Most tax-efficient

Outside IR35 Ltd

Simplest

Umbrella

Decider

IR35 status

The answer is not always simple. Which structure pays more depends on your IR35 status, day rate, expenses, pension contributions, admin tolerance and risk appetite.

Choosing between an umbrella company and a limited company can make a major difference to a contractor's take-home pay, tax flexibility, administration and risk. But the answer is not always simple.

An umbrella company is usually simpler and often used for inside IR35 contracts, but take-home pay can feel lower because the assignment rate may fund employer-side costs before PAYE salary is calculated.

A limited company can be more tax-efficient for genuinely outside IR35 contracts because profits can be taken through a mix of salary and dividends, with legitimate business expenses reducing taxable profit. But it also brings more admin, accountancy costs, legal responsibility and IR35 risk.

This guide compares umbrella companies and limited companies for the 2025/26 tax year, explains which structure usually pays more, shows practical examples and helps you understand when each option may make sense.

The short answer

- Limited company (outside IR35)

- Usually has the potential to pay more, because the contractor may use a tax-efficient mix of salary, dividends and allowable business expenses.

- Umbrella company

- Often simpler and commonly used for inside IR35 contracts, but take-home pay may be lower because the assignment rate is processed through PAYE and may fund employer-side costs before taxable salary is calculated.

- Inside IR35 work

- The take-home pay difference between umbrella and limited company is usually much smaller, and many clients or agencies prefer umbrella arrangements.

Umbrella company vs limited company at a glance

| Feature | Umbrella company | Limited company |

|---|---|---|

| Employment status | Employee of the umbrella | Director/shareholder of your own company |

| Tax treatment | PAYE Income Tax and NI | Corporation Tax, salary and dividends |

| Best suited for | Inside IR35, short contracts | Outside IR35, ongoing business |

| IR35 position | Status handled via PAYE | Status risk sits with the engagement |

| Admin burden | Low | Higher |

| Expenses | Very limited | Allowable business expenses |

| Pension flexibility | Salary sacrifice possible | Employer contributions flexible |

| Take-home potential | Lower | Higher (outside IR35) |

| Risk level | Lower | Higher |

| Typical setup time | Same day / very fast | Days to weeks |

| Who handles payroll | Umbrella company | You / your accountant |

| Who deals with HMRC | Umbrella company | You / your accountant |

What is an umbrella company?

An umbrella company employs the contractor and processes pay through PAYE. The agency or client pays the umbrella company. The umbrella company then calculates employment costs, the umbrella margin, taxable gross pay and employee deductions before paying the contractor.

For a full breakdown of every deduction on an umbrella payslip, see our guide to umbrella company take-home pay.

What is a limited company?

A limited company contractor works through their own company, often called a Personal Service Company (PSC). The company invoices the client or agency, receives income, pays business costs and Corporation Tax, and then the director/shareholder can take income through salary, dividends or a mix of both.

Limited companies are separate legal entities and involve Companies House filings, annual accounts, Corporation Tax returns and director responsibilities. This added structure brings flexibility, but also more ongoing obligations.

Which pays more?

In general:

- Outside IR35 limited company contracts often have the highest take-home potential.

- Inside IR35 contracts usually reduce the advantage of a limited company.

- Umbrella companies are simpler but often produce lower net pay.

The correct answer depends on rate, IR35 status, expenses, pension contributions, accountancy fees, risk appetite and admin tolerance.

Most tax-efficient

Outside IR35 limited company

Simplest

Umbrella company

Best for inside IR35 simplicity

Umbrella company

Best for outside IR35 flexibility

Limited company

Why IR35 changes the answer

IR35 / off-payroll working rules are central to this comparison. If the contract is outside IR35, a limited company can usually operate as a genuine business and use normal company tax planning.

If the contract is inside IR35, the worker is treated more like an employee for tax purposes, meaning PAYE Income Tax and National Insurance are broadly brought into the calculation.

What GOV.UK says

To understand the status difference in detail, read Inside IR35 vs Outside IR35.

Inside IR35 comparison

Inside IR35 contracts often reduce the tax advantage of limited companies. Many agencies and clients prefer contractors to use umbrella companies for inside IR35 assignments because payroll is simpler.

Umbrella (inside IR35)

- PAYE handled by the umbrella

- Simple administration

- Visible employer-side costs

- Umbrella margin applies

- Less control

Limited company (inside IR35)

- May still be possible in some cases

- Deemed employment payment rules may apply

- Less tax flexibility

- Company admin still exists

- May not be worth it unless there are specific reasons

For why inside IR35 net pay feels so low, see Why Is Inside IR35 Take-Home Pay So Low? and How Umbrella Company Take-Home Pay Really Works.

Outside IR35 comparison

Outside IR35 is where limited companies usually become more attractive. A genuine outside IR35 contractor may:

- Invoice through a company

- Deduct allowable business expenses

- Pay Corporation Tax on profits

- Take a small salary

- Extract remaining profits as dividends

- Retain profits in the company

- Make employer pension contributions

This can improve take-home pay and flexibility compared with umbrella PAYE — but only where the contract and working practices genuinely support outside IR35 status.

How umbrella company pay works

An umbrella payslip generally works through this sequence:

- Assignment rate

- Employer's National Insurance

- Apprenticeship Levy

- Umbrella margin

- Taxable gross pay

- PAYE Income Tax

- Employee National Insurance

- Pension (if applicable)

- Student loan (if applicable)

- Net take-home pay

Umbrella Route

Limited Company Route

For the full breakdown, see How Umbrella Company Take-Home Pay Really Works.

How limited company pay works

- The client/agency pays the company invoice.

- The company pays business costs.

- The company pays Corporation Tax on profits.

- The director may take income through salary, dividends, pension contributions and reimbursed expenses where allowable.

This creates more flexibility, but also more responsibility — accounts, filings and director duties all sit with you.

Compare your contracting structures

Use our free Contractor Tax Calculator to model salary, dividends and Corporation Tax for an outside IR35 limited company in the 2025/26 tax year.

Salary and dividends explained

Limited company contractors often use a salary and dividend mix.

Salary

- A deductible company expense

- Subject to PAYE / National Insurance depending on the level

- May help maintain your National Insurance record

Dividends

- Paid from post-Corporation Tax profits

- Not subject to National Insurance

- Taxed under dividend tax rules above the dividend allowance

For the optimal split, see Best Salary and Dividend Split for UK Contractors.

Corporation Tax explained

A limited company pays Corporation Tax on its taxable profits. For the 2025/26 tax year:

- 19% small profits rate for profits up to £50,000

- 25% main rate for profits above £250,000

- Marginal relief may apply between those levels

Thresholds can be affected by associated companies and accounting periods, so the effective rate depends on your specific circumstances.

Dividend tax explained

Dividends are paid from company profits after Corporation Tax. For the 2025/26 tax year:

- A £500 dividend allowance applies

- Above the allowance, dividends are taxed at 8.75% (basic rate), 33.75% (higher rate) and 39.35% (additional rate)

- Dividends are not subject to National Insurance

- Dividend income still counts towards your total taxable income

Expenses and admin

Umbrella

- Limited expense flexibility

- Most ordinary commuting expenses are usually not claimable

- Payroll handled for you

Limited company

- May claim allowable business expenses

- Accountancy fees

- Software

- Insurance

- Equipment

- Professional subscriptions

- Some travel costs depending on the rules

- More record keeping required

Only claim genuine expenses

Risk and compliance

Umbrella company risks

- Non-compliant umbrella schemes

- Unrealistic take-home claims

- Unclear holiday pay

- Confusing payslips

- Hidden margins

Limited company risks

- IR35 status risk

- Companies House obligations

- Corporation Tax returns

- VAT if registered

- Payroll responsibilities

- Director responsibilities

- Accountancy costs

- Late filing penalties

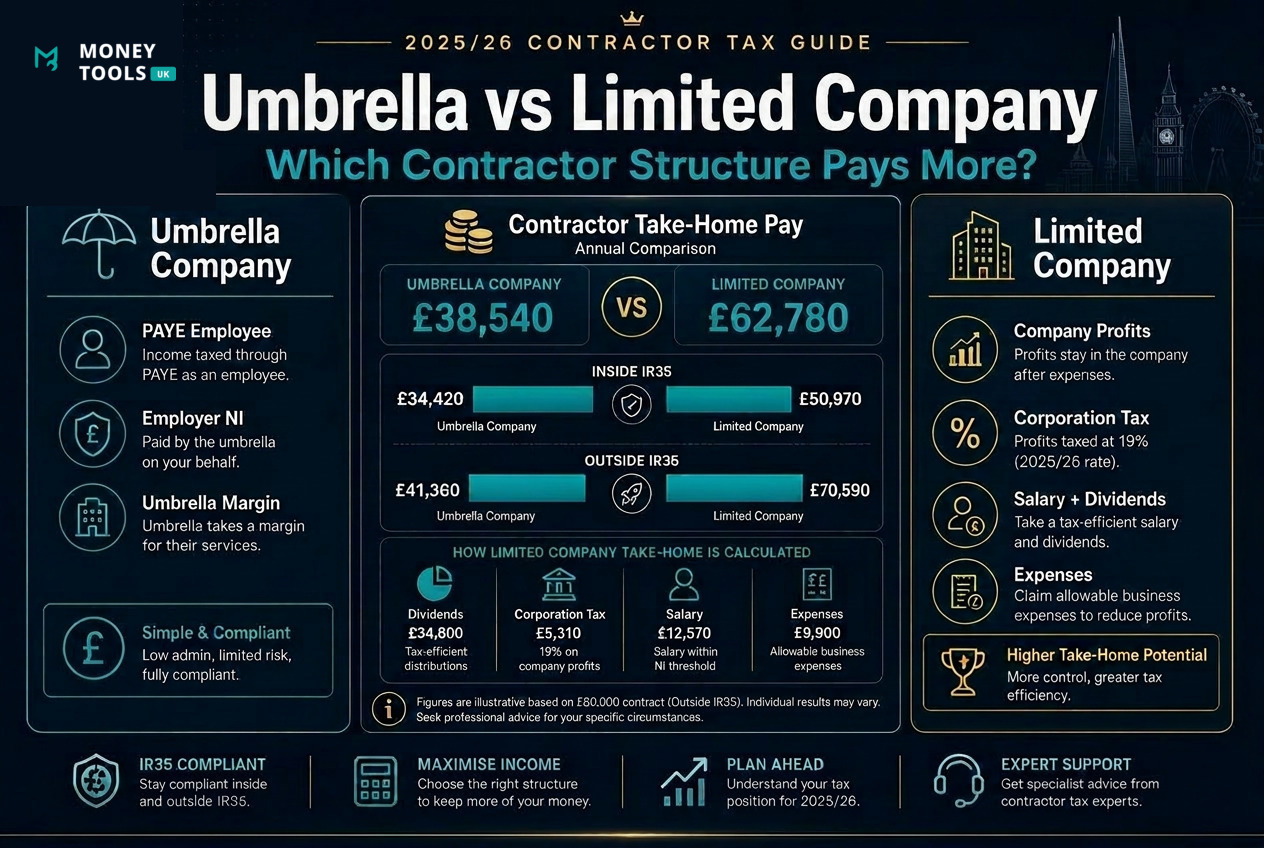

Worked examples

These illustrative examples show how structure and IR35 status change the outcome. They are not exact advice — figures depend on tax code, pension contributions, student loans, expenses, working days, VAT, IR35 status and personal circumstances.

Example A — £500/day inside IR35 through umbrella

- Assignment income: ~£130,000 (≈260 days)

- Employer costs: employer's NI + Apprenticeship Levy deducted first

- Umbrella margin: typically £15–£30 per week

- PAYE deductions: Income Tax + employee NI on taxable salary

- Estimated take-home: roughly 55–60% of the assignment rate

Example B — £500/day outside IR35 through a limited company

- Company income: ~£130,000 invoiced

- Expenses/accountancy: allowable costs reduce taxable profit

- Corporation Tax: charged on profits (19% / marginal relief band)

- Extraction: small salary plus dividends

- Estimated take-home: typically higher than the umbrella route

Illustrative Take-Home Pay Comparison

The figures below are illustrative examples only and are intended to demonstrate why outside IR35 limited company contractors often achieve higher take-home pay than umbrella workers. Actual results depend on expenses, pension contributions, tax code, working days, student loans and personal circumstances.

| Structure | Annual Contract Income | Estimated Take-Home Pay |

|---|---|---|

| Umbrella Company (Inside IR35) | £130,000 | Approximately £72,000 |

| Limited Company (Inside IR35) | £130,000 | Approximately £70,000–£75,000 |

| Limited Company (Outside IR35) | £130,000 | Approximately £85,000–£95,000Highest Take-Home Potential |

Key takeaway

Many contractors focus on the difference between an umbrella company and a limited company. In reality, IR35 status usually has a much bigger impact on take-home pay.

A limited company operating outside IR35 often provides significantly greater flexibility through salary, dividends, pension contributions and allowable business expenses.

However, once a contract falls inside IR35, much of that advantage is reduced because the income is broadly taxed in a similar way to employment income. This is why an inside IR35 limited company often produces a take-home figure that is much closer to an umbrella company than many contractors expect.

At higher rates, limited company flexibility becomes more valuable. With larger profits, the salary/dividend split, pension contributions and the ability to retain profits in the company can materially improve overall tax efficiency compared with PAYE.

Example C — Inside IR35: limited company vs umbrella

When a contract is inside IR35, the limited company advantage shrinks significantly. Deemed employment rules pull income into PAYE-style taxation, so net pay lands close to the umbrella outcome — but with extra company admin. For most inside IR35 work, umbrella is simpler for a similar result.

Illustrative only

Pros and cons

Umbrella company pros

- Simple

- PAYE handled for you

- Suitable for inside IR35

- Less admin

- No company accounts

- No Corporation Tax filing

Umbrella company cons

- Often lower take-home

- Umbrella margin

- Less flexibility

- Employer costs may reduce salary available

- Limited expense options

Limited company pros

- Higher take-home potential outside IR35

- Business expense flexibility

- Salary/dividend planning

- Pension planning

- Professional image

- Retain profits in the company

Limited company cons

- Admin

- Accountancy fees

- IR35 risk

- Companies House duties

- Corporation Tax and filings

- Less useful for many inside IR35 contracts

Which structure should you choose?

Choose umbrella if

- The contract is inside IR35

- You want simplicity

- The assignment is short

- You do not want company admin

- The agency/client requires umbrella payroll

Choose a limited company if

- The contract is genuinely outside IR35

- You expect multiple contracts or clients

- You are comfortable with admin

- You want tax planning flexibility

- You have allowable business expenses

- You want to build a contractor business

Compare umbrella and limited company take-home pay

Use Money Tools UK contractor calculators to compare umbrella PAYE, inside IR35 and outside IR35 limited company take-home pay before accepting a contract.

Related guides

These guides explain how contractor structures, IR35 and deductions fit together so you can choose the right route for your next contract.

- How Umbrella Company Take-Home Pay Really Works — every deduction on an umbrella payslip.

- Umbrella vs PAYE — how umbrella and agency PAYE deductions compare.

- Inside IR35 vs Outside IR35 — the status rules that decide your structure.

- Why Is Inside IR35 Take-Home Pay So Low? — where inside IR35 income goes.

- How Much Tax Do UK Contractors Actually Pay? — PAYE, umbrella and limited compared.

- Best Salary and Dividend Split for UK Contractors — limited company tax efficiency.

- Salary Sacrifice Explained — cut Income Tax and NI through pension sacrifice.

Sources & references

This guide reflects official UK government and HMRC guidance on off-payroll working (IR35), umbrella companies, Corporation Tax, dividend tax, National Insurance, PAYE and running a limited company for the 2025/26 tax year.

- GOV.UK — Understanding off-payroll working (IR35)

- GOV.UK — Working through an umbrella company

- GOV.UK — Corporation Tax rates

- GOV.UK — Tax on dividends

- GOV.UK — National Insurance rates and categories

- GOV.UK — PAYE and payroll for employers

- GOV.UK — Running a limited company

- GOV.UK — Self Assessment tax returns

Last updated

This article was last reviewed on 20 June 2026 and reflects UK contractor tax, IR35, umbrella company, Corporation Tax and dividend tax rules for the 2025/26 tax year. We refresh this guide each time HMRC publishes a material change.

Reviewed by Money Tools UK Editorial Team

This guide was reviewed for accuracy against HMRC and GOV.UK guidance for the 2025/26 tax year. We regularly update our contractor and tax content when thresholds, rates or eligibility rules change.

Last reviewed: 20 June 2026

Disclaimer

Money Tools UK provides educational information only and does not provide tax, accounting or financial advice. Figures are estimates based on standard 2025/26 UK tax rules and individual circumstances may vary. Consider obtaining professional advice before making tax or contracting decisions.

Get new UK finance and property guides from Money Tools UK

Plain-English UK finance insights, tax updates and property investing guides.

Related calculators

Contractor Tax Calculator

The exact calculator this article is built around — open it and run your own numbers.

Open calculatorFrequently asked questions

Related guides

More flagship guides and tools from Money Tools UK.

Can you still use a limited company inside IR35? Learn what happens to PAYE, dividends, Corporation Tax, expenses, umbrella companies and mixed inside/outside IR35 contracts.

Read guide

See how much an umbrella company really costs in 2025/26, including umbrella margin, Employer's NI, Apprenticeship Levy, holiday pay, pension deductions and contractor take-home pay.

Read guide

See how much a £500/day contract could be worth after tax in 2025/26. Compare umbrella company, inside IR35, outside IR35 and limited company take-home pay.

Read guideDisclaimer: This content is for informational purposes only and should not be treated as financial, tax, mortgage, investment or legal advice.