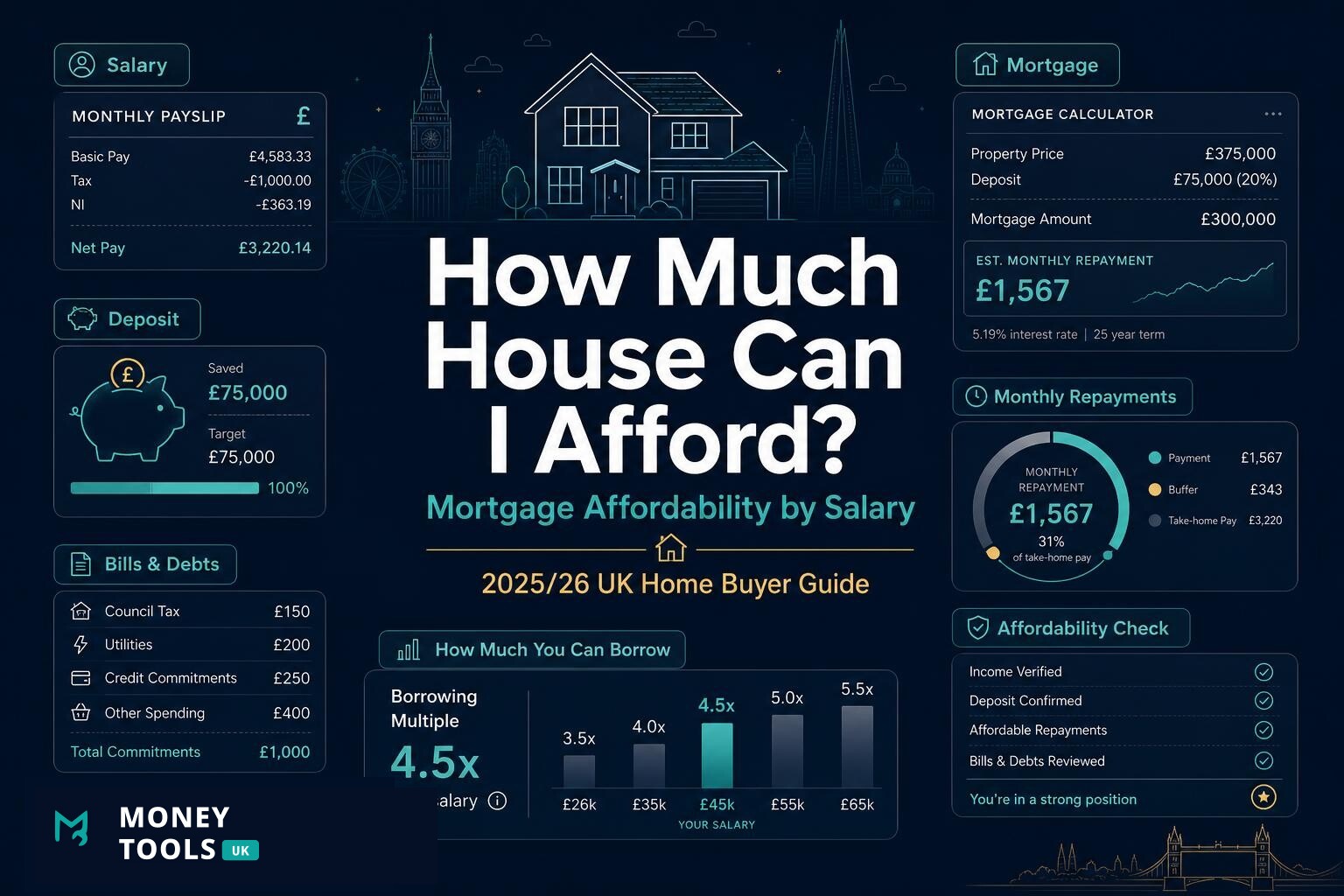

Buying a home is not just about asking how much a bank might lend you. The better question is: how much house can I afford on my salary without stretching myself too far?

In the UK, lenders often use income multiples as a starting point, but final affordability depends on much more than salary. Your deposit, debts, credit profile, monthly bills, household spending, interest rate, mortgage term, dependants and employment type can all affect how much you can borrow.

This guide explains how mortgage affordability works in 2025/26, how much house different salaries might afford, what lenders look at, how deposit size changes your budget and how to estimate a realistic property price before applying for a mortgage.

The short answer

A rough mortgage affordability estimate

Estimated mortgage borrowing = annual income × 4 to 4.5

Estimated property budget = mortgage borrowing + deposit

For example, a £40,000 salary might support rough borrowing of £160,000 to £180,000 before deposit, subject to affordability checks. With a £25,000 deposit, that could suggest a property budget of around £185,000 to £205,000.

Important

How lenders estimate affordability

Lenders do not only look at salary. A mortgage offer is the result of a detailed affordability assessment that usually considers:

- gross annual income

- stable employment

- bonuses and overtime

- self-employed income

- deposit size

- credit history

- monthly debts

- childcare costs

- household bills

- dependants

- mortgage term

- interest rate stress testing

- loan-to-income limits

- loan-to-value ratio

Because of this, two people earning the same salary may be offered very different mortgage amounts depending on their deposit, debts, spending and overall risk profile.

Salary multiples explained

Many UK borrowers use income multiples as a quick estimate of how much they might be able to borrow. Common rough estimates are:

- Cautious estimate: 4× income

- Typical estimate: 4.5× income

- Stronger-case estimate: 5× income or more for some applicants

However, you should not treat 5× as guaranteed. Some lenders may consider higher multiples for stronger applicants, but this depends on lender rules, income level, deposit, credit profile and affordability. Most buyers are best planning around the cautious to typical range of 4 to 4.5 times income.

Deposit and property price explained

It helps to separate three different numbers:

- Mortgage borrowing — the loan from the lender

- Deposit — your own cash contribution

- Property price — the total you can spend on a home

Property budget formula

If you can borrow £180,000 and have a £20,000 deposit, your potential purchase budget is £200,000 before buying costs such as Stamp Duty and legal fees.

Your deposit also determines your loan-to-value (LTV) — the size of the loan compared with the property price:

- 95% mortgage = 5% deposit

- 90% mortgage = 10% deposit

- 85% mortgage = 15% deposit

- 75% mortgage = 25% deposit

A bigger deposit may improve your mortgage choice, reduce your interest rate and increase your overall buying power.

How much house can I afford by salary?

The table below shows rough mortgage borrowing at 4× and 4.5× income, plus example property budgets once a deposit is added.

| Salary | Mortgage at 4× | Mortgage at 4.5× | Budget (£20k deposit) | Budget (£40k deposit) |

|---|---|---|---|---|

| £20,000 | £80,000 | £90,000 | £100,000–£110,000 | £120,000–£130,000 |

| £25,000 | £100,000 | £112,500 | £120,000–£132,500 | £140,000–£152,500 |

| £30,000 | £120,000 | £135,000 | £140,000–£155,000 | £160,000–£175,000 |

| £35,000 | £140,000 | £157,500 | £160,000–£177,500 | £180,000–£197,500 |

| £40,000 | £160,000 | £180,000 | £180,000–£200,000 | £200,000–£220,000 |

| £50,000 | £200,000 | £225,000 | £220,000–£245,000 | £240,000–£265,000 |

| £60,000 | £240,000 | £270,000 | £260,000–£290,000 | £280,000–£310,000 |

| £70,000 | £280,000 | £315,000 | £300,000–£335,000 | £320,000–£355,000 |

| £80,000 | £320,000 | £360,000 | £340,000–£380,000 | £360,000–£400,000 |

| £100,000 | £400,000 | £450,000 | £420,000–£470,000 | £440,000–£490,000 |

These are rough affordability examples only and do not include individual lender rules, debt, credit score, dependants, monthly spending, mortgage term or interest rate.

Estimate your own borrowing

Run your salary, deposit, monthly costs and mortgage assumptions through the Money Tools UK Mortgage Affordability Calculator for a personalised estimate.

Monthly repayments matter more than headline borrowing

Being offered a large mortgage does not automatically mean it is sensible to borrow the maximum. What matters most is whether the monthly payment fits comfortably alongside the rest of your spending, including:

- monthly mortgage payments

- council tax

- energy bills

- buildings insurance

- contents insurance

- service charges

- ground rent where relevant

- maintenance

- commuting costs

- emergency savings

- childcare

- food and household spending

Don't judge affordability by the offer alone

£20k salary example

- Single applicant

- £20,000 gross salary

- 4× to 4.5× rough borrowing range

- £10,000 deposit

- No major debts

Estimated borrowing: £80,000 to £90,000. Estimated property budget: £90,000 to £100,000.

This may be challenging in many parts of the UK, but possible in lower-cost areas, through shared ownership, in joint purchase situations or with a larger deposit. See your take-home first with our £20k Salary After Tax UK guide.

£30k salary example

- £30,000 gross salary

- £15,000 deposit

- No major debts

Estimated borrowing: £120,000 to £135,000. Estimated property budget: £135,000 to £150,000.

This may work in some lower-cost areas but can be tight where house prices are higher. Check your monthly take-home with our £30k Salary After Tax UK guide.

£40k salary example

- £40,000 gross salary

- £25,000 deposit

Estimated borrowing: £160,000 to £180,000. Estimated property budget: £185,000 to £205,000. See the full take-home breakdown in our £40k Salary After Tax UK guide.

£50k salary example

- £50,000 gross salary

- £30,000 deposit

Estimated borrowing: £200,000 to £225,000. Estimated property budget: £230,000 to £255,000.

At this salary, lenders may still examine credit commitments, childcare, car finance, student loans and other spending carefully. Review your net pay in our £50k Salary After Tax UK guide.

£60k salary example

- £60,000 gross salary

- £40,000 deposit

Estimated borrowing: £240,000 to £270,000. Estimated property budget: £280,000 to £310,000.

If the buyer has children and claims Child Benefit, they should also understand adjusted net income and the High Income Child Benefit Charge, which begins above £60,000. See our £60k Salary After Tax UK, Adjusted Net Income Explained and Child Benefit Tax Charge Explained guides.

Joint income examples

Joint applications combine income, which can increase borrowing power significantly — but they also combine debts, dependants and affordability checks. Both applicants' credit histories and commitments matter.

| Combined income | Borrowing at 4× | Borrowing at 4.5× |

|---|---|---|

| £30k + £30k = £60,000 | £240,000 | £270,000 |

| £40k + £30k = £70,000 | £280,000 | £315,000 |

| £50k + £40k = £90,000 | £360,000 | £405,000 |

Joint income can lift your potential budget considerably, but lenders still stress-test the combined affordability, so existing loans or credit commitments on either side can reduce the final offer.

What lenders check

When assessing your application, lenders may check:

- payslips

- bank statements

- employment contract

- bonuses or overtime history

- tax returns if self-employed

- credit report

- existing loans

- credit cards

- car finance

- childcare costs

- dependants

- overdraft use

- gambling transactions

- deposit source

- regular subscriptions

Clean bank statements and stable income can help your affordability case, while frequent overdraft use or unexplained large transactions may count against you.

How debts reduce affordability

Debts can reduce mortgage borrowing even when your salary is strong, because lenders focus on your disposable income, not just gross pay. Common commitments that lower affordability include:

- car finance

- personal loans

- credit card balances

- childcare costs

- student loans

- buy now pay later

- overdrafts

How your deposit changes everything

A larger deposit can:

- reduce loan-to-value

- improve mortgage rates

- reduce monthly repayments

- make applications more attractive

- increase the property price you can target

- reduce the risk of negative equity

Deposit makes a real difference

£50k salary: with a £20k deposit your budget is around £220,000–£245,000; with a £60k deposit it rises to around £260,000–£285,000.

First-time buyer costs

Your deposit is not the only upfront cost. Budget for the following on top of your deposit:

- valuation fee

- legal fees

- survey

- mortgage arrangement fee

- broker fee where applicable

- moving costs

- buildings insurance

- initial furniture

- repairs

- emergency fund

- Stamp Duty where applicable

Stamp Duty and buying costs

For England and Northern Ireland, Stamp Duty Land Tax (SDLT) rules apply. Scotland and Wales have different systems (Land and Buildings Transaction Tax and Land Transaction Tax respectively).

- a standard SDLT threshold below which no SDLT is due

- a higher first-time buyer relief threshold for eligible buyers

- an additional property surcharge for second homes and buy-to-let

Always use an official calculator for exact figures. You can estimate the cost with our Stamp Duty Calculator or read our Stamp Duty Explained guide.

Affordability mistakes to avoid

Common affordability mistakes

- using gross salary only

- forgetting debts

- ignoring monthly bills

- borrowing the maximum just because a lender allows it

- forgetting Stamp Duty

- ignoring service charges

- not stress-testing higher interest rates

- assuming bonuses count fully

- underestimating maintenance

- applying before checking your credit file

- not keeping emergency savings

How to increase what you can afford

Practical ways to improve your affordability include:

- save a larger deposit

- reduce debts

- improve your credit score

- extend the mortgage term carefully

- consider a joint application

- reduce monthly commitments

- compare lenders

- speak to a mortgage broker

- consider lower-cost areas

- use salary sacrifice carefully, because it may reduce mortgage affordability if it lowers your payslip income

Salary sacrifice and mortgages

Estimate your mortgage affordability

Use the Money Tools UK Mortgage Affordability Calculator to estimate how much you may be able to borrow based on salary, deposit, monthly costs and mortgage assumptions.

Related salary guides

- £20k Salary After Tax UK

- £30k Salary After Tax UK

- £40k Salary After Tax UK

- £50k Salary After Tax UK

- £60k Salary After Tax UK

- £70k Salary After Tax UK

- £80k Salary After Tax UK

- £100k Salary After Tax UK

- Salary Sacrifice Explained

- Adjusted Net Income Explained

Related calculators

- Mortgage Affordability Calculator

- Stamp Duty Calculator

- UK Take-Home Pay Calculator

- Salary to Hourly Calculator

Sources & references

This guide reflects independent UK mortgage affordability, lending and Stamp Duty guidance for the 2025/26 tax year.

- MoneyHelper — Mortgage affordability calculator

- MoneyHelper — Buying a home

- GOV.UK — Stamp Duty Land Tax

- GOV.UK — Stamp Duty Land Tax: first-time buyer relief

- Bank of England — Mortgage market and loan-to-income policy

- Financial Conduct Authority — Mortgages and responsible lending

Last updated

This article was last reviewed on 20 June 2026 and reflects UK mortgage affordability, salary, deposit and Stamp Duty guidance available for the 2025/26 tax year.

Disclaimer

Money Tools UK provides educational information and calculators only. Mortgage affordability depends on lender criteria, credit history, deposit, income, debts, spending, interest rates and personal circumstances. This article is not mortgage, financial or tax advice. Speak to a qualified mortgage adviser before making borrowing decisions.

Get new UK finance and property guides from Money Tools UK

Plain-English UK finance insights, tax updates and property investing guides.

Related calculators

Mortgage Affordability Calculator

The exact calculator this article is built around — open it and run your own numbers.

Open calculatorFrequently asked questions

Related guides

More flagship guides and tools from Money Tools UK.

A plain-English UK guide to checking if HMRC owes you a tax refund: why overpayments happen, how to use your Personal Tax Account, P800 and Simple Assessment, when refunds are automatic, how to claim, and how to avoid tax refund scams.

Read guide

Why HMRC overtaxes pension withdrawals with emergency tax, how pension tax refunds work, and which form to use — P55, P53Z, P50Z or P53 — to reclaim overpaid tax for 2025/26.

Read guide

Can you still use a limited company inside IR35? Learn what happens to PAYE, dividends, Corporation Tax, expenses, umbrella companies and mixed inside/outside IR35 contracts.

Read guideDisclaimer: This content is for informational purposes only and should not be treated as financial, tax, mortgage, investment or legal advice.