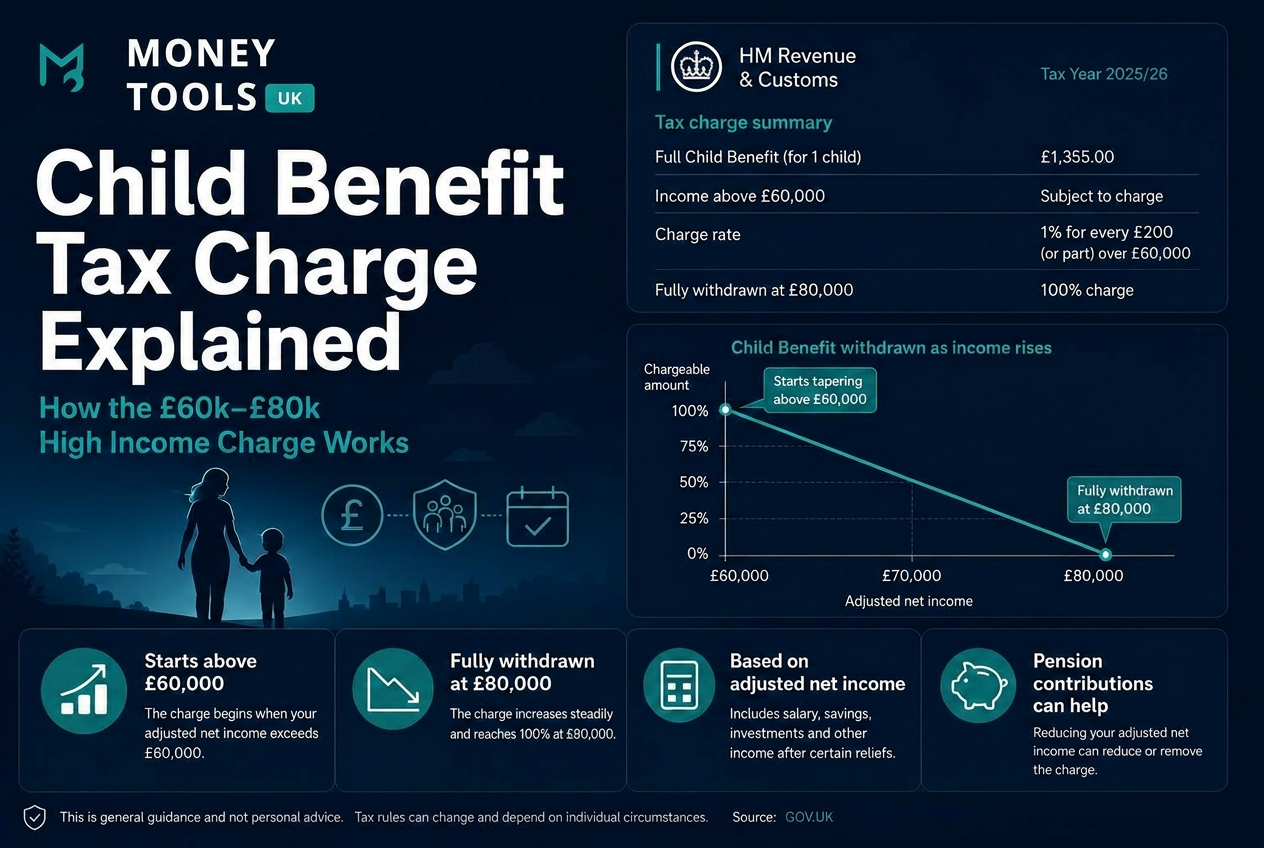

The High Income Child Benefit Charge (HICBC) catches out thousands of UK families every year — largely because it is misunderstood. Crucially, the charge is based on the income of the highest earner, not your total household income. If one partner's adjusted net income climbs above £60,000, some of your Child Benefit is gradually clawed back through a tax charge, until it is fully withdrawn at £80,000.

The good news: being affected by the charge does not always mean losing your Child Benefit for good. This guide explains, in plain English, whether you're caught, exactly how the charge is calculated for the 2025/26 tax year, and how pension contributions and salary sacrifice can reduce your adjusted net income and protect your benefit.

Updated for 2025/26

The short answer

The short answer

- It is based on individual income, not combined household income.

- Between £60,000 and £80,000, you repay 1% of your Child Benefit for every £200 of adjusted net income over £60,000.

- At £80,000 or above, the full Child Benefit amount is effectively repaid through the charge.

- Pension contributions and salary sacrifice reduce adjusted net income — and can reduce or remove the charge entirely.

What is the High Income Child Benefit Charge?

Child Benefit is a payment from the government to help with the cost of raising children. For 2025/26 it is paid at £26.05 per week for your eldest or only child and £17.25 per week for each additional child. Over a full year that's roughly £1,354.60 for one child and £897 more for each further child.

The High Income Child Benefit Charge exists to claw back Child Benefit from higher earners. Rather than stopping the payment, HMRC recovers it through an Income Tax charge on the higher-earning partner.

- Who pays it. The partner with the higher adjusted net income pays the charge — whether or not they are the person who actually receives the Child Benefit.

- Why one earner can trigger it. Because the test looks at a single individual's income, a family can be affected even when only one parent earns above the threshold.

- The household quirk. A two-earner household where each partner earns, say, £55,000 (total £110,000) keeps full Child Benefit, while a single-earner household on £80,000 loses all of it. It feels unfair — but it follows directly from the individual-income rule.

The household income paradox

One of the most controversial aspects of the High Income Child Benefit Charge is that it is based on an individual’s adjusted net income rather than total household income.

Consider these two families:

Family A

- Parent 1 income: £55,000

- Parent 2 income: £55,000

- Combined household income: £110,000

- Child Benefit retained: 100%

Neither individual earns more than £60,000, so no Child Benefit charge applies.

Family B

- Parent 1 income: £80,000

- Parent 2 income: £0

- Combined household income: £80,000

- Child Benefit retained: 0%

Because one individual earns £80,000, the High Income Child Benefit Charge fully withdraws the benefit.

Why this matters

Although Family B earns £30,000 less overall than Family A, they lose more Child Benefit because the charge is based on the income of the highest individual earner rather than total household income.

This is one of the most commonly criticised features of the Child Benefit system and catches many families by surprise.

2025/26 Child Benefit Tax Charge thresholds

The charge increases steadily across the £60,000–£80,000 band. The table below shows the percentage of your Child Benefit repaid at each level of adjusted net income:

| Adjusted Net Income | Charge |

|---|---|

| £60,000 or below | No charge |

| £65,000 | 25% of Child Benefit repaid |

| £70,000 | 50% repaid |

| £75,000 | 75% repaid |

| £80,000+ | 100% repaid |

The formula

Worked examples

These examples use the 2025/26 Child Benefit rates: £1,354.60 a year for one child, £2,251.60 for two children and £3,148.60 for three children. The charge is rounded to whole pounds, as HMRC does.

Example A — one child, income £62,000

- Child Benefit received: £1,354.60 (one child).

- Income over £60,000: £2,000 → £2,000 ÷ £200 = 10% charge.

- Amount repaid: 10% × £1,354.60 ≈ £135.

- Net benefit kept: roughly £1,220.

Example B — two children, income £70,000

- Child Benefit received: £2,251.60 (two children).

- Income over £60,000: £10,000 → 50% charge.

- Amount repaid: 50% × £2,251.60 ≈ £1,126.

- Net benefit kept: roughly £1,126.

Example C — three children, income £80,000

- Child Benefit received: £3,148.60 (three children).

- Income over £60,000: £20,000 → 100% charge.

- Amount repaid: the full £3,149.

- Net benefit kept: £0 — the entire benefit is clawed back.

Example D — income £75,000 reduced to £60,000 with pension contributions

Suppose you have two children and earn £75,000. Without action you'd face a 75% charge (£15,000 over ÷ £200), repaying around £1,689 and keeping only ~£563.

- Make a £15,000 gross pension contribution (via salary sacrifice or a personal pension), reducing adjusted net income to £60,000.

- HICBC charge: £0 — you keep the full £2,251.60.

- You also save 40% Income Tax (and potentially National Insurance via salary sacrifice) on the £15,000 — the pension contribution is far cheaper than it looks once the protected benefit and tax relief are counted.

Adjusted net income explained

The HICBC is based on your adjusted net income — not your gross salary. Adjusted net income is your total taxable income from all sources, minus certain reliefs such as pension contributions and Gift Aid donations.

Income that counts towards adjusted net income includes:

- Salary and wages.

- Bonuses and commission.

- Taxable benefits in kind (company car, medical insurance, etc.).

- Savings interest above your allowance.

- Dividends.

- Rental and other property income.

Things that reduce adjusted net income:

- Pension contributions (grossed up) — the most powerful lever for most families.

- Gift Aid donations — the gross value of charitable giving reduces adjusted net income.

- Certain other allowable deductions, such as trading losses or specific reliefs.

Money Tools UK will publish a full Adjusted Net Income Explained guide soon — until then, the section above covers the essentials you need to estimate where you stand against the £60,000 and £80,000 thresholds.

How salary sacrifice can reduce the charge

Pension salary sacrifice is one of the cleanest ways to bring your adjusted net income back below the threshold. You agree to give up part of your salary, and your employer pays it directly into your pension before Income Tax and National Insurance are applied.

- It reduces adjusted net income pound for pound. Every £1 sacrificed lowers the figure used for the HICBC test.

- It protects Child Benefit. Bringing income from £70,000 down to £60,000 removes the charge entirely — you keep 100% of your Child Benefit instead of repaying 50%.

- It saves tax and NI at the same time. You avoid 40% Income Tax and employee National Insurance on the sacrificed amount, and the money builds your pension instead.

For full worked examples of how these arrangements stack up, read our Salary Sacrifice Explained guide — it shows exactly how salary sacrifice reduces adjusted net income across different salary levels.

How bonuses can trigger the charge

A bonus can quietly push you over the £60,000 line even when your base salary sits safely below it. Because the HICBC is calculated on your annual adjusted net income, a one-off bonus is added to everything else you earn in the tax year.

- A £55,000 base salary plus a £10,000 bonus gives an adjusted net income of £65,000 — triggering a 25% Child Benefit charge.

- Even if your salary alone never crosses £60,000, bonus income can do so and create a charge you weren't expecting.

- Sacrificing all or part of a bonus into your pension can keep your adjusted net income under £60,000 and protect your Child Benefit.

For a full breakdown of how variable pay is taxed, see our guide on how bonuses are taxed in the UK.

What happens if you do not pay the charge?

The HICBC is your responsibility to report — HMRC does not automatically deduct it from your salary.

- Self Assessment. The charge is usually reported and paid through a Self Assessment tax return. If you're liable, you may need to register for Self Assessment.

- PAYE collection. In some cases HMRC can collect the charge through your tax code where this option is available.

- Penalties and interest. If the charge isn't reported correctly, HMRC may apply interest and penalties on the unpaid amount.

- Check official guidance. Always confirm your position against current HMRC and GOV.UK guidance, as collection methods can change.

Should you still claim Child Benefit?

Even if the charge will recover some or all of your Child Benefit, there are strong reasons to still claim it.

- National Insurance credits. Claiming protects NI credits for a non-working or lower-earning parent, helping them build entitlement towards the State Pension.

- Automatic NI number. A Child Benefit claim helps your child receive their National Insurance number automatically before they turn 16.

- Claim but opt out of payments. Many families choose to register the claim but tick the box to not receive payments, which avoids the charge while keeping the NI credit protection.

Claiming vs receiving payments

Common mistakes parents make

- Thinking the charge is based on household income. It's based on the highest individual earner.

- Thinking both parents need to earn over £60k. Only one partner crossing the threshold is enough.

- Forgetting bonuses when working out adjusted net income.

- Forgetting taxable benefits such as a company car or medical insurance.

- Ignoring pension contributions that could legally reduce the charge.

- Not claiming Child Benefit and losing valuable NI credits as a result.

- Assuming £80k salary always means no benefit — pension contributions can drop adjusted net income below £80,000 (or even £60,000) and restore some or all of it.

- Forgetting to update HMRC when circumstances or income change.

How to legally reduce the Child Benefit charge

- Pension contributions — reduce adjusted net income and earn tax relief.

- Salary sacrifice — cut income before tax and NI, lowering the HICBC test figure.

- Gift Aid donations — the gross value reduces adjusted net income.

- Bonus sacrifice into pension — keep variable pay out of the charge zone.

- Review taxable benefits — benefits in kind add to adjusted net income.

- Check your tax code and adjusted net income regularly to avoid surprises.

Check your real take-home pay and Child Benefit impact

Use the Money Tools UK Take-Home Pay Calculator to model your salary, pension contributions, salary sacrifice and bonus income so you can understand how your adjusted net income may affect Child Benefit.

Related guides

- £60k Salary After Tax UK — where higher-rate tax and the Child Benefit charge begin.

- £70k Salary After Tax UK — see take-home pay deep in the higher-rate band.

- £80k Salary After Tax UK — the point where Child Benefit is fully withdrawn.

- £90k Salary After Tax UK — approaching the £100k personal allowance taper.

- £100k Salary After Tax UK — understand the 60% tax trap above £100,000.

- Salary Sacrifice Explained — the most effective way to cut adjusted net income.

- How Bonuses Are Taxed in the UK — why a bonus can trigger the charge.

- Personal Allowance Taper Explained — the related trap above £100,000.

Sources & references

This guide references current HMRC and GOV.UK guidance for the 2025/26 UK tax year.

- GOV.UK — High Income Child Benefit Charge

- HMRC — Child Benefit guidance

- GOV.UK — Child Benefit rates

- GOV.UK — Self Assessment tax returns

- GOV.UK — Personal Allowances: adjusted net income

Last updated

This article was last reviewed on 12 June 2026 and reflects the High Income Child Benefit Charge thresholds and Child Benefit rates confirmed for the 2025/26 tax year. We refresh this guide each time HMRC publishes a material change.

Disclaimer

Money Tools UK provides educational content and calculators only. The figures above are estimates based on standard 2025/26 UK tax rules and assume a single PAYE employment. They do not account for benefits in kind, pension annual-allowance limits, or personal circumstances that may change your actual liability. Because benefit entitlement depends on your personal circumstances, it's worth checking GOV.UK benefit calculators rather than assuming you are not eligible. For regulated tax or financial advice, please speak to a qualified accountant or independent financial adviser.

Get new UK finance and property guides from Money Tools UK

Plain-English UK finance insights, tax updates and property investing guides.

Related calculators

UK Take-Home Pay Calculator

The exact calculator this article is built around — open it and run your own numbers.

Open calculatorFrequently asked questions

Related guides

More flagship guides and tools from Money Tools UK.

A plain-English UK guide to checking if HMRC owes you a tax refund: why overpayments happen, how to use your Personal Tax Account, P800 and Simple Assessment, when refunds are automatic, how to claim, and how to avoid tax refund scams.

Read guide

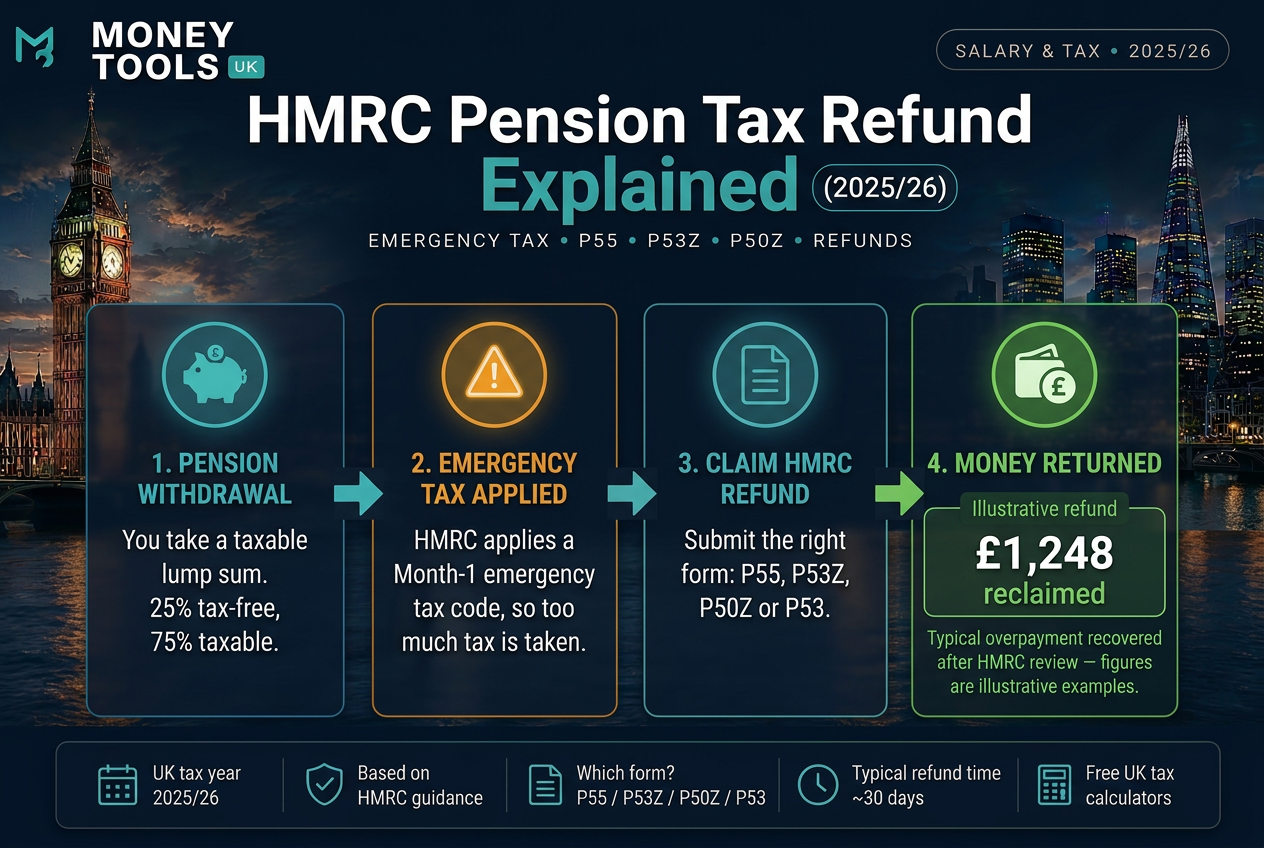

Why HMRC overtaxes pension withdrawals with emergency tax, how pension tax refunds work, and which form to use — P55, P53Z, P50Z or P53 — to reclaim overpaid tax for 2025/26.

Read guide

Learn how UK company car tax works in 2025/26, including Benefit-in-Kind tax, P11D value, CO2 emissions, electric cars, fuel benefit and salary sacrifice examples.

Read guideDisclaimer: This content is for informational purposes only and should not be treated as financial, tax, mortgage, investment or legal advice.