An umbrella company might advertise a weekly margin of £20, £25 or £30. But that small weekly fee is not the full story. For contractors, the better question is not simply "how much does the umbrella company charge?" — it is "out of my assignment rate, how much disappears before the money reaches my bank account?" This guide explains the real cost of working through an umbrella company in the 2025/26 tax year, including umbrella margins, Employer's National Insurance, the Apprenticeship Levy, holiday pay, pension deductions, PAYE tax and take-home pay. The umbrella company's margin is often the smallest deduction on your payslip.

Wondering what YOUR umbrella pay will be?

Use the Money Tools UK Umbrella Company Calculator to estimate your take-home pay based on your day rate, working days, umbrella margin, pension contributions and tax assumptions.

Quick example: £500/day through an umbrella company

The short answer

An umbrella company's visible fee is usually its margin — often around £20–£35 per week. However, a contractor's total deductions can be much larger, because the assignment rate may also fund:

- Employer's National Insurance

- the Apprenticeship Levy

- employer pension contributions where applicable

- holiday pay treatment

- the umbrella margin

- PAYE Income Tax

- Employee National Insurance

- student loan deductions where applicable

- employee pension contributions where applicable

Important: the umbrella margin is the umbrella company's actual fee. Employer's National Insurance and PAYE tax are not the umbrella company's "profit" — but they still reduce what reaches the contractor.

What is an umbrella company?

An umbrella company is an employer that sits between the contractor and the recruitment agency or end client. The agency pays the umbrella company, and the umbrella company then:

- employs the contractor

- processes payroll

- deducts taxes and National Insurance

- issues payslips

- handles employment administration

- pays the contractor their net pay

Umbrella companies are especially common for inside IR35 contracts. When an engagement is caught by the off-payroll working rules, the contractor must be taxed broadly like an employee — so paying through an umbrella under PAYE is usually the simplest compliant route, avoiding the need to run a limited company that can no longer be operated tax-efficiently for that contract. For the full mechanics, see How Umbrella Company Take-Home Pay Really Works.

What does an umbrella company charge?

It helps to separate three very different things that all reduce your pay but reach completely different places:

- The umbrella margin — this is the umbrella company's actual fee for employing and paying you.

- Statutory employment costs — costs funded from the assignment rate, such as Employer's NI and the Apprenticeship Levy. These go to HMRC, not the umbrella.

- PAYE deductions — your own Income Tax and Employee National Insurance, exactly as any employee pays.

The weekly fee is only one part of the story

The difference between umbrella margin and total deductions

A contractor might see an umbrella margin of just £25/week, yet the total difference between the assignment rate and take-home pay can run to tens of thousands of pounds a year. That does not mean the umbrella company has taken all that money as a fee. Most of the gap is tax, National Insurance, pension, holiday pay treatment and statutory employment costs.

How your assignment rate becomes take-home pay

Where your assignment rate goes

Take a realistic example: a £500/day contract billed for 220 days, giving an annual assignment value of roughly £110,000. A possible flow looks like this:

- Annual assignment value: £110,000

- Employer's NI and Apprenticeship Levy: approximately £14,000–£16,000

- Umbrella margin: approximately £500–£1,500

- Gross taxable pay after employer costs: approximately £93,000–£95,000

- PAYE Income Tax and Employee NI: approximately £28,000–£33,000

- Estimated net take-home: approximately £62,000–£68,000

Figures are illustrative only

Employer's National Insurance explained

Employer's National Insurance is a cost of employment. In ordinary employment, the employer pays it on top of your salary and you never see it. With umbrella contracting, the assignment rate is usually intended to cover employment costs before your gross taxable pay is calculated — so Employer's NI is effectively funded from the rate the agency pays the umbrella.

This is one of the main reasons umbrella take-home can feel lower than expected: contractors compare the headline assignment rate to a salary, but the assignment rate has to absorb Employer's NI first. To be clear, Employer's National Insurance is not an umbrella company fee — it is a statutory tax that goes to HMRC.

Apprenticeship Levy explained

The Apprenticeship Levy is a charge that applies to larger employers in the UK. In umbrella arrangements, it is typically accounted for within the assignment rate calculation, alongside Employer's NI. It is a small percentage but, like Employer's NI, it reduces the gross taxable pay your PAYE deductions are based on. Again, this is a statutory cost, not the umbrella's profit.

Holiday pay explained

Holiday pay is one of the most confusing parts of an umbrella payslip, and it is a common reason two "take-home" estimates differ. There are two main approaches:

- Rolled-up holiday pay — holiday pay (commonly 12.07% of gross) is paid to you on every payslip, so you receive it continuously rather than when you take leave.

- Accrued holiday pay — the umbrella retains your holiday pay and pays it out when you actually take time off.

Either way, holiday pay is your money — but the treatment changes how much hits your account each week and whether any balance could be retained or, in some cases, forfeited if unclaimed.

Always check your holiday pay treatment

Pension deductions

Umbrella contractors are usually auto-enrolled into a workplace pension. Depending on your arrangement, you may see:

- employee pension contributions deducted from your pay

- employer pension contributions where applicable

- salary sacrifice pension arrangements, where contributions are made before tax and NI

Pension contributions reduce your immediate cash take-home, but they can significantly improve long-term tax efficiency — particularly via salary sacrifice, which can reduce both Income Tax and National Insurance. See Salary Sacrifice Explained and Adjusted Net Income Explained for how pensions interact with higher-rate tax and the £100,000 allowance taper.

PAYE Income Tax and Employee National Insurance

Once employer costs and the umbrella margin have been dealt with, the contractor is left with gross taxable pay. PAYE deductions then usually include:

- Income Tax (20%, 40% and 45% bands)

- Employee National Insurance

- student loan repayments where applicable

- employee pension contributions where applicable

This is broadly similar to being a normal employee — but the starting point is different. Your gross taxable pay is not your assignment rate; it is what remains after the assignment rate has absorbed Employer's NI, the Apprenticeship Levy and the margin.

Example: £500/day through an umbrella company

Worked example — £500/day

Assumptions

- £500/day, 220 billed days = £110,000 assignment value

- no student loan, standard tax code

- typical umbrella margin, no unusual pension arrangement

Illustrative outcome

- Assignment value: £110,000

- Employer costs and umbrella margin: approximately £15,000–£17,000

- Gross taxable pay: approximately £93,000–£95,000

- PAYE Income Tax and Employee NI: approximately £28,000–£33,000

- Estimated annual take-home: approximately £62,000–£68,000

- Estimated monthly take-home: approximately £5,150–£5,650

This is not a quote. Always request a full Key Information Document and an umbrella illustration before accepting a role.

Example: £400/day through an umbrella company

Worked example — £400/day

Assumptions

- £400/day, 220 billed days = £88,000 assignment value

Illustrative outcome

- Assignment value: £88,000

- Employer costs and umbrella margin: approximately £11,000–£13,000

- Gross taxable pay: approximately £75,000–£77,000

- PAYE Income Tax and Employee NI: approximately £20,000–£25,000

- Estimated annual take-home: approximately £52,000–£57,000

- Estimated monthly take-home: approximately £4,300–£4,750

See exactly what you could take home

Use the Money Tools UK Umbrella Company Calculator to test your own day rate, working days, pension contributions, student loan plan, umbrella margin and holiday pay assumptions.

Umbrella company payslip explained

An umbrella payslip can look confusing because some deductions happen before gross taxable salary is calculated and some happen after. Common lines include:

- Assignment rate — the rate the agency pays the umbrella

- Gross pay — pay after employer costs and margin

- Taxable pay — the figure PAYE is applied to

- Umbrella margin — the umbrella's fee

- Employer's NI — statutory employment cost

- Apprenticeship Levy — statutory employment cost

- Holiday pay — paid or accrued

- Pension — employee and/or employer contributions

- PAYE tax — your Income Tax

- Employee NI — your National Insurance

- Net pay — what reaches your bank account

Why umbrella take-home feels lower than expected

Contractors often compare their assignment rate to a normal salary — but the assignment rate may include employment costs the rate has to fund first. The most common surprises are:

- "Why am I paying Employer's NI?"

- "Why is my gross pay lower than my day rate?"

- "Why is my holiday pay separate?"

- "Why is the umbrella margin different from total deductions?"

- "Why is take-home lower than online estimates?"

Umbrella company cost comparison table

| Item | Who receives it? | Is it an umbrella fee? | Does it reduce take-home? |

|---|---|---|---|

| Umbrella margin | Umbrella company | Yes | Yes |

| Employer's NI | HMRC | No | Yes |

| Apprenticeship Levy | HMRC | No | Yes |

| PAYE Income Tax | HMRC | No | Yes |

| Employee NI | HMRC | No | Yes |

| Pension contribution | Pension provider | No | Yes, but builds pension value |

| Holiday pay | Contractor (paid or accrued) | No | Depends on treatment |

What is a fair umbrella margin?

A fair umbrella margin is often around £20–£35 per week, though it depends on the provider and the service offered. Crucially, do not choose purely on the lowest fee. A slightly higher margin from a compliant, well-run provider is far better than a cheap, opaque one. Consider:

- compliance and reputation

- clarity of payslips

- quality of customer support

- payment speed and reliability

- pension options

- holiday pay transparency

- whether the umbrella is FCSA accredited or otherwise demonstrably reputable

Red flags to watch for

Some "umbrella" arrangements are actually tax-avoidance schemes that can leave the contractor — not the promoter — with a large tax bill years later. Treat the following as warning signs:

- unusually high take-home promises

- claims of 80–90% retention through an umbrella

- loan schemes or "advances"

- offshore structures or trusts

- unclear or incomplete payslips

- no Key Information Document

- pressure to sign quickly

- unclear holiday pay treatment

- hidden or unexplained fees

- no written contract of employment

- refusal to explain Employer's NI

- vague pension treatment

If it looks too good to be true, it is

Umbrella vs agency PAYE

Both umbrella and agency PAYE involve being paid under PAYE, but the structure differs. With agency PAYE, the agency employs you directly and absorbs employer costs from a lower headline rate. With umbrella, a third-party employer runs your payroll and the assignment rate funds those costs. Compare them on:

- who employs the worker

- how payroll is handled

- holiday pay treatment

- benefits and continuity of employment

- deductions and simplicity

- net take-home on a like-for-like rate

For a full breakdown, see Umbrella vs PAYE.

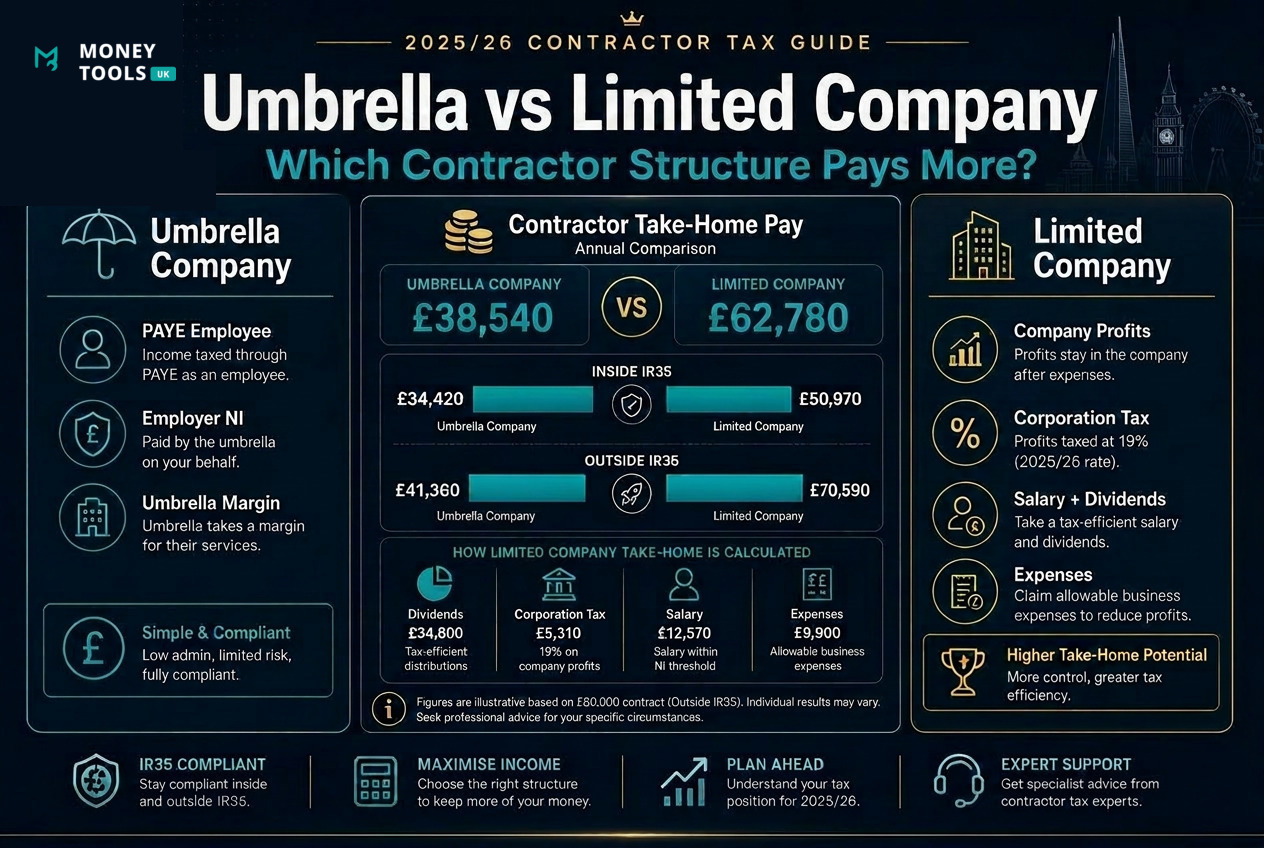

Umbrella vs limited company

Umbrella is usually simpler and is the common route for inside IR35 contracts. A limited company can be more tax-efficient when a contract is genuinely outside IR35, thanks to the salary/dividend split, allowable expenses and pension planning — but it carries more admin and risk. Compare them on:

- admin burden

- tax flexibility

- expenses

- pension planning

- risk and responsibility

- IR35 status

- take-home potential

Read next: Umbrella Company vs Limited Company, Is a £500/Day Contract Worth It After Tax? and What Expenses Can Contractors Claim?

How to reduce umbrella costs legally

You cannot simply avoid PAYE tax or National Insurance — and any scheme that claims you can is a red flag. But you can improve your outcome by:

- checking and comparing the umbrella margin

- understanding your holiday pay treatment

- using pension contributions sensibly (often via salary sacrifice)

- avoiding non-compliant schemes

- ensuring you are on the correct tax code

- checking your student loan plan is set correctly

- reducing gaps between contracts where possible

- comparing compliant umbrella illustrations side by side

Estimate your umbrella take-home pay

Use the Money Tools UK Umbrella Company Calculator to estimate how your day rate, working days, pension contributions, student loan plan and umbrella margin affect your take-home pay.

Related guides

- How Umbrella Company Take-Home Pay Really Works — a full walkthrough of umbrella deductions and net pay.

- Is a £500/Day Contract Worth It After Tax? — umbrella, inside and outside IR35 compared on the same rate.

- Umbrella Company vs Limited Company — which structure leaves you better off.

- Umbrella vs PAYE — how the two PAYE routes really differ.

- Inside IR35 vs Outside IR35 — status and its impact on take-home pay.

- Why Is Inside IR35 Take-Home Pay So Low? — the mechanics behind the deductions.

- What Expenses Can Contractors Claim? — allowable expenses for limited company contractors.

- Best Salary and Dividend Split for UK Contractors — for outside IR35 limited company contractors.

- Salary Sacrifice Explained — cut tax and NI while building your pension.

- Adjusted Net Income Explained — how pensions interact with the £100k taper.

Related calculators

Sources & references

This guide reflects official UK government and HMRC guidance on umbrella companies, PAYE, National Insurance, the Apprenticeship Levy, holiday pay and workplace pensions for the 2025/26 tax year.

- GOV.UK — Working through an umbrella company

- GOV.UK — Key Information Documents for agency workers

- GOV.UK — National Insurance rates and categories

- GOV.UK — Income Tax rates and Personal Allowances

- GOV.UK — Apprenticeship Levy

- GOV.UK — Holiday entitlement

- GOV.UK — Workplace pensions

- GOV.UK — Understanding your payslip

- GOV.UK — Tax avoidance schemes aimed at contractors and agency workers

- HMRC — Off-payroll working (IR35) guidance

Last updated

This article was last reviewed on 25 June 2026 and reflects UK umbrella company, PAYE, National Insurance, Apprenticeship Levy, holiday pay, pension and contractor tax guidance for the 2025/26 tax year.

Disclaimer

Money Tools UK provides educational information and calculators only. This article is not tax, accounting, legal, employment or financial advice. Umbrella company take-home pay depends on day rate, assignment rate, umbrella margin, Employer's NI, holiday pay treatment, pension contributions, student loan deductions, tax code, working days and individual circumstances. Always request a full umbrella illustration and speak to a qualified adviser before making contractor decisions.

Get new UK finance and property guides from Money Tools UK

Plain-English UK finance insights, tax updates and property investing guides.

Related calculators

Umbrella Company Calculator

The exact calculator this article is built around — open it and run your own numbers.

Open calculatorFrequently asked questions

Related guides

Is a £500/Day Contract Worth It After Tax? (2025/26)See how much a £500/day contract could be worth after tax in 2025/26. Compare umbrella company, inside IR35, outside IR35 and limited company take-home pay.

Is a £500/Day Contract Worth It After Tax? (2025/26)See how much a £500/day contract could be worth after tax in 2025/26. Compare umbrella company, inside IR35, outside IR35 and limited company take-home pay. What Expenses Can Contractors Claim in 2025/26?Learn which business expenses UK contractors can claim in 2025/26, including travel, home office, equipment, subscriptions, accountancy fees, training, pensions and more.

What Expenses Can Contractors Claim in 2025/26?Learn which business expenses UK contractors can claim in 2025/26, including travel, home office, equipment, subscriptions, accountancy fees, training, pensions and more. Umbrella Company vs Limited Company (2025/26): Which Pays More?Compare umbrella company vs limited company take-home pay in 2025/26. Learn how tax, IR35, dividends, expenses, admin, risk and calculator examples affect which structure pays more.

Umbrella Company vs Limited Company (2025/26): Which Pays More?Compare umbrella company vs limited company take-home pay in 2025/26. Learn how tax, IR35, dividends, expenses, admin, risk and calculator examples affect which structure pays more.Disclaimer: This content is for informational purposes only and should not be treated as financial, tax, mortgage, investment or legal advice.