional compliance requirements

For a detailed comparison, see our How Much Tax Do UK Contractors Actually Pay? guide, or compare structures with the IR35 Comparison Calculator.

Does an umbrella company affect student loan repayments?

Yes. Student loan repayments are normally calculated through PAYE. If your earnings exceed the relevant threshold, deductions may appear automatically on your payslip. For more information, see our Plan 2 Student Loan Explained guide.

Does pension salary sacrifice reduce tax?

Potentially. Many umbrella providers offer pension salary sacrifice arrangements. This can reduce:

- Income Tax

- National Insurance

- Adjusted Net Income

For more information, see our Salary Sacrifice Explained guide.

Common mistakes contractors make

- Assuming the assignment rate is salary. It isn't — it must cover employment costs first.

- Comparing umbrella pay to outside IR35 income. The tax treatment is completely different.

- Ignoring umbrella margin fees. Margins vary between providers and directly affect your take-home pay.

- Not reviewing pension options. Salary sacrifice can significantly improve tax efficiency.

Compare your contracting options

Model umbrella PAYE against inside and outside IR35 structures with our free contractor calculators to see which gives you the best take-home pay.

Can I claim expenses through an umbrella company?

In most cases, no. Following changes to UK travel and subsistence rules, most umbrella company workers cannot claim tax relief on ordinary commuting expenses. Limited exceptions may apply depending on your circumstances and contract arrangement. Always check current HMRC guidance before relying on expense claims. Working outside IR35 through a limited company is different — see what expenses contractors can claim for the full list of allowable business costs.

Related guides

Umbrella take-home pay is one piece of the wider contractor tax picture. These guides help you understand how structures, IR35 and deductions fit together.

- Umbrella vs PAYE Explained — how umbrella and agency PAYE deductions really compare.

- Inside vs Outside IR35 Explained — the status rules that decide your structure.

- How Much Tax Do UK Contractors Actually Pay? — PAYE, umbrella and limited company compared.

- Best Salary and Dividend Split for UK Contractors — limited company tax efficiency.

- What Expenses Can Contractors Claim? — allowable business expenses that cut your Corporation Tax bill.

- Salary Sacrifice Explained — cut Income Tax and NI through pension sacrifice.

- Plan 2 Student Loan Explained — how repayments work through PAYE.

Sources & references

This guide reflects official UK government and HMRC guidance on PAYE, National Insurance, the Apprenticeship Levy, workplace pensions and student loan repayments for the 2025/26 tax year.

- HMRC — PAYE and payroll for employers

- GOV.UK — National Insurance: how it works

- HMRC — Pay Apprenticeship Levy

- GOV.UK — Workplace pensions

- GOV.UK — Repaying your student loan

Last updated

This article was last reviewed on 19 June 2026 and reflects current PAYE, National Insurance and umbrella company payroll rules for the 2025/26 UK tax year. We refresh this guide each time HMRC publishes a material change.

Reviewed by Money Tools UK Editorial Team

This guide was reviewed for accuracy against HMRC and GOV.UK guidance for the 2025/26 tax year. We regularly update our contractor and tax content when thresholds, rates or eligibility rules change.

Last reviewed: 19 June 2026

Disclaimer

Money Tools UK provides educational information only and does not provide tax, accounting or financial advice. Figures are estimates based on standard 2025/26 UK tax rules and individual circumstances may vary. Consider obtaining professional advice before making tax or contracting decisions.

Get new UK finance and property guides from Money Tools UK

Plain-English UK finance insights, tax updates and property investing guides.

Related calculators

Umbrella Company Calculator

The exact calculator this article is built around — open it and run your own numbers.

Open calculatorFrequently asked questions

Related guides

More flagship guides and tools from Money Tools UK.

Umbrella vs agency PAYE compared for 2025/26: full worked example on a £400/day contract, side-by-side payslips, deductions, holiday pay, pensions and rights.

Read guide

A plain-English UK guide to checking if HMRC owes you a tax refund: why overpayments happen, how to use your Personal Tax Account, P800 and Simple Assessment, when refunds are automatic, how to claim, and how to avoid tax refund scams.

Read guide

Why HMRC overtaxes pension withdrawals with emergency tax, how pension tax refunds work, and which form to use — P55, P53Z, P50Z or P53 — to reclaim overpaid tax for 2025/26.

Read guideDisclaimer: This content is for informational purposes only and should not be treated as financial, tax, mortgage, investment or legal advice.